July | Monthly Project Tracker of New Energy Storage | Newly Commissioned User-Side New Energy Storage Projects +9% Year-on-Year, -41% Month-on-Month, East China Holds Largest Market Share

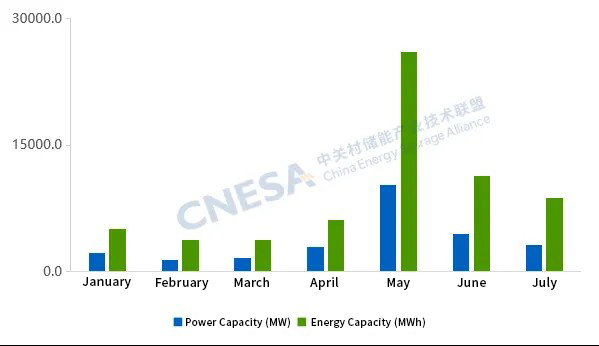

According to the incomplete statistics of the CNESA DataLink Global Energy Storage Database, in July 2025, the total newly commissioned capacity of domestic new energy storage projects was 3.24GW/8.79GWh, a year-on-year decrease of -35%/-26% and a month-on-month decrease of -28%/-23%. Affected by the “rush installation” of new energy, the newly added capacity of new energy storage continued the downward trend since “May 30.” The newly added capacity in July continued to decline, with a drop about 10 percentage points greater than the same period last year.

Figure 1: January–July 2025 Installed Capacity of Newly Commissioned New Energy Storage Projects in China

Data Source: CNESA DataLink Global Energy Storage Database https://www.esresearch.com.cn/

Since June this year, we have been publishing monthly updates on new energy storage projects by application market, dividing them into power source & grid side and user side. The following is the user-side new energy storage project installation landscape for July.

In July, user-side newly installed capacity was 252.3MW/529.7MWh, a year-on-year change of +9%/-1% and a month-on-month change of -41%/-49%.

User-side new energy storage project installations showed the following characteristics.

1. C&I Energy Storage Dominated, with Emergency Power Assurance Functions Becoming Prominent

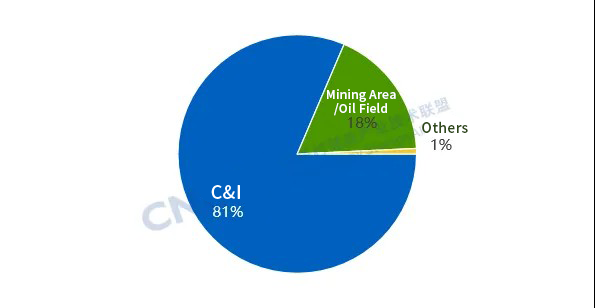

In July, the user-side energy storage market was dominated by C&I applications. Newly installed capacity in C&I scenarios reached 205.4MW/435.7MWh, a year-on-year change of -3%/-11%. Projects owned by high energy-consuming enterprises such as chemical, cement, and metallurgy accounted for 40% of the total, with the emergency power assurance role of user-side energy storage becoming increasingly prominent.

On the technical side, all newly commissioned projects adopted electrochemical energy storage technology, with lithium iron phosphate battery technology accounting for nearly 100% of installed power capacity. In addition, one vanadium redox flow battery C&I energy storage project was completed and put into operation.

Figure 2: Application Distribution of Newly Commissioned User-Side New Energy Storage Projects in July 2025 (MW%)

Data Source: CNESA DataLink Global Energy Storage Database https://www.esresearch.com.cn/

Note: “C&I” includes industry, industrial parks, and commercial buildings; “Others” includes EV charging stations, municipal utilities, and island.

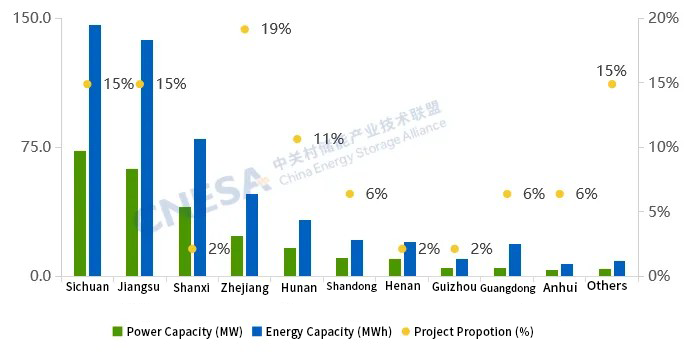

2. East China User-side Energy Storage Market Active, Sichuan Recorded the Largest Newly Installed Capacity

From the perspective of regional distribution, newly commissioned projects were mainly concentrated in 15 provinces including Sichuan, Jiangsu, Shanxi, Zhejiang, and Hunan. In terms of project numbers, the East China region (Zhejiang, Jiangsu, Shandong, etc.) held the largest market share, with nearly half of the country’s new projects, and Zhejiang accounted for nearly one-fifth of the national total, ranking first nationwide.

In terms of installed capacity, Sichuan recorded the largest increase, accounting for nearly 30% of the national total; Jiangsu followed, ranking first in East China. In July, Sichuan Power Grid Power Trading Center issued the “2025 User-Side New Energy Storage Project-Related Matters,” which clarified that energy storage operation revenue consists of two parts: peak-valley fluctuation revenue and storage discharge compensation fees, providing a clear revenue expectation for investment and operation of user-side storage projects.

Figure 3: Provincial Distribution of Newly Commissioned User-Side New Energy Storage Projects in China, July 2025

Data Source: CNESA DataLink Global Energy Storage Database https://www.esresearch.com.cn/

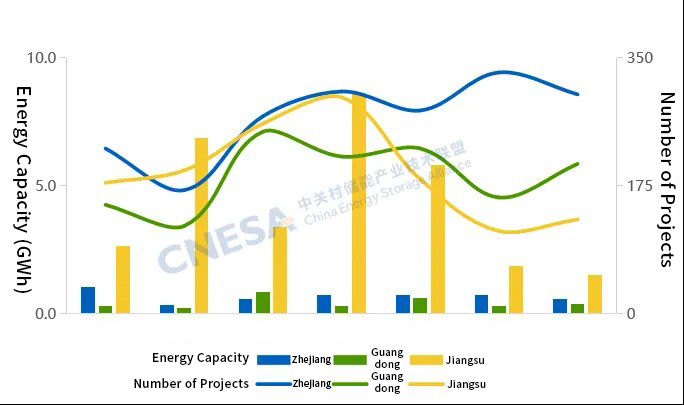

From the perspective of filed projects, since the second half of the year, overall investment enthusiasm in the user-side storage market has declined. In July, over 750 newly filed user-side storage projects were added nationwide, a year-on-year decrease of 35%, with energy capacity decreasing by 20% year-on-year.

Traditional user-side storage markets in Zhejiang, Guangdong, and Jiangsu showed sluggish growth. These three provinces recorded over 630 newly filed user-side storage projects, accounting for 84% of the national total, and remain the main market for user-side storage. However, both the number of newly filed projects and the energy capacity in these provinces were lower than the same period last year: Zhejiang -25%/-9% year-on-year, Guangdong -29%/-7%, Jiangsu -53%/-25%.

Emerging markets driven by power supply security needs are beginning to surface. Since 2025, Anhui’s user-side storage market has remained active, with the monthly number of newly filed projects consistently higher than the same period last year, and July growth exceeding 180%. In the first half of the year, Sichuan recorded 66 newly filed user-side storage projects, significantly higher than the same period last year. Henan recorded over 570 newly filed projects in the first half, a year-on-year increase of 21%.

Figure 4: Monthly Distribution of Newly Filed Storage Projects in Zhejiang, Guangdong, and Jiangsu (January–July 2025)

Data Source: CNESA DataLink Global Energy Storage Database https://www.esresearch.com.cn/