Latest News

The 6th Energy Storage Safety Forum Successfully Held in Hefei

With the diversification of energy storage technologies, application scenarios are rapidly expanding beyond traditional power systems into emerging fields such as industrial manufacturing, data centers, and zero-carbon parks. However, these emerging applications have much lower tolerance for fire risks, presenting unprecedented challenges to the safe development of the energy storage industry. At this critical stage, the 6th Energy Storage Safety Forum, themed “AI Empowering Energy Storage Risk Management and Control, Safety Building a Sustainable Future”, aimed to build industry consensus, address key safety challenges, and promote the stable and sustainable growth of the energy storage sector.

On July 17, 2026, the 6th Energy Storage Safety Forum was successfully held in Hefei, Anhui Province. The event was organized by the China Energy Storage Alliance (CNESA), and co-organized by the National Energy Storage Technology Industry-Education Integration Innovation Platform of Tianjin University, the CNESA Energy Storage Safety Committee, and Gotion High-tech. The forum brought together government officials, industry leaders, academic experts, and research institutions to jointly explore pathways toward safer and more sustainable energy storage development.

The opening ceremony gathered representatives from government authorities, leading research institutions, and enterprises. Attendees included Wang Shijiang, Deputy Director of the Department of Electronic Information of the Ministry of Industry and Information Technology (MIIT); Xu Ziming, Deputy Director of the Electricity Safety Supervision Department of the National Energy Administration (NEA); Jiang Chenyue, Member of the Party Leadership Group and Deputy Director of the Anhui Provincial Department of Industry and Information Technology; Zeng Xiaoming, Member of the Party Leadership Group and Deputy Director of the Anhui Energy Bureau; Sun Jinhua, Academician of the European Academy of Sciences and Professor at the University of Science and Technology of China; Chen Zhongwei, Fellow of the Royal Society of Canada and the Canadian Academy of Engineering; Chen Haisheng, Director of the Institute of Engineering Thermophysics at the Chinese Academy of Sciences; Yang Quanhong, Chair Professor at Tianjin University; Zhuo Ping, Director of the Fourth Research Division of Tianjin Fire Research Institute under the Ministry of Emergency Management; Wang Qisui, Executive President of Gotion High-tech; and Yu Zhenhua, Executive Vice Chairman of CNESA.

The forum also received strong support from organizations and companies including the School of Energy and Power Engineering at Tianjin University, Sungrow, Envision Energy, Honeywell China, Xien Technology, Pengcheng Infinite, Benji Electric, Yangyi Technology, and Huachu Technology. The opening ceremony was hosted by Liu Wei, Secretary General of CNESA.

Opening Remarks: Balancing Energy Storage Safety and Development

In his opening speech, Wang Shijiang stated that energy storage is a key driver for achieving China’s dual-carbon goals. The country’s energy storage industry is currently developing rapidly, with strong momentum. In the first quarter of 2026, China’s energy storage lithium battery output reached 185GWh, representing year-on-year growth of more than 100%. Meanwhile, technological innovation continues to accelerate, with applications expanding across power systems, industrial sectors, and zero-carbon parks.

However, safety risks have become a major bottleneck restricting high-quality industry development. Wang emphasized that MIIT’s Department of Electronic Information will coordinate both development and safety, focusing on four key areas:

Strengthening top-level planning and guiding the industry’s transition from scale expansion toward quality improvement and enhanced safety;

Regulating market competition and fostering a healthy industrial ecosystem;

Establishing a strong safety foundation by accelerating the development of national standards, including safety grading evaluation standards for energy storage batteries;

Enhancing technological innovation to prevent and mitigate safety risks at the source.

He called for deeper collaboration across the industry to jointly promote safe, healthy, and sustainable development of energy storage.

Jiang Chenyue

Deputy Director, Anhui Provincial Department of Industry and Information Technology

Jiang Chenyue highlighted Anhui’s strong industrial growth, noting that the province’s industrial output value has increased from RMB 3.8 trillion at the beginning of the 14th Five-Year Plan period to RMB 5.5 trillion, with its national ranking rising from 12th to 6th place.

In the energy storage sector, Anhui has established a complete industrial chain covering materials, batteries, and systems. Multiple technology routes are developing in parallel, and the industry scale has grown sixfold since the beginning of the 14th Five-Year Plan period, surpassing RMB 1 trillion last year. Leading companies such as Gotion High-tech and Sungrow have emerged as globally competitive enterprises, with energy storage battery cells and system shipments ranking among the world’s leading levels.

Looking ahead to the 15th Five-Year Plan period, Anhui will prioritize new energy storage as a key sector within its “1188” modern industrial system. The province will further integrate industrial development with technological innovation, strengthen market players, accelerate commercialization of new technologies and products, and build an ecosystem integrating government, industry, academia, research, finance, services, and applications.

Chen Haisheng

Chairman of CNESA; Director of the Institute of Engineering Thermophysics, Chinese Academy of Sciences

Chen Haisheng stated that 2026 marks a critical year for China’s new energy storage industry as it transitions from large-scale expansion toward high-quality growth.

By the end of June 2026, China’s cumulative installed capacity of energy storage projects reached 237.2GW, representing year-on-year growth of 41.4%. Among this, new energy storage accounted for 168.2GW, exceeding 70% of total capacity. Newly installed capacity reached 21.64GW/58.20GWh, while storage duration continued to increase and technology pathways rapidly evolved.

Despite rapid industry expansion, safety challenges remain the most critical issue facing the sector. Chen emphasized that CNESA will continue strengthening international cooperation, building a global energy storage safety platform, developing comprehensive safety systems, and supporting the global transition toward green and low-carbon energy.

Emerging Insights: Tackling Energy Storage Safety Challenges Across the Entire Value Chain

A clear trend is emerging: energy storage safety innovation is moving beyond battery cell-level protection toward a comprehensive approach integrating battery innovation, system architecture, intelligent operation and maintenance, safety standards, and application scenarios.

Sun Jinhua

Academician of the European Academy of Sciences; Professor, University of Science and Technology of China

In his presentation titled “Fire Risks and Prevention Strategies for Energy Storage in Computing Power and Data Centers,” Sun Jinhua highlighted the rapid growth of electricity demand from artificial intelligence computing and data centers.

Electricity consumption by computing and data centers approached 200 billion kWh in 2025 and is expected to reach 526–700 billion kWh by 2030. With China requiring newly built data centers in national computing hubs to achieve at least 80% renewable electricity consumption, energy storage will become increasingly essential.

However, fire risks remain a major concern. Global energy storage fire probability is estimated at approximately 0.3%–0.4%, while data centers face higher potential losses due to concentrated assets and personnel, requiring much stricter safety standards.

Sun proposed three layers of safety protection:

Improving intrinsic battery safety through interdisciplinary research and AI technologies to reduce thermal runaway probability below 10⁻⁸;

Enhancing process safety through intelligent thermal management materials, fiber-optic in-situ monitoring, and integrated thermal management and early-warning technologies;

Optimizing firefighting solutions through technologies such as liquid nitrogen extinguishing and multiple-stage suppression.

He emphasized the need to develop intelligent safety management platforms integrating remote monitoring, predictive analysis, multi-level warnings, and dynamic response capabilities.

Chen Zhongwei, Fellow of the Royal Society of Canada and the Canadian Academy of Engineering; Researcher and PhD Supervisor at the Dalian Institute of Chemical Physics, Chinese Academy of Sciences.

Chen Zhongwei delivered a keynote speech titled “Building an Intelligent Management System for the Full Life Cycle of Electrochemical Energy Storage.”

He identified five major challenges in the energy storage industry: design, manufacturing, management, operation and maintenance, and electricity market participation. AI-based full life-cycle management provides a key solution.

Since 2015, Chen’s team has focused on integrating electrochemistry and artificial intelligence, achieving breakthroughs in:

Building battery industrial databases covering design, manufacturing, management, and operation;

Developing AI-assisted battery design based on electrochemical simulation;

Creating electrochemistry-AI coupled models for battery health evaluation;

Establishing closed-loop manufacturing optimization through production data and performance feedback;

Applying AI algorithms and robotics for retired battery sorting and second-life utilization;

Developing high-precision algorithms for RUL, SOC, and SOH estimation.

Based on these technologies, the team developed the Energy Storage AI Intelligent Monitoring System, establishing a three-level health diagnosis framework covering cells, battery containers, and entire energy storage stations.

Yang Quanhong

Chair Professor, Tianjin University

Yang Quanhong discussed “Water Management in Intrinsically Safe Aqueous Zinc Batteries: Fundamental Principles and Solutions.”

He emphasized that future energy storage technologies must achieve high safety, low cost, and resource sustainability. Aqueous zinc batteries represent a promising pathway due to their intrinsic safety and resource availability.

However, commercialization faces challenges caused by water-related reactions, including hydrogen evolution, corrosion, dendrite growth, cathode structural degradation, and limited cycle life.

The key solution lies in precise “water management,” including:

Water reaction management;

Water demand management;

Water state management;

Advanced conversion-type cathode technologies.

Zhuo Ping

Director, Fourth Research Division, Tianjin Fire Research Institute, Ministry of Emergency Management

Zhuo Ping introduced China-led international standards research on energy storage fire safety.

She explained that energy storage fire scenarios should consider four major safety objectives:

Life safety;

Property protection;

Environmental protection;

Cultural heritage protection.

Fire scenarios should incorporate different application characteristics, ignition sources, fire types, firefighting systems, and human behaviors.

Zhang Peidao

Solution Director, Energy Storage Business Division, Gotion High-tech

Zhang Peidao shared industrial practices under the theme “Architectural Innovation of Energy Storage Systems in New Power Systems.”

He noted that energy storage faces challenges including efficiency improvement, safety risks, high availability requirements, and life-cycle cost optimization.

Gotion High-tech addresses these challenges through architectural innovation:

The Qianyuan Intelligent Energy Storage 2.0 grid-forming high-voltage cascade storage system directly connects to 6–35kV grids without transformers;

System efficiency exceeds 92%;

AI-based predictive maintenance improves operational efficiency by 50%;

Multi-dimensional sensing and fire protection systems create layered safety protection;

Modular design reduces land occupation by 38%.

The solutions have already been applied in projects including user-side storage in Jinzhai and grid-side storage in Lujiang.

Roundtable Discussion: AI Empowering Energy Storage Safety from Passive Protection to Active Intelligence

The roundtable focused on how AI can transform energy storage safety from passive prevention to proactive intelligence.

Hosted by Wang Qingsong, Researcher at the University of Science and Technology of China and Chairman of the CNESA Energy Storage Safety Committee, the discussion gathered experts from grid operators, equipment manufacturers, industrial software providers, sensor companies, and AI technology companies.

Participants agreed on three major conclusions:

The transition from passive protection to active intelligence is inevitable.

AI will not replace intrinsic battery safety, hardware protection, or human operation, but will serve as an enabling technology connecting sensing, simulation, and decision-making.AI adoption should follow a gradual human-machine collaboration approach.

Challenges remain, including data silos, limited algorithm generalization, incomplete standards, and hardware adaptation issues.Full industrial collaboration is essential.

Energy storage intelligent safety requires cooperation among grid operators, battery manufacturers, research institutions, software companies, and sensor providers.

Launch of the New Intelligent Safety Ecosystem for Energy Storage

During the opening ceremony, Gotion High-tech initiated the establishment of the New Energy Storage Digital Intelligence Safety Ecosystem, bringing together universities, research institutions, and industry leaders.

Representatives from organizations including Beijing University of Science and Technology, University of Science and Technology of China, Hefei University of Technology, Gotion High-tech, Siemens Digital Industries Software, iFlytek, Tishen Technology, Inovance Technology, and CNESA participated in the launch ceremony.

Special Forums: Exploring the Future Path of Energy Storage Safety Technologies

Two parallel forums were held in the afternoon:

“Safety of Energy Storage Power Stations and Commercial & Industrial Storage Systems”

This forum focused on:

Implementation of safety standards;

Fire monitoring and early-warning technologies;

Fire risk assessment of large-scale lithium iron phosphate systems;

Immersion cooling technologies;

Full-chain safety solutions for sodium-ion batteries.

“AI and Energy Storage Safety”

This forum explored:

National-level energy storage operation data platforms;

Intelligent operation and maintenance technologies;

Big data platforms for power generation companies;

AI-driven life-cycle management of large-scale energy storage.

The 6th Energy Storage Safety Forum brought together government authorities, industry players, academic experts, and research institutions to explore the future of energy storage safety.

Participants agreed that safety is the foundation for high-quality energy storage development, and AI-driven technologies are accelerating the transformation from passive protection toward proactive intelligent safety management.

Looking ahead, only through collaboration across the entire value chain and continuous strengthening of safety foundations can the energy storage industry achieve sustainable growth and contribute Chinese solutions to the global green energy transition.

Bookmark This! Six Long-Duration Energy Storage Technology Pathways, Three Revenue Models, and Prospects for Large-Scale Deployment

With multiple supportive policies being introduced, long-duration energy storage (LDES) is entering a period of significant growth opportunities!

Recently, the State Council of China issued the “15th Five-Year Plan Carbon Peak Action Plan”, while the National Energy Administration released the “Energy Sector Energy Conservation and Carbon Reduction Action Plan (2026–2028)”. Both policy documents explicitly emphasized the development of long-duration energy storage, indicating that LDES is gradually becoming an essential component of the new power system.

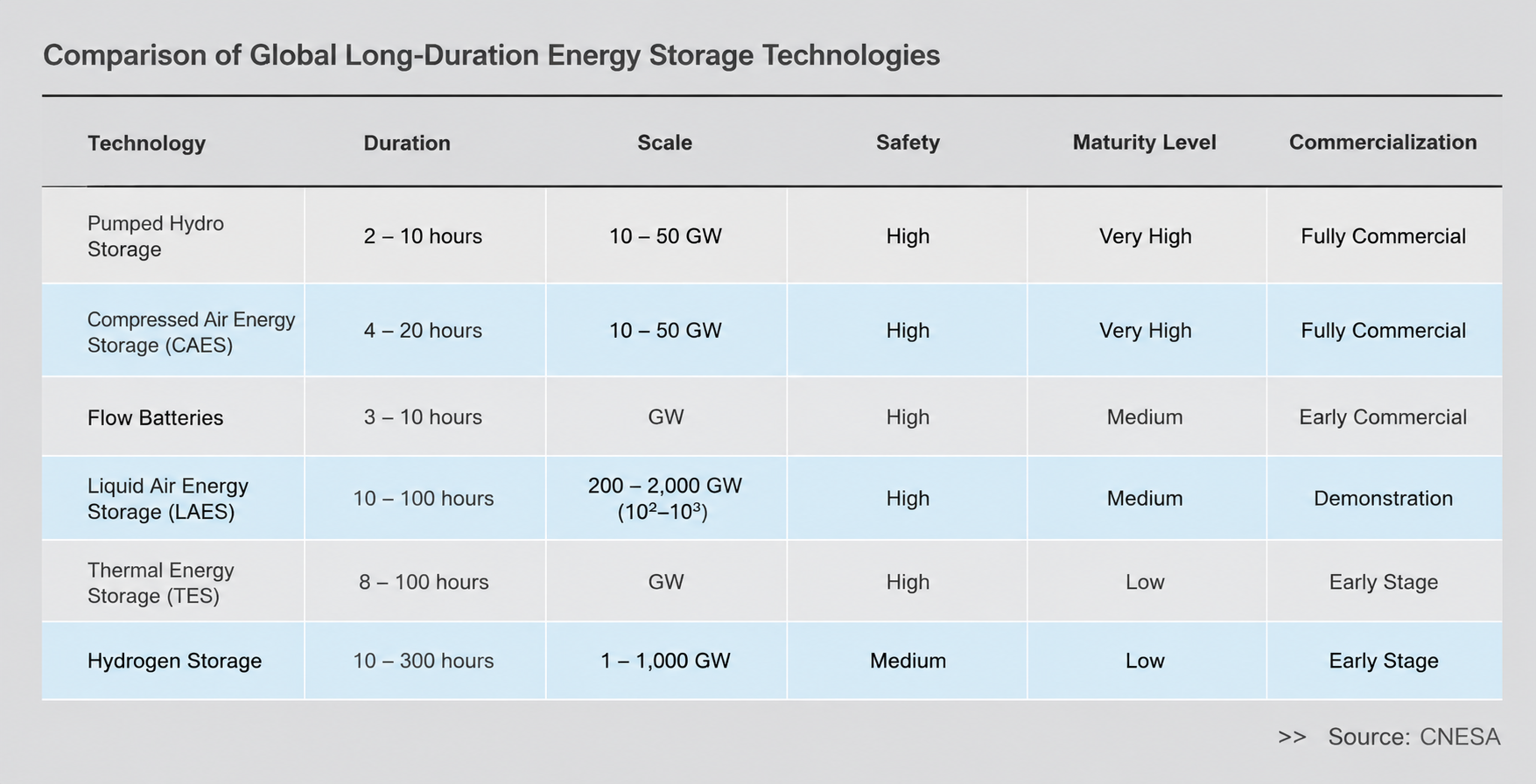

Currently, LDES technologies are developing toward greater diversification. Technologies such as compressed air energy storage (CAES), flow batteries, and hydrogen energy storage each demonstrate different advantages and limitations in terms of technology maturity, application scenarios, and construction costs.

This article provides a systematic analysis of LDES from three perspectives: technology development, revenue structures, and prospects for large-scale deployment, offering industry insights and references.

Six Technology Pathways Leading LDES Development for Diverse Applications

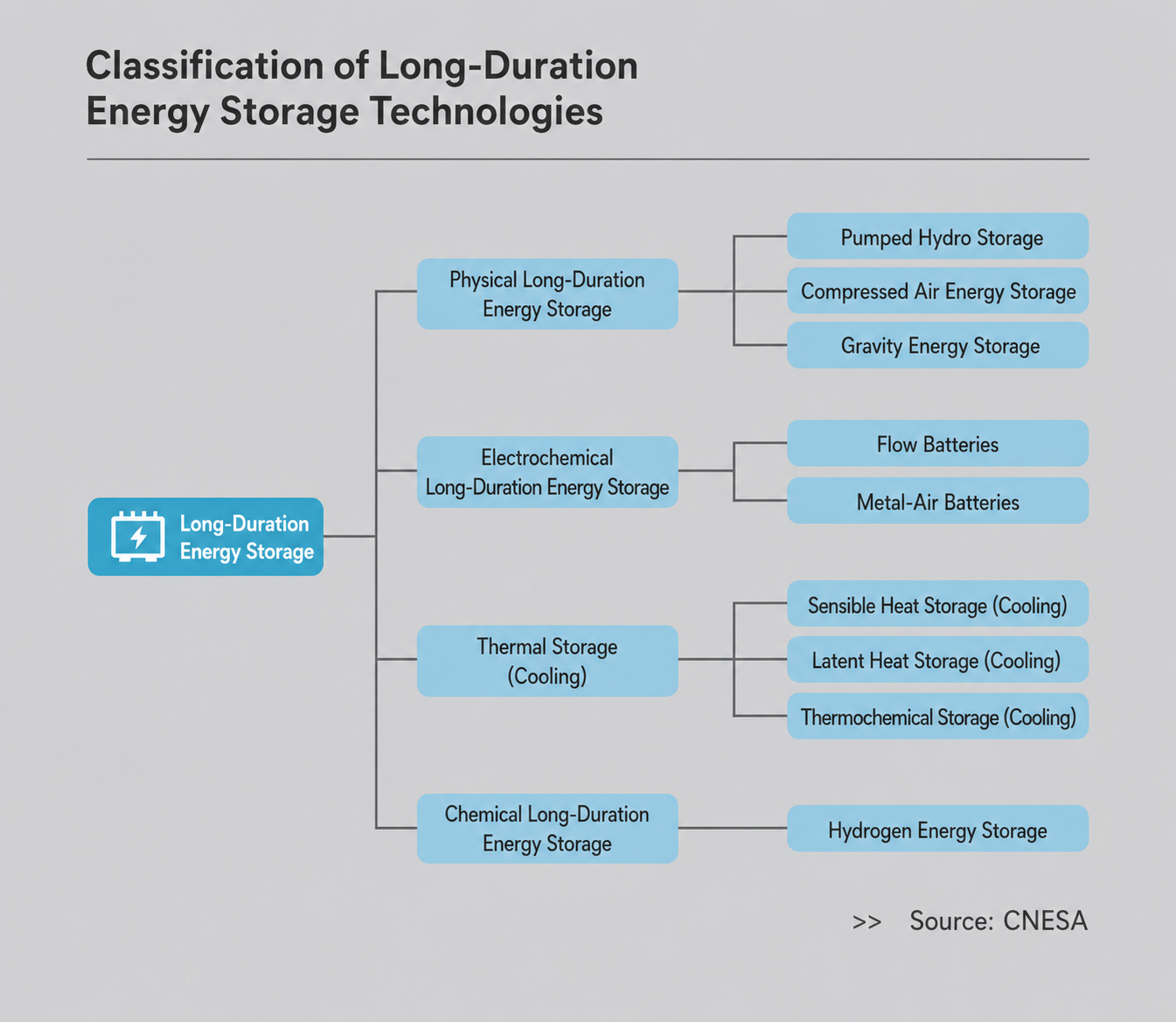

Long-duration energy storage technologies are diverse and mainly include:

Physical energy storage technologies, represented by pumped hydro storage, compressed air energy storage, and gravity energy storage;

Electrochemical energy storage technologies, represented by flow batteries and metal-air batteries;

Thermal energy storage (including cooling storage) and chemical energy storage technologies, represented by hydrogen energy storage.

Among them, pumped hydro storage is currently the most mature and widely deployed long-duration energy storage technology.

As of the first quarter of 2026, China’s operational pumped hydro storage capacity had reached 67.09 GW.

At present, pumped hydro storage is primarily based on large-scale fixed-speed pumped hydro power stations. However, as suitable sites for large-scale pumped hydro projects become increasingly limited, the development of small- and medium-scale pumped hydro storage projects is gradually increasing.

Gravity Energy Storage

The operating principle of gravity energy storage is similar to pumped hydro storage. It mainly uses the physical lifting and lowering of solid masses to drive power generation equipment, thereby achieving energy storage and discharge.

Currently, China’s 100 MWh-scale gravity energy storage tower demonstration project has been completed in Rudong, Jiangsu Province, and has entered the grid connection commissioning stage.

The project, invested and developed by China Tianying, has an energy storage capacity of 100 MWh and a power output of 25–26 MW. It is expected to be connected to the grid and begin operation by the end of 2026.

Compressed Air Energy Storage

Compressed air energy storage is another long-duration energy storage technology with significant potential for large-scale application.

The technology converts electricity from off-peak periods or curtailed renewable energy into compressed air pressure energy and thermal energy, storing them separately in air storage units and thermal storage units.

During periods of high electricity demand, the stored high-pressure air is released and expanded through turbines to generate electricity.

Currently, large-scale engineering applications mainly focus on adiabatic compressed air energy storage systems with thermal storage.

According to statistics from the China Energy Storage Alliance (CNESA), as of the first quarter of 2026, China had 14 operational compressed air energy storage projects connected to the grid, with a cumulative installed capacity exceeding 1.5 GW.

The total installed capacity of projects under construction and in the planning stage has exceeded 54 GW.

Flow Batteries

Flow batteries are electrochemical batteries in which the active materials of both the positive and negative electrodes are liquid.

Depending on the types of active electrode materials, flow batteries can be categorized into:

Vanadium redox flow batteries (VRFBs);

Zinc-bromine flow batteries;

Iron-chromium flow batteries;

and other technology pathways.

Overall, flow batteries offer advantages including:

high safety;

no risk of explosion or fire;

long service life;

deep charge and discharge capability;

and environmental friendliness.

By the end of 2025, China’s 10 kW-scale vanadium redox flow battery demonstration projects had already entered operation.

Thermal Energy Storage

Thermal energy storage refers to storing energy from sources such as:

solar thermal energy;

geothermal energy;

industrial waste heat;

low-grade waste heat;

and releasing it when needed, thereby addressing mismatches between thermal energy supply and demand caused by differences in time, location, or energy intensity.

Based on storage principles, thermal energy storage technologies can be categorized into three types:

sensible heat storage;

latent heat storage;

thermochemical energy storage.

Currently, relatively mature thermal storage materials include:

hot water;

molten salt;

refractory bricks;

and other thermal storage media.

Hydrogen Energy Storage

Hydrogen energy storage is a form of chemical energy storage that enables:

large-scale energy storage;

long-duration storage;

and cross-regional energy storage.

It mainly consists of three key stages:

hydrogen production;

hydrogen storage and transportation;

hydrogen utilization.

Water electrolysis for hydrogen production is expected to become the dominant future technology pathway.

Hydrogen storage and transportation technologies include:

gaseous hydrogen storage;

liquid hydrogen storage;

solid-state hydrogen storage;

ammonia (alcohol)-based hydrogen storage;

underground hydrogen storage;

and other approaches.

In the power sector, hydrogen energy can generate electricity mainly through:

hydrogen gas turbines;

hydrogen internal combustion engines;

hydrogen fuel cells.

Different LDES Technologies Demonstrate Distinct Competitive Advantages

Different long-duration energy storage technology pathways demonstrate diverse technical characteristics and competitive advantages.

In terms of efficiency, pumped hydro storage and gravity energy storage achieve relatively high efficiency, while molten salt thermal storage and hydrogen energy storage have comparatively lower efficiency.

Regarding service life, physical energy storage technologies such as pumped hydro storage, compressed air energy storage, and gravity energy storage generally offer longer lifetimes.

In terms of safety, most LDES technologies demonstrate high safety levels, except hydrogen energy storage, which requires additional safety considerations.

Regarding environmental adaptability, pumped hydro storage and compressed air energy storage have relatively limited adaptability to certain environmental conditions.

In terms of response speed, flow batteries demonstrate significant advantages.

Lifecycle Cost of Energy Storage Determines Economic Competitiveness

The levelized cost of electricity (LCOE) over the full lifecycle is a key indicator for evaluating the economic performance of energy storage technologies.

According to estimates from the China Energy Storage Alliance (CNESA), when the storage duration reaches 8 hours, salt cavern compressed air energy storage and pumped hydro storage currently demonstrate relatively lower lifecycle electricity costs.

With continuous technological advancement and large-scale deployment, the lifecycle costs of emerging long-duration energy storage technologies are expected to continue declining.

According to projections, by 2035, mainstream LDES technologies including:

compressed air energy storage;

pumped hydro storage;

flow batteries;

molten salt thermal storage;

could achieve lifecycle electricity costs of approximately:

RMB 0.3–0.5/kWh

under conditions of 250 annual utilization cycles.

If calculated based on each technology’s inherent lifecycle cycle life, the lifecycle cost of energy storage could decline even further.

Revenue Channels Established, Value of Long-Duration Storage Yet to Be Fully Released

Currently, the development of market mechanisms for long-duration energy storage is accelerating its transition from policy-driven growth toward market-driven development.

The three-part revenue structure of:

“Energy Market + Capacity Market + Ancillary Services Market”

is gradually moving from the stage of framework establishment toward detailed implementation.

Energy Market: The Most Fundamental Revenue Source

The energy market is currently the most fundamental and primary revenue source for long-duration energy storage.

The core business logic is:

“Charge during low-price periods and discharge during high-price periods.”

Compared with 2-hour energy storage systems, the key advantage of LDES lies in its ability to provide:

cross-period energy shifting;

large-scale electricity time-shifting capability;

and flexible short-term operation.

Some technology pathways can also achieve multiple daily cycles, allowing them to capture more price arbitrage opportunities.

In provinces where electricity spot markets are relatively mature, peak-valley price differences have become a major revenue source for energy storage projects.

Taking compressed air energy storage as an example, the first phase of the Jintan Salt Cavern Compressed Air Energy Storage National Demonstration Project in Jiangsu, which began operation in 2024, has an installed capacity of:

60 MW / 300 MWh

The project can achieve:

one charge and two discharge cycles per day;

or multiple charge-discharge operations within a day.

Capacity Market: Providing Long-Term Reliability Value

Unlike the “price arbitrage” mechanism of the energy market, the core logic of the capacity market is the “value of availability” — meaning that energy storage systems commit to remaining available whenever the power grid requires support.

This mechanism is particularly important for long-duration energy storage because:

it requires higher upfront investment costs;

it has a longer payback period;

and it requires stable baseline revenues to improve project bankability.

Currently, the development of capacity markets in China demonstrates a dual-track approach, which is gradually removing market access barriers for long-duration energy storage.

On one hand, the coal-fired power capacity pricing mechanism began nationwide implementation in 2024, providing a stable revenue foundation for the transformation of thermal power generation.

On the other hand, the Notice on Improving the Capacity Electricity Pricing Mechanism for the Generation Side, released in January this year, established for the first time at the national policy level a capacity electricity pricing mechanism for independent new-type energy storage systems on the grid side.

Based on the principle of “equal pay for equal performance,” independent energy storage has officially been incorporated into the generation-side capacity pricing mechanism.

The capacity payment mechanism for independent energy storage has therefore evolved from regional exploration toward a nationwide unified framework.

Ancillary Services Market: Unlocking Additional Value

If the energy market addresses the question of “whether energy storage can generate revenue,” the ancillary services market determines “whether energy storage can generate additional value.”

Currently, power ancillary service markets mainly include three categories:

frequency regulation;

peak shaving;

backup reserve.

In regions where electricity spot markets operate on a regular basis, peak-shaving ancillary services have gradually been replaced by spot energy markets, with their original functions being absorbed by electricity trading mechanisms.

Meanwhile, some provinces have begun pilot programs for new ancillary services, including:ramping support;

inertia support;

and other grid flexibility services.

Long-duration energy storage can provide:long-cycle energy shifting;

backup reserve capability;

and some technology pathways can also provide physical inertia, effectively supporting grid stability requirements.

However, although the three-part revenue structure appears relatively complete, the current market mechanism still mainly focuses on the question of “whether energy storage exists”, without further distinguishing “how long energy storage can provide service.”

The differentiated advantages of LDES — including:cross-time energy shifting;

large capacity;

high reliability;

have not yet been fully translated into market revenues.

This remains the most significant challenge in current market mechanism development and represents a key area requiring further breakthroughs.

Technology and Market Mechanisms Advancing Together to Support Demonstration Deployment

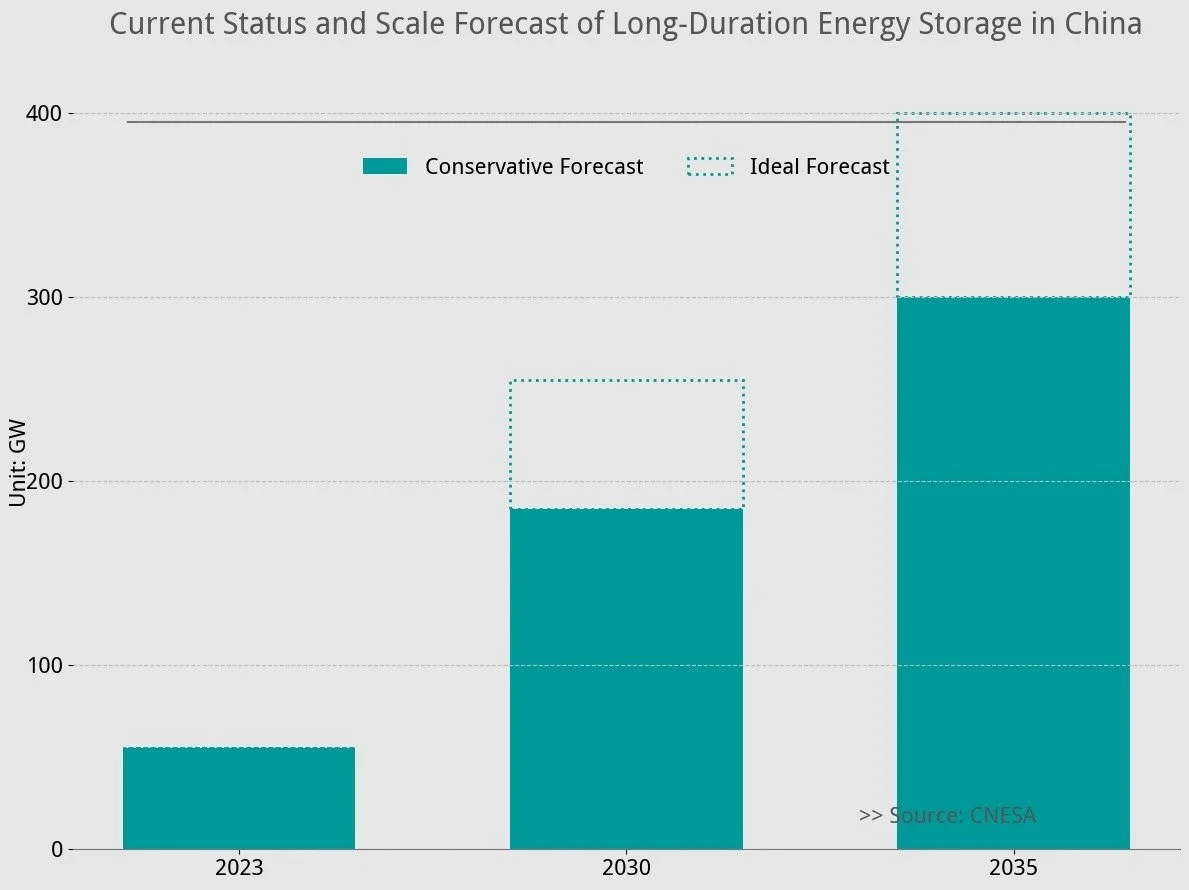

At the recently held Energy Storage International Conference and Expo (ESIE2026), Ma Yuan, Assistant Researcher at the Department of Earth System Science of Tsinghua University, stated that by 2030, energy storage capacity should account for 15%–20% of total renewable energy installed capacity, reaching a key milestone of approximately 400 GW.

Among this capacity, long-duration energy storage with durations exceeding 8 hours should account for at least 20% in order to effectively reduce renewable energy curtailment and ensure power system security.

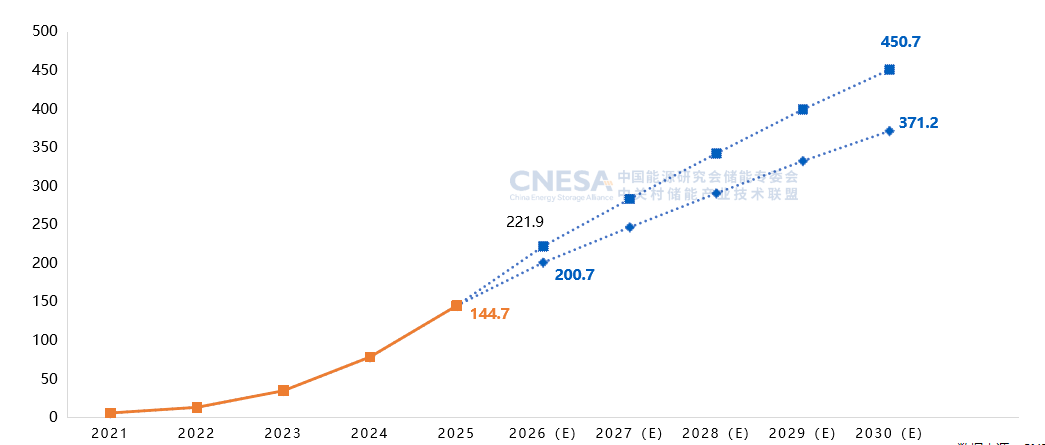

According to forecasts from the China Energy Storage Alliance (CNESA), during the 15th Five-Year Plan period, demand for long-duration energy storage will gradually become more prominent.

New LDES demand during this period will mainly focus on storage durations of:

4–10 hours

Under a conservative scenario, the market scale is expected to reach:

180 GW

while under an optimistic scenario, it could reach:

250 GW

Pumped hydro storage will remain the dominant technology, complemented by emerging LDES technologies such as:compressed air energy storage;

electrochemical energy storage.

However, this scale still falls short of the requirements of power grid companies.

In some northwestern provinces with high renewable energy penetration, demand for 24-hour-plus long-duration energy storage is expected to emerge first.

By 2035, the scale of long-duration energy storage is expected to reach:300 GW under a conservative scenario;

400 GW under an optimistic scenario.

Storage durations will mainly range from:

4–24 hours

while the deployment scale of emerging LDES technologies will continue to increase.

Accelerating the Transition from Technology Demonstration to Large-Scale Deployment

To continuously promote the transition of long-duration energy storage from technology demonstration to large-scale commercial application, more projects need to be implemented to transform technological maturity into commercial viability.

1. Coordinated Demonstration of Different Technology Pathways

Currently, emerging LDES projects face challenges including:technologies that are not yet fully mature;

incomplete industrial supply chains;

relatively high investment costs.

As a result, commercial applications remain dominated by short-duration lithium-ion battery energy storage.

Going forward, demonstration and deployment of LDES technologies should be promoted in an orderly manner based on different stages of technological development.

This approach will accelerate the implementation of emerging technologies while driving industrial technology upgrades and improving market competitiveness.

2. Promote Scenario-Specific Demonstration Projects Based on Local Conditions

Under the new power system framework, different application scenarios have different requirements for long-duration energy storage.

For example:developed cities in eastern China have relatively higher requirements for energy density;

northwestern “desert, Gobi, and barren land” regions;

eastern coastal areas;

and cold regions in northeastern China;

all have different requirements regarding:operating temperature;

humidity resistance;

sand and dust protection;

and environmental adaptability.

Therefore, demonstration projects should be combined with different application environments to deepen research into key technologies including:energy storage equipment;

system integration;

safety protection;

and operational reliability.

3. Strengthen Long-Term Monitoring and Evaluation of Demonstration Projects

Currently, management and evaluation mechanisms for demonstration projects are not yet sufficiently comprehensive.

In the future, long-term tracking, monitoring, and periodic evaluation should be carried out for demonstration projects.

This will provide scientific data support for:the practical application of new technologies;

new products;

and innovative solutions.

It will also provide evidence-based support for national industrial policies and technical standards.

4. Encourage Demonstration Projects to Explore Innovative Policies and Business Models

While demonstrating LDES technologies, pilot projects should also serve as platforms for exploring innovative commercial models.

At the same time, improving policy mechanisms and market support systems will be a critical foundation for large-scale LDES development.

Establishing Cost Recovery Mechanisms for Long-Duration Energy Storage

Compared with short-duration energy storage, LDES demonstrates greater value through:capacity contribution;

long-term backup capability;

and system reliability support.

Therefore, it is necessary to gradually establish market-based capacity cost recovery mechanisms.

Through market competition and pricing mechanisms, investment entities can be encouraged to make reasonable investments, ensuring long-term adequacy of power system capacity.

Improving Cost Allocation Mechanisms for Long-Duration Energy Storage

Long-duration energy storage can directly or indirectly accelerate the replacement of traditional fossil fuel power generation with renewable energy, significantly reducing overall societal carbon emissions.

In the future, policy and market frameworks for:green electricity;

green electricity certificates;

carbon trading;

should be further developed.

These mechanisms can better reflect the value of LDES in:energy transition;

carbon reduction;

and renewable energy integration.

By expanding revenue sources and improving cost allocation mechanisms, the economic foundation for long-duration energy storage can be further strengthened.

Conclusion

Long-duration energy storage is becoming an increasingly important pillar of future power systems as renewable energy deployment accelerates.

With continuous technological innovation, improved market mechanisms, and increasing project deployment, LDES is expected to move from early-stage demonstration toward large-scale commercialization.

The future development of long-duration energy storage will depend not only on breakthroughs in individual technologies, but also on the coordinated evolution of:technology pathways;

market structures;

business models;

and policy frameworks.

Together, these factors will unlock the full value of LDES in supporting renewable energy integration, enhancing grid flexibility, and enabling the global energy transition.

Top Energy Storage Projects in China in H1 2026

In the first half of 2026, China’s new energy storage sector maintained rapid growth momentum, with multiple breakthroughs achieved in grid-connected projects. Notably, industry development is no longer focused solely on maximizing individual project scale. While lithium iron phosphate (LFP) battery storage remains the dominant technology route, the industry is gradually shifting from simply expanding installed capacity toward improving the overall performance and efficiency of energy storage systems.

Energy storage technologies are becoming increasingly diversified. Beyond lithium-ion batteries, long-duration energy storage technologies such as vanadium redox flow batteries and compressed air energy storage have achieved large-scale grid-connected demonstrations. Emerging technologies, including semi-solid-state batteries, have also entered engineering demonstration stages. Meanwhile, grid-forming energy storage, intelligent string-based storage systems, and cloud-based energy storage solutions are accelerating commercialization and deployment.

Energy storage application scenarios continue to expand, covering a wide range of use cases including generation-side, grid-side, behind-the-meter, and standalone energy storage. Integrated models such as solar-storage, solar-hydrogen-storage, and grassland photovoltaic complementary storage projects are also being implemented.

The China Energy Storage Alliance (CNESA) has compiled representative new energy storage projects launched or connected to the grid in the first half of 2026 for industry reference.

01

China’s Largest Offshore PV-Hydrogen-Storage Integrated Demonstration Project

Guohua Investment Jiangsu Rudong Offshore PV-Hydrogen-Storage Integrated Project

Grid Connection Date: June 2026

Location: Jiangsu Province

Owner: Guohua (Rudong) New Energy Co., Ltd.

Energy Storage Technology: Lithium Iron Phosphate (LFP) Battery Storage

Storage Scale: 60MW/120MWh

Located at Yangkou Port in Rudong, Jiangsu Province, the project is one of the key projects under China’s third batch of large-scale photovoltaic bases.

The project integrates a 400MW photovoltaic power plant, a 60MW/120MWh energy storage system, and a green hydrogen production facility with a capacity of 1,500 Nm³/h, forming a complete industrial chain covering green electricity generation, storage, and conversion.

02

China’s Largest Single-Site PV + Energy Storage Project

Ningxia Yongli 300MW/600MWh Energy Storage Project

Grid Connection Date: June 2026

Location: Ningxia Hui Autonomous Region

Owner: Ningxia Dian Investment Yongli (Zhongwei) New Energy Co., Ltd.

Energy Storage Technology: Lithium Iron Phosphate (LFP) Battery Storage

Storage Scale: 300MW/600MWh

Located in Shapotou District, Zhongwei City, Ningxia, the project was developed specifically to support the 3GW photovoltaic base in Zhongwei.

The project consists of three independent energy storage stations — No.1, No.2, and No.3 — each with a capacity of 100MW/200MWh. The combined installed capacity reaches 300MW/600MWh.

03

China’s Largest Vanadium Flow Battery Energy Storage Power Station

Three Gorges Group Xinjiang Jimusar 1GW PV + Vanadium Flow Battery Energy Storage Integrated Project

Grid Connection Date: June 2026

Location: Xinjiang

Owner: Three Gorges New Energy Jimusar Power Generation Co., Ltd.

Energy Storage Technology: Vanadium Redox Flow Battery (VRFB)

Storage Scale: 200MW/1000MWh

Located in Jimusar County, Changji Hui Autonomous Prefecture, Xinjiang, the project features a rated power capacity of 200MW and an energy storage capacity of 1,000MWh.

It is currently the largest vanadium flow battery energy storage power station in China, representing a major milestone in the large-scale application of long-duration energy storage technologies.

04

China’s First Desert Grassland “PV + Grassland Complementary” Pilot Project

Huaneng Inner Mongolia Tongwei Green Materials New Energy Storage Project

Grid Connection Date: May 2026

Location: Inner Mongolia Autonomous Region

Owner: Baotou No.1 Thermal Power Plant, North United Power Co., Ltd. (Huaneng North China Company)

Energy Storage Technology: Lithium Iron Phosphate (LFP) Battery Storage

Storage Scale: 90MW/360MWh

Developed by Huaneng North China Company’s Baotou No.1 Thermal Power Plant, the project has a planned renewable energy capacity of 350MW, including:

300MW wind power

50MW photovoltaic power

90MW/360MWh electrochemical energy storage system

The project adopts a “grassland + photovoltaic” complementary model, with renewable electricity accounting for 50.17% of the electricity consumption of the industrial silicon production facility.

05

The Industry’s First Fully Green Electricity Demonstration Factory

Baima Mountain Fully Green Electricity Factory

Grid Connection Date: March 2026

Location: Anhui Province

Owner: Anhui Conch Group

Energy Storage Technology: Lithium Iron Phosphate (LFP) Battery Storage

Storage Scale: 22.5MW/45MWh

Located in Wuhu, Anhui Province, the project is the industry’s first fully green electricity demonstration factory integrating:

photovoltaic power generation

electrochemical energy storage

smart microgrid systems

new energy vehicle charging infrastructure

Building on waste heat power generation from cement kilns, the project innovatively expands photovoltaic deployment across multiple scenarios, including:

rooftop and corridor spaces

building facades

floating PV systems on water surfaces

curved roof structures

By utilizing more than 130,000 square meters of available space, the project integrates renewable generation and energy storage systems to establish a multi-energy complementary energy ecosystem.

06

China's First Distribution-Level Aqueous Organic Flow Battery Energy Storage Project

Suqian Era Aqueous Organic Flow Battery Distribution-Level Energy Storage Project

Grid Connection Date: March 2026

Location: Jiangsu Province and Anhui Province

Energy Storage Technology: Aqueous Organic Flow Battery

Storage Capacity: 60kW/120kWh

The project represents China's first deployment of an aqueous organic flow battery energy storage system at the distribution-transformer level.

It achieved several technological breakthroughs, including the development of an organic quaternary ammonium salt-based electrolyte system, a high-ion-conductivity anion exchange membrane, and advanced multi-physics coupled control technology.

Jointly developed by Suqian Era Energy Storage Technology Co., Ltd. and State Grid Electric Power Research Institute, the project was commissioned in Suqian Economic Development Zone, Jiangsu Province, with a parallel deployment in Chuzhou, Anhui Province.

07

China's Largest Single-Site PV Project in a Coal Mining Subsidence Area

Ningxia Lingwu 4GW PV Project in a Coal Mining Subsidence Area

Grid Connection Date: February 2026

Location: Ningxia Hui Autonomous Region

Owner:CHN Energy

Energy Storage Technology: Lithium Iron Phosphate (LFP)

Storage Capacity: 400MW/800MWh

The project is being developed in two phases with a total installed PV capacity of 4GW, making it China's largest single-site photovoltaic project built on a former coal mining subsidence area.

As one of the key projects under China's second batch of large-scale desert, Gobi, and wasteland renewable energy bases, it also serves as an important green power source for the Ningxia–Zhejiang LingShao UHV DC transmission corridor.

The project is planned to include 600MW/1,200MWh of battery energy storage, of which 400MW/800MWh has already been commissioned.

08

World's Largest Compressed Air Energy Storage Power Station

Jiangsu Guoxin Suyan Huai'an Salt Cavern Compressed Air Energy Storage Demonstration Project

Grid Connection Date: January 2026

Location: Jiangsu Province

Owner: Jiangsu Guoxin Suyan (Huai'an) Energy Storage Power Generation Co., Ltd.

Energy Storage Technology: Compressed Air Energy Storage (CAES)

Storage Capacity: 2 × 300MW / 2,400MWh

The project utilizes underground salt caverns in Huai'an, Jiangsu Province, to construct two 300MW non-fuel supplementary compressed air energy storage units.

It adopts internationally advanced high-temperature adiabatic compressed air energy storage technology, combining molten salt thermal storage with pressurized hot water heat storage.

With a total storage capacity of 2,400MWh and a round-trip efficiency of approximately 71%, it is currently the world's largest compressed air energy storage power station.

09

China's Largest Sodium-Ion Battery Energy Storage Power Station Under Construction

Honghu 100MW/200MWh Sodium-Ion Battery Energy Storage Demonstration Project (Phase I)

Phase I Grid Connection Date: January 2026

Location: Hubei Province

Owner: Honghu Suifa New Energy Co., Ltd. (a wholly owned subsidiary of Guangzhou Development Group)

Energy Storage Technology: Sodium-Ion Battery

Phase I Capacity: 50MW/100MWh

The project is one of Hubei Province's first batch of new energy storage demonstration projects.

Phase I includes a 50MW/100MWh sodium-ion battery energy storage system, a new 110kV booster substation, and a dedicated transmission line connecting to the Maojiang 110kV substation.

Once fully completed, the project is expected to become one of China's largest sodium-ion battery energy storage power stations, demonstrating the commercial potential of sodium-ion technology for grid-scale applications.

10

China's First 100MWh Distribution-Level Cloud Energy Storage Demonstration Project

State Grid Shandong Integrated Energy Service Cloud Energy Storage Demonstration Project

Grid Connection Date: January 2026

Location: Shandong Province

Storage Capacity: 50MW/100MWh

As China's first 100MWh cloud energy storage demonstration project, the initiative is built around the concept of distributed aggregation, cloud-based dispatch, and intelligent coordination.

The project enables centralized management and flexible dispatch of a large number of geographically distributed energy storage resources, providing an innovative solution for improving grid flexibility, renewable energy integration, and distributed energy resource management.

Milestone Projects Commissioned at the End of 2025

While a wide range of innovative energy storage projects entered operation during the first half of 2026, several landmark projects commissioned in late 2025 also deserve recognition for their technological significance. These projects span hybrid energy storage, ultra-large-scale lithium battery storage, semi-solid-state battery systems, intelligent string-based energy storage, and other cutting-edge applications, further demonstrating China's accelerating innovation in the energy storage sector.

11

China's First 100MW-Scale Hybrid Energy Storage Demonstration Project Combining Supercapacitors and Lithium Batteries

Shunde Demonstration Base Project of the Guangdong New-type Energy Storage Innovation Center

Grid Connection Date: December 2025

Location: Guangdong Province

Owner: Guangdong New-type Energy Storage National Research Institute Co., Ltd.

Energy Storage Technology: Supercapacitors + Lithium Iron Phosphate (LFP) Batteries

Storage Capacity: 200MW/305MWh

As China's first commercial-scale demonstration project integrating supercapacitors and lithium batteries, the project validates the technical and commercial viability of hybrid energy storage systems at the 100MW scale.

The project utilizes domestically developed high-energy-density, high-power supercapacitors (90Wh/kg with a service life exceeding 100,000 charge-discharge cycles) and adopts a hybrid configuration consisting of 50MW/5MWh of supercapacitors and 150MW/300MWh of LFP battery storage.

By combining the ultra-fast response capability of supercapacitors with the long-duration energy support of lithium batteries, the system provides multiple grid services, including grid-forming support, primary and secondary frequency regulation, and sustained energy balancing, offering a comprehensive solution for next-generation power systems.

12

China's Largest Intelligent String Energy Storage Power Station by Single-Site Capacity

220kV Boxian Xingguang Energy Storage Power Station

Grid Connection Date: December 2025

Location: Inner Mongolia Autonomous Region

Owner: Baotou Boxian New Energy Technology Co., Ltd. (a wholly owned subsidiary of HyperStrong)

Energy Storage Technology: Lithium Iron Phosphate (LFP) Batteries

Storage Capacity: 400MW/2,400MWh

With a total capacity of 400MW/2,400MWh, the project is China's largest intelligent string energy storage power station by single-site capacity.

Developed by HyperStrong, the project features Huawei's intelligent string grid-forming PCS alongside HyperStrong's industry-leading 7MWh high-capacity battery energy storage system, enhancing system safety, operational flexibility, and grid support capability.

13

China's Largest Independent Grid-side Energy Storage Demonstration Project

Baotou Weijun 500MW/3,000MWh Independent Grid-side Energy Storage Demonstration Project

Grid Connection Date: December 2025

Location: Inner Mongolia Autonomous Region

Owner: Baotou Tuyou Banner Bosi New Energy Technology Co., Ltd. (a wholly owned subsidiary of HyperStrong)

Energy Storage Technology: Lithium Iron Phosphate (LFP) Batteries

Storage Capacity: 500MW/3,000MWh

Located in Tumed Right Banner, Baotou, Inner Mongolia, the project is currently China's largest independent grid-side energy storage demonstration project.

Serving as a flagship project for China's new power system development, it also plays a vital role in facilitating renewable energy integration across western Inner Mongolia while strengthening regional grid stability and flexibility.

14

World's Largest Single-Site Electrochemical Energy Storage Power Station

Envision Chaganhada Energy Storage Power Station

Grid Connection Date: December 2025

Location: Inner Mongolia Autonomous Region

Owner: Envision Group

Energy Storage Technology: Lithium Iron Phosphate (LFP) Batteries

Storage Capacity: 1,000MW/4,000MWh

Located in Bayannur, Inner Mongolia, the project has a total storage capacity of 4GWh, making it the world's largest single-site electrochemical energy storage power station.

The facility is fully equipped with Envision's AI-powered energy storage system, enabling intelligent operation and maintenance while successfully passing the grid's stringent "three-charge, three-discharge" commissioning test on its first attempt.

15

China's Largest Standalone New-type Energy Storage Power Station by Single-Site Capacity

Tongliao Hailuo 500MW/2,000MWh Standalone Energy Storage Power Station

Grid Connection Date: November 2025

Location: Inner Mongolia Autonomous Region

Owner: Tongliao Conch New Energy Co., Ltd. (a wholly owned subsidiary of Anhui Conch Group)

Energy Storage Technology: Lithium Iron Phosphate (LFP) Batteries

Storage Capacity: 500MW/2,000MWh

Located in Naiman Banner, Tongliao, Inner Mongolia, the project was developed by Tongliao Conch New Energy Co., Ltd.

The station adopts CATL's 5MWh battery energy storage system and, at the time of commissioning, became China's largest standalone new-type energy storage power station by single-site capacity.

16

China's Largest Semi-solid-state Lithium Battery Energy Storage Project

Wuhai 200MW/800MWh Semi-solid-state Energy Storage Power Station

Grid Connection Date: November 2025

Location: Inner Mongolia Autonomous Region

Owner: China Green Development Investment Group

Energy Storage Technology: Semi-solid-state Lithium Iron Phosphate Batteries

Storage Capacity: 200MW/800MWh

With a total investment of approximately RMB 600 million, the project is the first utility-scale energy storage project in Inner Mongolia to deploy semi-solid-state LFP battery technology.

Occupying approximately 100 mu (about 6.7 hectares), the facility comprises 160 battery containers and 40 integrated PCS and step-up transformer units, providing valuable engineering validation for the commercialization of next-generation battery technologies.

A review of China's landmark energy storage projects commissioned in recent years clearly demonstrates that the industry has entered a new stage of development. Rather than relying solely on expanding lithium battery deployment, China's energy storage market is rapidly evolving toward technology diversification, complementary short- and long-duration storage solutions, and full-spectrum applications spanning the generation, grid, and demand sides.

Emerging technologies—including long-duration energy storage, solid-state batteries, hybrid energy storage systems, intelligent aggregation, and cloud-based dispatch—are continuously advancing from engineering demonstrations to large-scale commercial deployment. At the same time, integrated energy solutions combining multiple renewable resources and storage technologies are becoming increasingly common across utility-scale, grid-side, and customer-side applications.

Driven by supportive policies, growing market demand, and sustained investment, China's energy storage industry is expected to continue overcoming technological and commercial barriers. The sector is steadily building a multi-level, diversified, and highly efficient energy storage ecosystem, accelerating the industrialization of advanced storage technologies while providing critical support for the country's energy transition and the development of a modern power system.

Dalian Institute of Chemical Physics Wins Second Prize of National Technical Invention Award for Next-Generation Large-Scale All-Vanadium Flow Battery Core Technologies & Applications

On the morning of July 8, the National Science and Technology Awards Ceremony, the General Assembly of the Chinese Academy of Sciences and the Chinese Academy of Engineering, and the 11th National Congress of the China Association for Science and Technology convened in Beijing.

As China’s highest honor in science and technology, the National Science and Technology Awards cover five categories: the State Preeminent Science and Technology Award, the National Natural Science Award, the National Technical Invention Award, the National Science and Technology Progress Award, and the International Science and Technology Cooperation Award of the People’s Republic of China.

The research achievement titled Key Technologies and Applications of Next-Generation Large-Scale All-Vanadium Flow Batteries developed by the Dalian Institute of Chemical Physics (DICP), Chinese Academy of Sciences, was conferred the Second Prize of the National Technical Invention Award.

DICP is the initiator institution of the Flow Battery Special Committee under the China Energy Storage Alliance (CNESA). Researcher Li Xianfeng, Deputy Director of DICP, serves as the first Chairman of the Special Committee. CNESA hereby extends our sincerest respect and warmest congratulations to Researcher Li Xianfeng and his entire R&D team.

Energy storage acts as an indispensable core technology for building a new power system dominated by renewable energy and delivering China’s Dual Carbon Goals. Featuring ultra-long service life, intrinsic high safety and outstanding energy efficiency, all-vanadium redox flow batteries (VRFBs) have emerged as a high-priority technical pathway for global energy storage and a top choice for large-scale energy storage deployment in China.

Nevertheless, all-vanadium flow battery systems boast sophisticated architectures that integrate multiple interdisciplinary disciplines. Efficient collaborative integration of diverse internal materials and functional components poses substantial challenges to system assembly and engineering implementation.

For more than a decade, the research team led by Researcher Li Xianfeng from DICP has dedicated itself to flow battery innovation. After completing MW-scale system demonstration and validation back in 2012, the team systematically resolved critical industrialization bottlenecks including high manufacturing costs, insufficient operational reliability, and foreign monopolies over core materials. Through sustained original innovation, the team pioneered the complete set of next-generation core technologies for large-scale all-vanadium flow batteries.

The team put forward the original concept of "ion sieving conduction", which underpinned the independent R&D and mass production of proprietary ion exchange membranes. Breakthroughs were also realized in novel electrolyte formulations, high-performance cell stacks and full system integration. Relying on these foundational principal innovations and core technical advances, the team established a fully independent industrialization chain for all-vanadium flow batteries, spanning fundamental research through full-scale commercial engineering.

Over the past five years, the team has deployed more than 30 commercial demonstration projects worldwide based on its proprietary next-generation VRFB technologies. Flagship projects include the world’s first national-grade 100 MW / 400 MWh all-vanadium flow battery peak-shaving power station, and the world’s largest ongoing 200 MW / 1 GWh PV-storage integrated project in Jimsar, Xinjiang. To date, the cumulative installed capacity of the team’s VRFB technologies has exceeded 4 GWh, capturing a dominant share of the global mainstream flow battery market.

The award-winning achievement has built a robust independent intellectual property portfolio, encompassing over 200 authorized invention patents including 12 international patents. A total of 15 patent licensing agreements has been signed with domestic and overseas enterprises, marking successful technology exports to developed European economies.

Furthermore, the team led the formulation and release of the world’s first international standard for flow batteries, alongside more than 20 national and industrial standards, securing China’s rule-setting dominance across the global flow battery sector.

This landmark research outcome was jointly completed by the Dalian Institute of Chemical Physics, Dalian Rongke Power Co., Ltd., and Dalian Rongke Power Group Co., Ltd. The technology has catalyzed a complete upstream and downstream industrial cluster with remarkable agglomeration effects, delivering pivotal support for technological advancement in China’s energy storage sector, the growth of the new energy industry, and the structural transformation of national energy systems.

Two Pioneering Figures in China’s Energy Storage Sector Win Top National Science and Technology Honors at the 2025 National Science and Technology Awards

A landmark moment for China’s energy storage industry unfolded at the 2025 China National Science and Technology Awards Ceremony, held in Beijing on July 8, 2026. Two trailblazing scientists who have shaped the trajectory of China’s energy storage technology received the nation’s most prestigious scientific recognitions, marking a historic milestone for domestic long-duration energy storage and lithium-ion battery innovation.

Academician Chen Liquan, a researcher at the Institute of Physics, Chinese Academy of Sciences, and the founding father of China’s lithium battery industry, was honored with the National Highest Science and Technology Award—the country’s supreme honor for scientific and technological contributions. As a pioneer and global leading authority on lithium battery technologies, Academician Chen Liquan laid the foundational framework for China’s lithium-ion battery industrial system, spearheading breakthroughs in basic materials, cell manufacturing and industrialization over decades of research. His lifelong work underpins the rapid growth of China’s electrochemical energy storage, power battery and new energy vehicle sectors, laying irreplaceable technical groundwork for the national dual carbon strategy and energy transition revolution.

Meanwhile, Prof. Chen Haisheng, Chairman of China Energy Storage Alliance (CNESA) and researcher at the Institute of Engineering Thermophysics, Chinese Academy of Sciences, led his research team to claim the Second Prize of the National Technology Invention Award for the landmark achievement Key Technologies for Large-Scale Advanced Compressed Air Energy Storage (CAES) Systems.

Energy storage stands as a core, indispensable supporting technology for China’s dual carbon goals and national energy revolution. Compressed Air Energy Storage (CAES) is widely recognized as one of the most promising long-duration bulk energy storage solutions worldwide, featuring large installation scale, low lifecycle cost, ultra-long service life and outstanding operational safety, and has become a strategically competitive technical field across all major economies. Traditional CAES systems have long been restrained by critical bottlenecks including fossil fuel dependency and low round-trip efficiency, severely limiting large-scale commercial rollout globally.

Supported by successive national key research programs including the National Basic Research Program (973), National High-Tech R&D Program (863) and National Key R&D Program, Prof. Chen Haisheng’s team dedicated 20 consecutive years to targeted research and iterative breakthroughs, delivering a full set of systematic original innovations that resolve historic pain points of conventional CAES technology:

1. Proposed the novel "storage-release correspondence & cycle matching" design theory for energy storage systems, and invented an advanced CAES architecture based on a homologous circulation principle;

2. Overcame the synergistic aerodynamic and structural design challenge for multi-stage compressors and expanders, developing ultra-high pressure ratio-compressors and ultra-high expansion ratio expanders with fully independent intellectual property rights;

3. Cracked core technical barriers for supercritical heat/cold storage heat exchangers, inventing high-efficiency compact heat exchange equipment for CAES systems.

The research team has completed the construction of the world’s first series of advanced CAES demonstration facilities covering 1.5MW, 10MW, 100MW and 300MW capacity levels. The round-trip efficiency of the flagship system exceeds 70%, repeatedly setting new global performance benchmarks and firmly establishing China’s world-leading position in advanced compressed air energy storage technology.

To date, the project has secured 162 authorized invention patents (including 9 international patents), ranking No.1 globally in CAES patent holdings and forming a high-value, tightly integrated patent portfolio. The team has published 267 SCI papers, which have accumulated over 13,700 SCI citations, demonstrating profound academic influence in the global energy storage research community. Industrial transformation of the core technologies has generated direct economic benefits exceeding 7 billion RMB, delivering tangible value for the large-scale commercialization of long-duration energy storage.

The National Science and Technology Awards consist of five major categories: the National Highest Science and Technology Award, National Natural Science Award, National Technology Invention Award, National Science and Technology Progress Award, and China International Science and Technology Cooperation Award, representing the highest official recognition of scientific innovation in China.

CNESA extends sincere congratulations to Academician Chen Liquan and Prof. Chen Haisheng’s research team on their extraordinary accomplishments. These top-tier national honors fully validate the core strategic value of energy storage technologies in advancing global low-carbon energy transition, and highlight the strength of sustained independent innovation among China’s energy storage scientific community. As energy storage evolves into a critical backbone of the global net-zero energy system, CNESA will continue to unite industrial, academic and research stakeholders to accelerate technology iteration, industrial standardization and global cooperation, further boosting the high-quality development of China’s energy storage industry and contributing Chinese solutions to worldwide energy transformation.

China Energy Storage Tenders & Awards H1 2026: System and EPC Prices Rebound Across the Board, with 4-Hour ESS Seeing Stronger Growth than 2-Hour Systems

According to incomplete statistics from the CNESA Datalink Global Energy Storage Database, China's new energy storage tendering and award market maintained strong momentum in the first half (H1) of 2026.

During the period, 1,987 new energy storage tender notices were tracked, up 41.8% year-on-year (YoY), while 1,504 contract awards were recorded, representing a 61.0% YoY increase. The projects covered the entire energy storage value chain, including EPC contracting, energy storage systems (ESS), battery cells, battery packs, PCS, EMS, and BMS.

The ESS tender market showed a clear divergence between power and energy capacity. Tendered power reached 24.5 GW, down 3.4% YoY, while tendered energy capacity surged to 148.1 GWh, an 88.3% YoY increase. The combination of slightly lower power capacity and significantly higher energy capacity indicates the continued market shift toward longer-duration energy storage systems.

Meanwhile, EPC tender and award volumes more than doubled year-on-year, significantly outpacing the growth of standalone ESS equipment procurement. This suggests that the market is increasingly favoring turnkey EPC solutions rather than purchasing storage equipment alone.

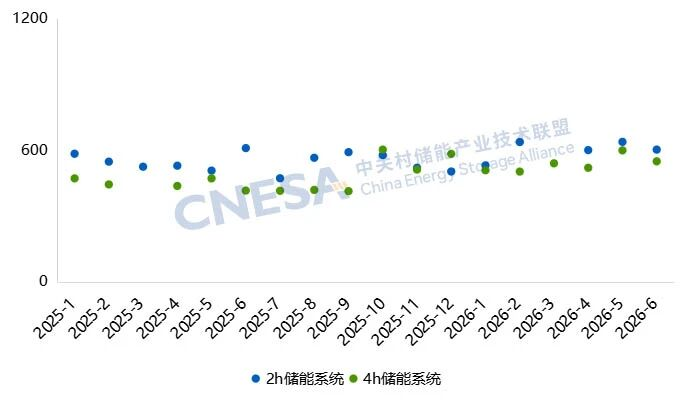

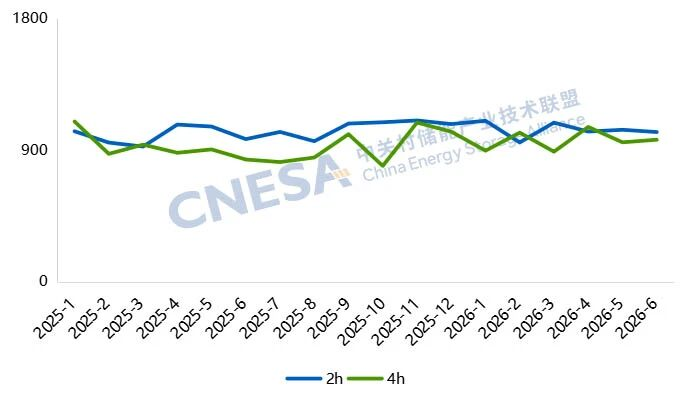

On pricing, the average winning bid price for 2-hour ESS increased to RMB 602.1 CNY/kWh, up 8.8% YoY, while the average price for 4-hour ESS reached RMB 541.3 CNY/kWh, representing a 21.1% YoY increase. Despite the stronger price growth, 4-hour systems remained less expensive per kWh than 2-hour systems, highlighting their advantages in economies of scale and lower levelized storage costs.

In terms of procurement models, centralized procurement and framework agreements have become standard industry practice. During H1 2026, centralized/framework procurement accounted for 80.6 GWh of ESS tenders, representing more than half of the total tendered capacity, further concentrating market orders among leading suppliers.

01

Tender Market Overview (H1 2026)

Tender Market Scale Overview (H1 2026)

In June 2026, ESS tenders totaled 6.1 GW / 48.3 GWh, representing a 58.5% decline in power capacity but a 37.4% increase in energy capacity compared with the same period last year. Compared with May, power capacity decreased 12.7%, while energy capacity increased 118.1%.

For the first six months of 2026, cumulative ESS tenders reached 24.5 GW / 148.1 GWh, representing -3.4% YoY in power capacity and +88.3% YoY in energy capacity.

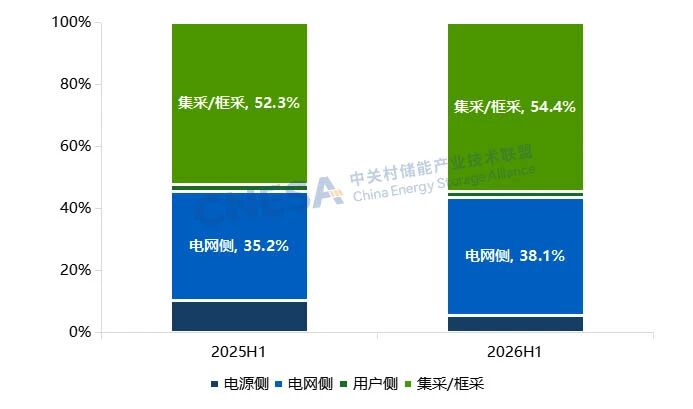

Among these, centralized procurement and framework agreements accounted for 80.6 GWh, up 96% YoY, representing 54.4% of the total tendered ESS energy capacity.

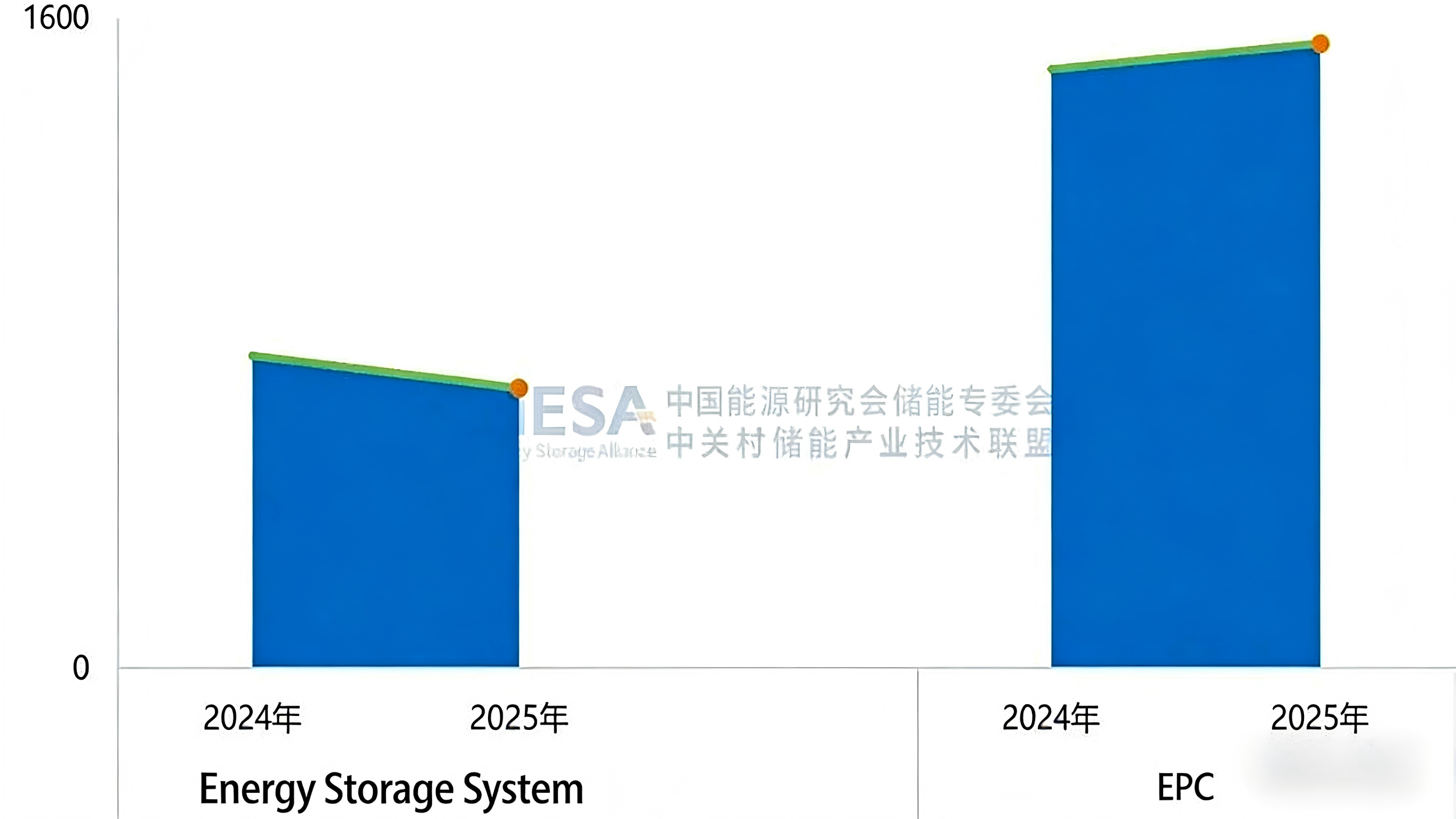

EPC Projects (Including PC)

In June 2026, EPC (including PC) tenders reached 19.3 GW / 56.4 GWh, up 111.7% YoY in power capacity and 154.4% YoY in energy capacity. Month-on-month growth reached 41.8% and 43.2%, respectively.

From January to June 2026, cumulative EPC (including PC) tenders totaled 80.1 GW / 227.9 GWh, representing 98.72% YoY growth in power capacity and 112.21% YoY growth in energy capacity.

Among them, grid-side EPC projects accounted for 200.9 GWh, increasing 145.8% YoY and representing 88.2% of the total EPC tendered energy capacity.

Blue: ESS Green: EPC

Figure 1. ESS and EPC Tender Volumes, January 2025–June 2026 (GWh)

Source: CNESA Datalink Global Energy Storage Database

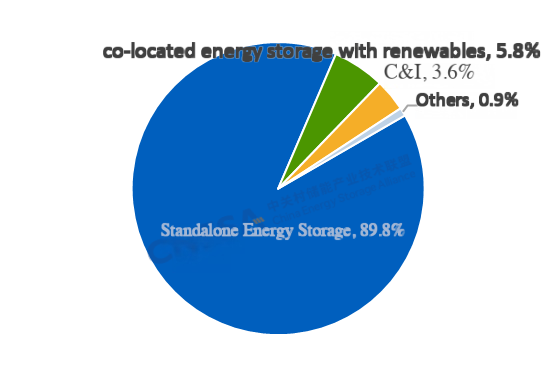

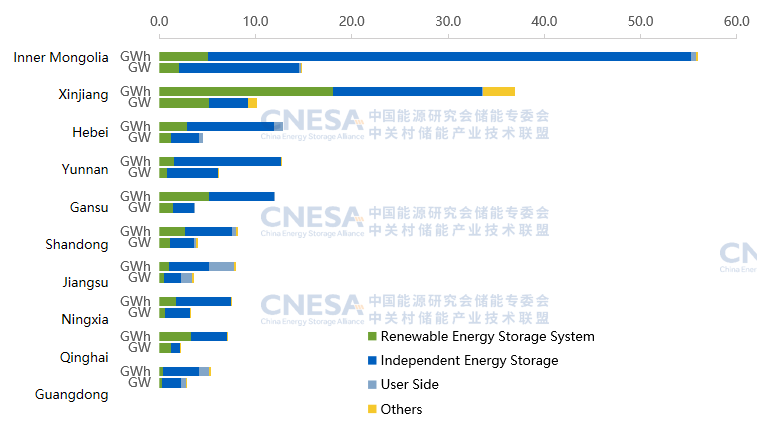

Distribution of ESS Tender Capacity by Application Scenario (H1 2026):

Based on application scenarios, total ESS tendered energy capacity reached 148.1 GWh during H1 2026.

· Centralized procurement/framework agreements accounted for 80.6 GWh, representing 54.4% of total tendered capacity.

· Grid-side projects totaled 56.4 GWh, of which 99.6% consisted of standalone energy storage projects.

· Power generation-side projects reached 8.1 GWh, with solar-plus-storage and wind-plus-storage accounting for a combined 88.4% of this segment.

From left to right:Generation-side,Grid-side,Behind-the-Meter (BTM),

Centralized Procurement / Framework Agreements

Figure 2. Distribution of ESS Tender Capacity by Application Scenario, H1 2025 vs. H1 2026 (GWh, %)

Note: Since centralized procurement and framework agreements have not yet identified their final application scenarios, they are categorized separately.

Source: CNESA Datalink Global Energy Storage Database

02

Contract Awards (H1 2026)

Awarded Project Scale Overview (H1 2026)

In June 2026, awarded ESS projects reached 4.7 GW / 13.8 GWh, representing year-on-year growth of 364.9% in power capacity and 341.1% in energy capacity. Compared with May, awarded power capacity increased 53.5%, while energy capacity rose 9.1%.

During H1 2026, cumulative ESS awards totaled 15.0 GW / 96.1 GWh, representing 37.2% YoY growth in power capacity and 12.15% YoY growth in energy capacity.

Centralized procurement and framework agreements accounted for 58.0 GWh, representing 60.1% of total awarded ESS energy capacity, although this figure was 2.13% lower than the same period last year.

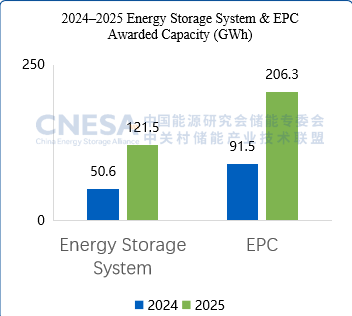

EPC Projects (Including PC)

In June 2026, EPC (including PC) awards reached 12.5 GW / 32.3 GWh, increasing 54.3% YoY in power capacity and 87.4% YoY in energy capacity.

Cumulative EPC awards during H1 2026 totaled 56.8 GW / 165.6 GWh, representing 91.87% YoY growth in power capacity and 105.96% YoY growth in energy capacity.

Among these, grid-side projects accounted for 146.5 GWh, up 129.8% YoY, representing 88.5% of the total awarded EPC energy capacity.

Blue:ESS Green:EPC

Figure 3. ESS and EPC Awarded Capacity, January 2025–June 2026 (GWh)

Source: CNESA Datalink Global Energy Storage Database

ESS Winning Bid Price Analysis (H1 2026):

Overall ESS winning bid prices increased compared with the same period last year, with the overall pricing range shifting upward.

l For 2-hour ESS, the average winning bid price during H1 2026 reached RMB 602.1/kWh, up 8.8% YoY, with prices ranging from RMB 489.0/kWh to RMB 836.0/kWh.

l For 4-hour ESS, the average winning bid price reached RMB 541.3/kWh, representing 21.1% YoY growth, with prices ranging between RMB 420.0/kWh and RMB 781.8/kWh.

Compared with H1 2025, pricing ranges for both 2-hour and 4-hour ESS widened significantly, indicating greater pricing dispersion across projects and increasing differences among market quotations.

Notably, 0.25C ESS experienced the most significant increase in price dispersion, with its pricing range expanding by 108.2% year-on-year.

Although average prices for both 2-hour and 4-hour ESS continued to rise compared with last year, monthly average winning bid prices during H1 2026 indicate that the pace of price increases has gradually stabilized.

Blue: 2-hour ESS Green: 4-hour ESS

Figure 5. Average Winning Bid Prices for ESS, January 2025–June 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, RMB/kWh)

Source: CNESA Datalink Global Energy Storage Database

EPC Winning Bid Price Analysis (Excluding PC) (H1 2026):

Average EPC winning bid prices (excluding PC) also increased compared with H1 2025.

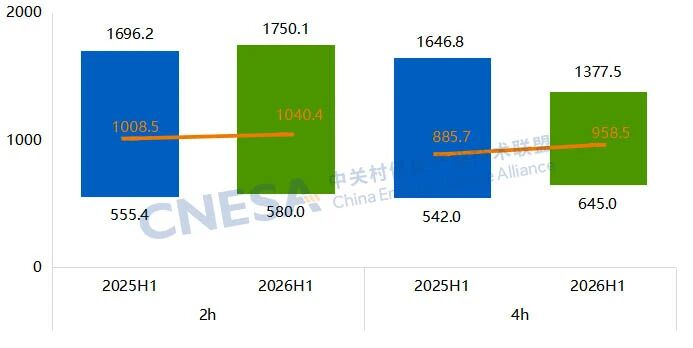

l For 2-hour EPC projects, the average winning bid price reached RMB 1,040.4/kWh, up 3.2% YoY, with prices ranging from RMB 580.0/kWh to RMB 1,750.1/kWh.

l For 4-hour EPC projects, the average winning bid price reached RMB 958.5/kWh, representing an 8.2% YoY increase, with prices ranging between RMB 645.0/kWh and RMB 1,377.5/kWh.

Regarding price distribution, both the highest and lowest prices for 2-hour EPC projects increased slightly compared with last year.

For 4-hour EPC projects, market quotations became more concentrated. Exceptionally high bids declined, while lower-end prices increased, indicating that pricing is gradually converging toward a more consistent market range and bid pricing has become increasingly standardized.

Figure 6. Winning Bid Price Ranges for 2-Hour and 4-Hour EPC Projects (Excluding PC), H1 2025 vs. H1 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, CNY/kWh)

Source: CNESA Datalink Global Energy Storage Database

Figure 7. Average Winning Bid Prices for EPC Projects (Excluding PC), January 2025–June 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, CNY//kWh)

Source: CNESA Datalink Global Energy Storage Database

The Fourth China-Europe Energy Technology Innovation Cooperation Forum:Energy Storage Sub-Forum Successfully Held in Chengdu

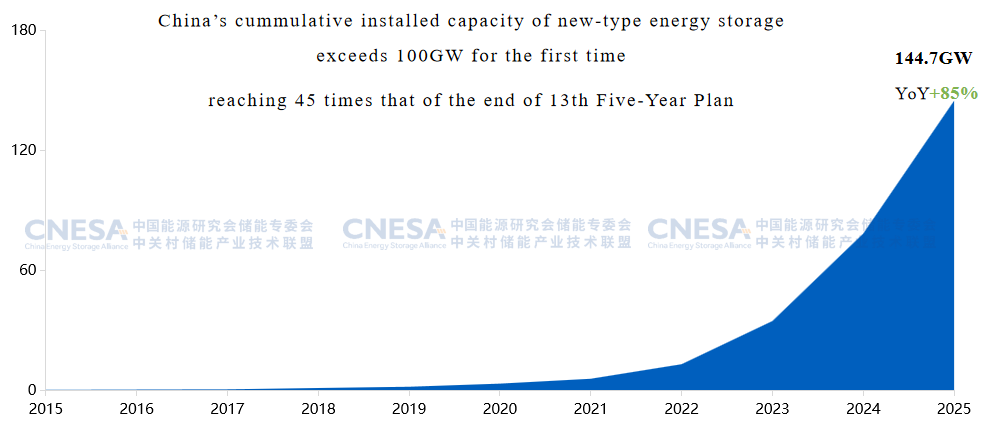

China's installed capacity of new-type energy storage has reached 157 GW, ranking first globally for four consecutive years. Germany has received grid connection applications exceeding 720 GW for large-scale storage, signaling an explosion in the European energy storage market.

On June 25, the Fourth China-Europe Energy Technology Innovation Cooperation Forum: Energy Storage Sub-forum was held in Chengdu, Sichuan, unfolding a panoramic view of China-Europe energy storage collaborative innovation. The sub-forum was co-hosted by the China-Europe Energy Innovation Cooperation Office and the China Energy Storage Alliance (CNESA).

Representatives from government agencies, industry associations, research institutions, and leading enterprises from China, the UK, France, Germany, Denmark, the Netherlands, Switzerland, and other countries gathered at the event, forming a high-end multi-national lineup spanning government, industry, academia, and research. The session was moderated by Li Zhen, Deputy Secretary-General of CNESA.

Concurrent events included Country Days for the UK, Iceland, and Finland, as well as thematic sub-forums on hydrogen energy, smart energy, wind power, and biomass energy, establishing a premier China-Europe exchange platform covering diverse new energy sectors.

【Key Highlights】

① China Leads Global Storage: As of May 2026, China's cumulative installed capacity of new-type energy storage reached 157 GW, a surge of over 45 times compared to the end of the 13th Five-Year Plan period, maintaining the global top spot for new additions for four straight years.

② European Large-Scale Storage Poised for Takeoff: Germany has over 720 GW of grid connection applications for large-scale storage, with authorities initially approving 78 GW. The UK plans to deploy no less than 23 GW of grid-scale battery storage and over 4 GW of long-duration storage by 2030.

③ Chinese Enterprises Enter New Phase of Globalization: CALB has broken ground on a 100 GWh industrial base in Portugal, marking a shift from product export to full value-chain localization.

④ New Consensus on China-Europe Cooperation: Lithium-ion batteries and hydrogen energy are complementary; AI is deeply empowering storage; and standards mutual recognition has become an industry imperative—China-Europe cooperation is evolving from "complementary strengths" to "symbiotic prosperity."

Policy Direction:

New-Type Energy Storage: A Critical Pillar of the New Energy System

Zhang Jianwei

First-Level Researcher, Department of Science, Technology and Equipment, National Energy Administration (NEA)

Zhang Jianwei, First-Level Researcher, Department of Science, Technology and Equipment, National Energy Administration (NEA), stated in his opening remarks that the Chinese government attaches great importance to energy storage development. The NEA coordinates an "effective market" with a "proactive government," promoting high-quality development in the sector through four key measures:

First, strengthening planning guidance.Jointly issuing multiple supportive policies with relevant departments to clarify development directions and tasks.

Second, persisting in innovation-driven development. Organizing pilot projects to explore over ten technological routes and continuously improving the standards system, having released over 50 national standards.

Third, refining market mechanisms.Clarifying market entity roles, improving pricing mechanisms, electricity spot markets, capacity compensation, and other market-based mechanisms to expand revenue streams.

Fourth, deepening international cooperation.Actively supporting Chinese enterprises going global. He noted that the 15th Five-Year Plan period presents both opportunities and challenges.Considering demands such as renewable energy integration and power system security, as well as the evolving role of coal power, the NEA will continue to target high-quality development to comprehensively support carbon peaking goals and contribute Chinese strength to the global energy transition.

Wang Shunchao

Vice President, International Energy Consulting Department,

China Electric Power Planning & Engineering Institute (EPPEI)

Wang Shunchao, Vice President, International Energy Consulting Department, China Electric Power Planning & Engineering Institute (EPPEI) ,emphasized in his address that energy storage is transforming from a traditional "shifting role" in power regulation to a critical technology for new power systems, undertaking diversified system service functions.