Latest News

China Energy Storage Tenders & Awards H1 2026: System and EPC Prices Rebound Across the Board, with 4-Hour ESS Seeing Stronger Growth than 2-Hour Systems

According to incomplete statistics from the CNESA Datalink Global Energy Storage Database, China's new energy storage tendering and award market maintained strong momentum in the first half (H1) of 2026.

During the period, 1,987 new energy storage tender notices were tracked, up 41.8% year-on-year (YoY), while 1,504 contract awards were recorded, representing a 61.0% YoY increase. The projects covered the entire energy storage value chain, including EPC contracting, energy storage systems (ESS), battery cells, battery packs, PCS, EMS, and BMS.

The ESS tender market showed a clear divergence between power and energy capacity. Tendered power reached 24.5 GW, down 3.4% YoY, while tendered energy capacity surged to 148.1 GWh, an 88.3% YoY increase. The combination of slightly lower power capacity and significantly higher energy capacity indicates the continued market shift toward longer-duration energy storage systems.

Meanwhile, EPC tender and award volumes more than doubled year-on-year, significantly outpacing the growth of standalone ESS equipment procurement. This suggests that the market is increasingly favoring turnkey EPC solutions rather than purchasing storage equipment alone.

On pricing, the average winning bid price for 2-hour ESS increased to RMB 602.1 CNY/kWh, up 8.8% YoY, while the average price for 4-hour ESS reached RMB 541.3 CNY/kWh, representing a 21.1% YoY increase. Despite the stronger price growth, 4-hour systems remained less expensive per kWh than 2-hour systems, highlighting their advantages in economies of scale and lower levelized storage costs.

In terms of procurement models, centralized procurement and framework agreements have become standard industry practice. During H1 2026, centralized/framework procurement accounted for 80.6 GWh of ESS tenders, representing more than half of the total tendered capacity, further concentrating market orders among leading suppliers.

01

Tender Market Overview (H1 2026)

Tender Market Scale Overview (H1 2026)

In June 2026, ESS tenders totaled 6.1 GW / 48.3 GWh, representing a 58.5% decline in power capacity but a 37.4% increase in energy capacity compared with the same period last year. Compared with May, power capacity decreased 12.7%, while energy capacity increased 118.1%.

For the first six months of 2026, cumulative ESS tenders reached 24.5 GW / 148.1 GWh, representing -3.4% YoY in power capacity and +88.3% YoY in energy capacity.

Among these, centralized procurement and framework agreements accounted for 80.6 GWh, up 96% YoY, representing 54.4% of the total tendered ESS energy capacity.

EPC Projects (Including PC)

In June 2026, EPC (including PC) tenders reached 19.3 GW / 56.4 GWh, up 111.7% YoY in power capacity and 154.4% YoY in energy capacity. Month-on-month growth reached 41.8% and 43.2%, respectively.

From January to June 2026, cumulative EPC (including PC) tenders totaled 80.1 GW / 227.9 GWh, representing 98.72% YoY growth in power capacity and 112.21% YoY growth in energy capacity.

Among them, grid-side EPC projects accounted for 200.9 GWh, increasing 145.8% YoY and representing 88.2% of the total EPC tendered energy capacity.

Blue: ESS Green: EPC

Figure 1. ESS and EPC Tender Volumes, January 2025–June 2026 (GWh)

Source: CNESA Datalink Global Energy Storage Database

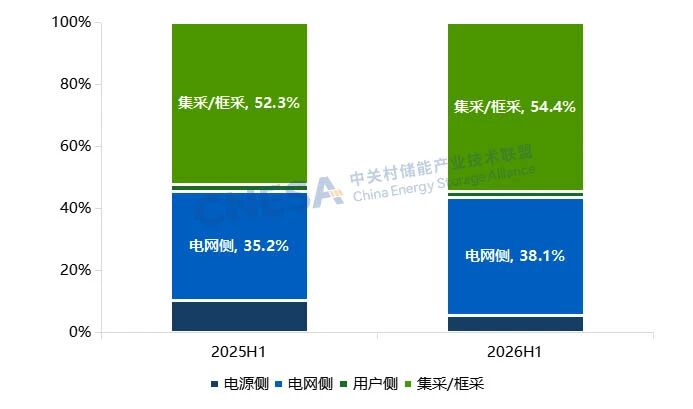

Distribution of ESS Tender Capacity by Application Scenario (H1 2026):

Based on application scenarios, total ESS tendered energy capacity reached 148.1 GWh during H1 2026.

· Centralized procurement/framework agreements accounted for 80.6 GWh, representing 54.4% of total tendered capacity.

· Grid-side projects totaled 56.4 GWh, of which 99.6% consisted of standalone energy storage projects.

· Power generation-side projects reached 8.1 GWh, with solar-plus-storage and wind-plus-storage accounting for a combined 88.4% of this segment.

From left to right:Generation-side,Grid-side,Behind-the-Meter (BTM),

Centralized Procurement / Framework Agreements

Figure 2. Distribution of ESS Tender Capacity by Application Scenario, H1 2025 vs. H1 2026 (GWh, %)

Note: Since centralized procurement and framework agreements have not yet identified their final application scenarios, they are categorized separately.

Source: CNESA Datalink Global Energy Storage Database

02

Contract Awards (H1 2026)

Awarded Project Scale Overview (H1 2026)

In June 2026, awarded ESS projects reached 4.7 GW / 13.8 GWh, representing year-on-year growth of 364.9% in power capacity and 341.1% in energy capacity. Compared with May, awarded power capacity increased 53.5%, while energy capacity rose 9.1%.

During H1 2026, cumulative ESS awards totaled 15.0 GW / 96.1 GWh, representing 37.2% YoY growth in power capacity and 12.15% YoY growth in energy capacity.

Centralized procurement and framework agreements accounted for 58.0 GWh, representing 60.1% of total awarded ESS energy capacity, although this figure was 2.13% lower than the same period last year.

EPC Projects (Including PC)

In June 2026, EPC (including PC) awards reached 12.5 GW / 32.3 GWh, increasing 54.3% YoY in power capacity and 87.4% YoY in energy capacity.

Cumulative EPC awards during H1 2026 totaled 56.8 GW / 165.6 GWh, representing 91.87% YoY growth in power capacity and 105.96% YoY growth in energy capacity.

Among these, grid-side projects accounted for 146.5 GWh, up 129.8% YoY, representing 88.5% of the total awarded EPC energy capacity.

Blue:ESS Green:EPC

Figure 3. ESS and EPC Awarded Capacity, January 2025–June 2026 (GWh)

Source: CNESA Datalink Global Energy Storage Database

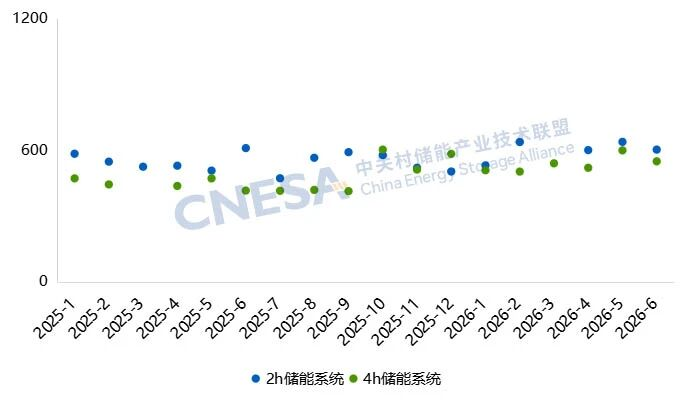

ESS Winning Bid Price Analysis (H1 2026):

Overall ESS winning bid prices increased compared with the same period last year, with the overall pricing range shifting upward.

l For 2-hour ESS, the average winning bid price during H1 2026 reached RMB 602.1/kWh, up 8.8% YoY, with prices ranging from RMB 489.0/kWh to RMB 836.0/kWh.

l For 4-hour ESS, the average winning bid price reached RMB 541.3/kWh, representing 21.1% YoY growth, with prices ranging between RMB 420.0/kWh and RMB 781.8/kWh.

Compared with H1 2025, pricing ranges for both 2-hour and 4-hour ESS widened significantly, indicating greater pricing dispersion across projects and increasing differences among market quotations.

Notably, 0.25C ESS experienced the most significant increase in price dispersion, with its pricing range expanding by 108.2% year-on-year.

Although average prices for both 2-hour and 4-hour ESS continued to rise compared with last year, monthly average winning bid prices during H1 2026 indicate that the pace of price increases has gradually stabilized.

Blue: 2-hour ESS Green: 4-hour ESS

Figure 5. Average Winning Bid Prices for ESS, January 2025–June 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, RMB/kWh)

Source: CNESA Datalink Global Energy Storage Database

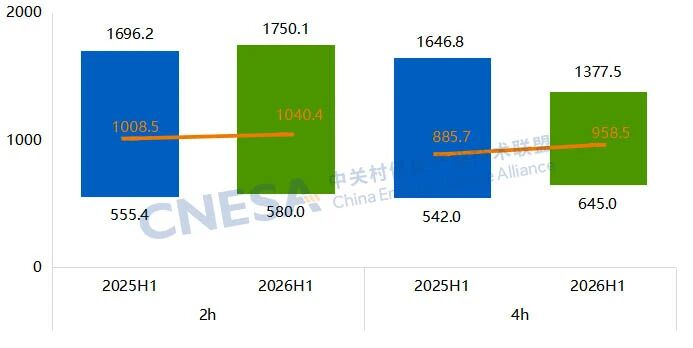

EPC Winning Bid Price Analysis (Excluding PC) (H1 2026):

Average EPC winning bid prices (excluding PC) also increased compared with H1 2025.

l For 2-hour EPC projects, the average winning bid price reached RMB 1,040.4/kWh, up 3.2% YoY, with prices ranging from RMB 580.0/kWh to RMB 1,750.1/kWh.

l For 4-hour EPC projects, the average winning bid price reached RMB 958.5/kWh, representing an 8.2% YoY increase, with prices ranging between RMB 645.0/kWh and RMB 1,377.5/kWh.

Regarding price distribution, both the highest and lowest prices for 2-hour EPC projects increased slightly compared with last year.

For 4-hour EPC projects, market quotations became more concentrated. Exceptionally high bids declined, while lower-end prices increased, indicating that pricing is gradually converging toward a more consistent market range and bid pricing has become increasingly standardized.

Figure 6. Winning Bid Price Ranges for 2-Hour and 4-Hour EPC Projects (Excluding PC), H1 2025 vs. H1 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, CNY/kWh)

Source: CNESA Datalink Global Energy Storage Database

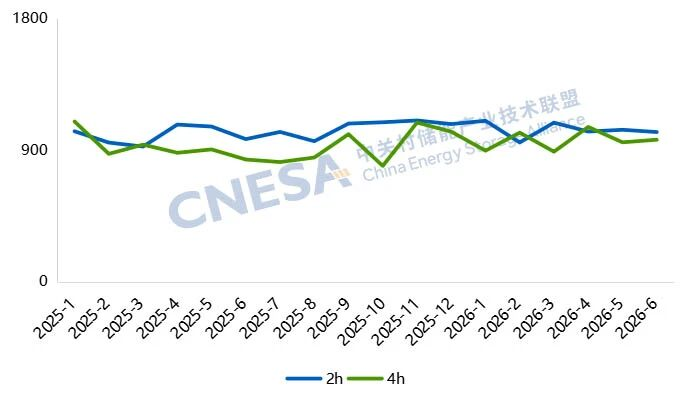

Figure 7. Average Winning Bid Prices for EPC Projects (Excluding PC), January 2025–June 2026 (Excluding Centralized Procurement/Framework Agreements and Behind-the-Meter Projects, CNY//kWh)

Source: CNESA Datalink Global Energy Storage Database

The Fourth China-Europe Energy Technology Innovation Cooperation Forum:Energy Storage Sub-Forum Successfully Held in Chengdu

China's installed capacity of new-type energy storage has reached 157 GW, ranking first globally for four consecutive years. Germany has received grid connection applications exceeding 720 GW for large-scale storage, signaling an explosion in the European energy storage market.

On June 25, the Fourth China-Europe Energy Technology Innovation Cooperation Forum: Energy Storage Sub-forum was held in Chengdu, Sichuan, unfolding a panoramic view of China-Europe energy storage collaborative innovation. The sub-forum was co-hosted by the China-Europe Energy Innovation Cooperation Office and the China Energy Storage Alliance (CNESA).

Representatives from government agencies, industry associations, research institutions, and leading enterprises from China, the UK, France, Germany, Denmark, the Netherlands, Switzerland, and other countries gathered at the event, forming a high-end multi-national lineup spanning government, industry, academia, and research. The session was moderated by Li Zhen, Deputy Secretary-General of CNESA.

Concurrent events included Country Days for the UK, Iceland, and Finland, as well as thematic sub-forums on hydrogen energy, smart energy, wind power, and biomass energy, establishing a premier China-Europe exchange platform covering diverse new energy sectors.

【Key Highlights】

① China Leads Global Storage: As of May 2026, China's cumulative installed capacity of new-type energy storage reached 157 GW, a surge of over 45 times compared to the end of the 13th Five-Year Plan period, maintaining the global top spot for new additions for four straight years.

② European Large-Scale Storage Poised for Takeoff: Germany has over 720 GW of grid connection applications for large-scale storage, with authorities initially approving 78 GW. The UK plans to deploy no less than 23 GW of grid-scale battery storage and over 4 GW of long-duration storage by 2030.

③ Chinese Enterprises Enter New Phase of Globalization: CALB has broken ground on a 100 GWh industrial base in Portugal, marking a shift from product export to full value-chain localization.

④ New Consensus on China-Europe Cooperation: Lithium-ion batteries and hydrogen energy are complementary; AI is deeply empowering storage; and standards mutual recognition has become an industry imperative—China-Europe cooperation is evolving from "complementary strengths" to "symbiotic prosperity."

Policy Direction:

New-Type Energy Storage: A Critical Pillar of the New Energy System

Zhang Jianwei

First-Level Researcher, Department of Science, Technology and Equipment, National Energy Administration (NEA)

Zhang Jianwei, First-Level Researcher, Department of Science, Technology and Equipment, National Energy Administration (NEA), stated in his opening remarks that the Chinese government attaches great importance to energy storage development. The NEA coordinates an "effective market" with a "proactive government," promoting high-quality development in the sector through four key measures:

First, strengthening planning guidance.Jointly issuing multiple supportive policies with relevant departments to clarify development directions and tasks.

Second, persisting in innovation-driven development. Organizing pilot projects to explore over ten technological routes and continuously improving the standards system, having released over 50 national standards.

Third, refining market mechanisms.Clarifying market entity roles, improving pricing mechanisms, electricity spot markets, capacity compensation, and other market-based mechanisms to expand revenue streams.

Fourth, deepening international cooperation.Actively supporting Chinese enterprises going global. He noted that the 15th Five-Year Plan period presents both opportunities and challenges.Considering demands such as renewable energy integration and power system security, as well as the evolving role of coal power, the NEA will continue to target high-quality development to comprehensively support carbon peaking goals and contribute Chinese strength to the global energy transition.

Wang Shunchao

Vice President, International Energy Consulting Department,

China Electric Power Planning & Engineering Institute (EPPEI)

Wang Shunchao, Vice President, International Energy Consulting Department, China Electric Power Planning & Engineering Institute (EPPEI) ,emphasized in his address that energy storage is transforming from a traditional "shifting role" in power regulation to a critical technology for new power systems, undertaking diversified system service functions.

Both China and Europe prioritize energy storage development. China's 15th Five-Year Plan has positioned new-type energy storage as a crucial support for the new energy system. Advanced technologies like grid-forming storage have been validated in diverse domestic scenarios and are gradually entering commercial application. Europe, meanwhile, has accumulated rich experience in market mechanism design and business model innovation while actively promoting cutting-edge R&D. The two sides boast complementary advantages, providing a global (demonstration) for energy transition. Against this backdrop, the sub-forum is timely and will strongly propel deep bilateral cooperation.

The Chinese Market:

157 GW! New-Type Storage Installations Rank First Globally for Four Years

Chen Haisheng

Chairman of CNESA and Director of the Institute of Engineering Thermophysics, Chinese Academy of Sciences (CAS)

Chen Haisheng, Chairman of CNESA and Director of the Institute of Engineering Thermophysics, Chinese Academy of Sciences (CAS),provided a systematic overview of China's latest progress and outlook in energy storage technology and industry. He noted that China's storage sector is on par with international levels, transitioning from policy-driven to market-driven growth, moving from scale expansion to comprehensive commercialization, with storage emerging as a core entity in the new power system. Currently, multiple technology routes are breaking through in parallel, with long-duration storage, grid-forming storage, solid-state batteries, and AI-integrated storage becoming R&D hotspots.China has led the world in new installations for four consecutive years. As of May 2026, cumulative installed capacity of new-type storage reached 157 GW, a surge of over 45 times since the end of the 13th Five-Year Plan. The compound annual growth rate for the next five years is projected at 20.7–25.5%, with total installed capacity expected to reach 371.2–450.7 GW by 2030.

The European Market:

Large-Scale Storage Explosion & Policy Breakthroughs for Long-Duration Storage

Vincent Fremery

Energy Advisor, Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ)

Vincent Fremery, Energy Advisor, Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ),presented a keynote report titled "German Energy Storage Policy and Market." Mr. Fremery highlighted Germany's significant progress in energy transition, with renewables accounting for over 60% of power generation. Germany aims for net-zero by 2045 and 80% renewable share by 2030, planning to phase out coal by 2038. Regarding the storage market, Germany exhibits a pattern of "household storage dominance, steady growth in C&I storage, and accelerated explosion in utility-scale storage": Household storage remains dominant but growth is slowing; the C&I storage market is steadily expanding; large-scale storage (including pumped hydro) is rapidly rising, with market revenues expected to increase 2–3 times between 2025–2026. Notably, grid operators report over 720 GW of grid connection applications for large-scale storage, with 78 GW initially approved by grid companies, indicating vast development space in the next five years.

Vincent specifically mentioned that the entry of Chinese manufacturers has significantly reduced storage costs, facilitating the implementation of large-scale German projects. He noted that the new German government has yet to issue specific storage policies, leaving broad potential for Sino-German cooperation.

Bea Swords

Senior Policy Advisor, Industrial Policy & Supply Chain Strategy, Clean Energy Investment Directorate, Department for Energy Security and Net Zero (DESNZ), UK

Bea Swords, Senior Policy Advisor, Industrial Policy & Supply Chain Strategy, Clean Energy Investment Directorate, Department for Energy Security and Net Zero (DESNZ), UK,shared insights on UK storage policies, industry status, and medium-to-long-term plans. She stated that the UK targets power sector decarbonization by 2030 and net-zero emissions by 2050, where flexible power systems are key, with storage playing a central supporting role. Currently, the UK operates 7.3 GW of grid-scale battery storage and 2.8 GW of pumped hydro. It plans to deploy no less than 23 GW of grid-scale battery storage and over 4 GW of long-duration storage by 2030.The government is removing barriers through measures like eliminating "double charging" of grid fees, lowering market entry thresholds, and reducing taxes on residential storage. Crucially, it has introduced a revenue floor and cap investment support mechanism for long-duration storage exceeding 8 hours to address high upfront costs and long payback periods.

Corporate Practices:

From Product Export to Full Value-Chain Localization

Pei Yang

VP of Sales ESS, CALB Group Co., Ltd.,

Pei Yang , VP of Sales ESS, CALB Group Co., Ltd.,presented a report titled "The Energy Revolution in Zero-Carbon Cities." He emphasized that developing storage is essential for zero-carbon urban transitions in China and Europe, with the industry shifting from scale competition to market deepening and technological empowerment. CALB is undergoing a strategic transformation, upgrading from a single equipment provider to a zero-carbon solution provider, covering three major sectors: storage equipment supply, power station investment & O&M, and zero-carbon business development & operation. Leveraging deep AI-energy integration, the company proposes a "Zero-Carbon Smart City" vision, centered on a zero-carbon platform linking power trading, carbon asset management, and microgrid dispatch, aiming to convert the levelized cost of storage advantage directly into competitive Token pricing for AI data centers. On core products, its long-cycle cells achieve "zero degradation in three years, 15,000+ cycles," and storage system products have been upgraded to 6.9 MWh. Regarding European footprint, the Portugal industrial base involves an investment of approximately €2 billion (~CNY ¥15.2 billion), with Phase I annual capacity reaching 15 GWh. Multiple landmark projects have been deployed in the UK, Hungary, and other markets. Yang Pei expressed CALB's willingness to deepen all-round collaboration with European partners to build an open, win-win China-Europe new energy ecosystem.

Dongping Li

General Manager, Energy Storage Business Unit, ZHEJIANG INPOWER ENERGY Co., Ltd.

Dongping Li, General Manager, Energy Storage Business Unit, ZHEJIANG INPOWER ENERGY Co., Ltd.,analyzed the current status, regional landscape, and market opportunities in Europe. He pointed out that the European storage market is in a phase of high-speed growth, with a projected CAGR exceeding 25% from 2026 to 2030. In 2025, Europe added 27.1 GWh of new storage capacity, bringing cumulative installations to 77.3 GWh. Notably, utility-scale storage accounted for over 50% of new additions for the first time, marking a dual-driven development pattern of centralized and distributed storage. Regionally, the UK, Germany, and Italy form the first tier: the UK boasts the largest and most mature market (>16 GWh); Germany is Europe's largest household storage market (penetration >86%); Italy sees rapid large-scale storage growth fueled by capacity and frequency regulation market incentives. Meanwhile, emerging regions like Eastern Europe, Spain, and the Netherlands are releasing sustained demand, showing outstanding growth potential. Inpower ESS offers full-power-range PCS products adaptable to diverse overseas scenarios and has successfully deployed multiple projects abroad.

Deputy General Manager, Professorate Senior Engineer, Energy Storage Technology Institute Co., Ltd. (affiliated with CEEC Times)

Yueling Gu, Deputy General Manager, Professorate Senior Engineer, Energy Storage Technology Institute Co., Ltd. (affiliated with CEEC Times), shared insights on the development background, design philosophy, and China-Europe synergy prospects for storage supporting large-scale wind and solar bases. He noted that these bases are cornerstones of national energy security, with new-type storage being indispensable. Given their massive scale and diverse generation types, storage planning must follow an integrated development approach. Calculations indicate that a 10 GW-class base typically requires 1–2 GW of storage with a duration of 2–4 hours to optimize multiple objectives. Currently, lithium-ion batteries dominate base storage, but future diversification will create complementarity. Furthermore, he highlighted immense potential for China-Europe energy transition cooperation, suggesting joint R&D on frontier storage technologies and deeper industrial chain synergy to drive global energy transformation.

Roundtable Dialogue:

Accelerating the Pace of China-Europe Energy Storage Cooperation

In the roundtable discussion themed "China-Europe Collaborative Innovation and Win-Win Development in Energy Storage," Qu Haoyuan, Chief Analyst of Renewable Energy Research at CICC,engaged in deep dialogue with four experts. The panelists covered Sino-European technological complementarity, computing-power-electricity synergy trends, industrial investment strategies, and standards/certification mutual recognition.

Victor Gout

Deputy Representative for Alternative Energies, French Atomic Energy and Alternative EnergiesCommission (CEA) -China Office

Victor Gout, Deputy Representative for Alternative Energies, French Alternative Energies and Atomic Energy Commission (CEA) -China Office,argued that lithium-ion batteries and hydrogen energy are not adversarial but complementary, each suited to different scenarios and economic models. Li-ion batteries offer fast charging, high efficiency, and millisecond-level response, ideal for short-term frequency regulation and 2–4 hour power shifting. Thanks to China's large-scale industrialization, Li-ion costs have plummeted, with durations potentially extending to 8 hours or more. Hydrogen, conversely, suits regions unsuitable for pumped hydro and long-duration storage scenarios, while also serving hard-to-abate sectors like industrial decarbonization and fuel replacement, though hindered by lower conversion efficiency and insufficient infrastructure. He stressed that basic research is the most suitable entry point for Sino-French collaboration,with vast potential in solid oxide fuel cells, battery chemistry materials, grid modeling/testing, and standards systems. Both technology paths require continuous breakthroughs to support grids with high renewable penetration.

Zilong Yang

Director of Digital Energy Technologies, Innovation Center, Asia Pacific & Greater China Region, Siemens Energy

Zilong Yang , Director of Digital Energy Technologies, Innovation Center, Asia Pacific & Greater China Region, Siemens Energy, focused on computing-power-electricity synergy. He noted that national data center power consumption reached 170 billion kWh in 2025 and is projected to quadruple by 2030, coinciding with soaring renewable capacity. Storage becomes the critical link balancing fluctuations on both sides. Regarding implementation pathways, he outlined three green power consumption models: green power trading, direct green power connections, and green certificate trading. He emphasized that the internal shift in data centers from AC to 800V DC power supply itself creates new demands for storage.On "computing driving electricity," he highlighted how AI can deeply empower storage system planning/simulation, operational dispatch, and power trading decisions, enabling optimal scheduling amid real-time electricity prices and load fluctuations. Consequently, storage becomes a vital pillar for the safe and stable operation of new power systems.

Pei Yang

VP of Sales ESS, CALB Group Co., Ltd.,

Pei Yang , VP of Sales ESS, CALB Group Co., Ltd.,elaborated on practical pathways and win-win scenarios based on CALB's overseas footprint. Currently, the company's 100 GWh industrial base in Portugal is under construction, and its battery pack facility in Thailand is operational.To navigate the EU Carbon Border Adjustment Mechanism (CBAM) and varying national standards, CALB is making synchronized efforts in industry, standards, and technology: On standards, it proactively engages in aligning with European regulations from early project planning stages to meet diverse certification requirements for grid characteristics and functional specifications. On technology, it operates R&D centers in Europe to enhance localized technical synergy. Pei Yang asserted that global deployment is an inevitable trend, and vast cooperation space exists between China and Europe across industrial investment, standards mutual recognition, and joint R&D.Enterprises should proactively integrate into local systems to foster deep industrial chain integration through co-development.

Among Chen

General Manager – Battery & Container ESS & Charge Station, DEKRA China

Among Chen ,General Manager -Battery & Container ESS & Charge Station, DEKRA China, first systematically outlined differences between Chinese and European storage standards/certification systems regarding regulatory frameworks, standard granularity, and management mechanisms.

Addressing Chinese enterprises going global, he proposed four adaptation pathways: Proactively aligning product designs with EU standards during the design phase; engaging qualified testing laboratories for oversight; preparing bilingual technical documentation; and establishing R&D capabilities with China-Europe linkages. Regarding AIDC (AI Data Center) + Storage, Chen noted that the explosive growth of data centers has spawned new integrated storage demands encompassing "backup power + peak shaving + grid-forming capabilities." China holds distinct manufacturing and technological advantages in high-rate LFP batteries, liquid cooling integration, and grid-forming PCS. Europe excels in data center O&M management, energy efficiency optimization, AI-driven peak load forecasting, and grid-side interconnection. The two sides are highly complementary, enabling a commercial model of "Chinese smart-manufactured products + European management/O&M systems."

Energy Storage

The Most Solid "Technological Foundation" for China-Europe Green Cooperation

As pivotal participants and drivers of the global energy transition, China and Europe exhibit strong complementarity and vast cooperation potential in energy storage. Europe has accumulated advanced experience in power market mechanisms, standards systems, and system O&M management. China possesses a complete industrial system, economies of scale in manufacturing, and rich, diverse application scenarios.

Amid accelerating global energy transformation and technological iteration, deepening China-Europe technical exchanges and industrial synergy in energy storage is both an intrinsic need to advance respective energy transitions and a crucial measure to jointly address global energy security challenges and promote sustainable energy development.

Outcomes from this sub-forum demonstrate that dialogue between China and Europe on storage policy, technology, standards, and markets has entered deep waters. The two sides are transitioning from simple trade relations to a new stage of comprehensive cooperation featuring industrial chain synergy, standards system co-construction, and joint basic research.

It is anticipated that this forum serves as a new starting point for China-Europe energy storage collaboration, continuously injecting robust momentum into the global green, low-carbon energy transition.

Sign up for our free monthly newsletter to stay informed about the Chinese energy storage market.