PCS Vendors Begin to Diversify Their Energy Storage Activities

In response to the rapid development of energy storage, many PCS vendors have begun expanding their business models to become more deeply involved in energy storage services. According to the CNESA Global Energy Storage Vendor Database, China’s current PCS manufacturers can be divided into three categories. The first group includes companies focused predominantly on solar inverters, such as Sungrow. The second is companies predominantly focused on UPS, such as Kelong. The final group is those who focus on energy recovery products, such as Soaring. Data from CNESA’s Global Energy Storage Database reveals that in recent years Sungrow and other companies have become increasingly involved in energy storage projects by taking on the role of energy storage solutions providers. Examples include:

- In June 2017, Sungrow provided solutions for a complete solar-plus-storage system in the Maldives. The system included a PV inverter, energy storage inverter, BMS, and Li-ion battery.

- In March 2018, Kelong provided the Baitu substation second-life battery demonstration project with an SPH series energy storage converter and EMS smart energy management system.

- In 2013, Soaring won a successful tender to provide a PCS for China Southern Grid’s “Modular Distributed Energy Storage System Critical Technology Research Project.” Soaring will supply the project with a bidirectional energy storage converter, project plan design, and engineering services.

Current trends reveal that these and other vendors will continue to expand their activities beyond the sole supply of PCSs to diversified roles in multiple aspects of the energy storage business.

Sungrow was the earliest company in China to begin research, development, and production of inverter products. According to the company’s 2017 annual report, by the end of the 2017 year, a total of 60000 MW of Sungrow’s inverter equipment was deployed worldwide. In 2016, Sungrow and Samsung SDI joined to created Samsung-Sungrow and Sungrow-Samsung companies. Sungrow-Samsung’s range of business includes the production and sale of energy storage inverters, Li-ion batteries, and energy management systems (EMS), among other products. Production began in July of 2016 and has reached an annual production capacity of 2000MWh of electric energy storage equipment. The production of batteries for energy storage is significant in that it allows Sungrow to provide system integration services that not only make use of its own PCS system, but also a battery produced by its joint venture company, ensuring a stable product supply and convenient and accurate assembly during systems integration. In 2017, Sungrow began promoting its “inverter-plus-storage technology” solution. The service not only lowers the cost of the system, but also provides more efficient energy generation through the system’s integrated functionality. Sungrow has also built a reputation in photovoltaics, energy storage, wind power, electric vehicles, and similar areas, which has helped the company’s energy storage solutions achieve better recognition and acceptance among customers.

Kelong has established a name for itself as a PCS provider with over 30 years of industry experience. The company has three main business sectors. Kelong’s core is its “Energy Foundation” business, including high-end UPS, customized power sources, military and industrial power sources, and automated power systems. The second sector is the “Cloud Computing Service,” including data center, data protection, and cloud resource services. The final category is the “Renewable Energy” business, including solar and wind generation, energy storage, microgrids, and electric vehicle charging systems. In energy storage, Kelong’s main focus has been PCSs, supplemented by research in energy routers and microgrid technologies in order to increase competitiveness in the storage market. In residential storage, Kelong provides a 2-5kW residential PV inverter system (SPH). The system’s functions include self-generation, load shifting, backup power, and others. Kelong has expressed the advantages of using technologies from the same production source, expanding and diversifying business activities to transition from equipment supplier to systems solutions and service platform provider, from equipment manufacturer to a manufacturer of advanced technologies and services models.

Soaring represents China’s first company to provide energy recovery and energy storage microgrid system solutions. Soaring’s ES-500K and ES-250k bidirectional converters are specialized for smartgrid construction. Soaring has also researched and designed its own monitoring software for energy storage stations. In providing customers with complete storage solutions, Soaring is able to utilize its own core energy storage converter technology, energy management system, and other equipment, as well as its own software system. Core product technologies and specialized integrated systems and services has helped increase Soaring’s competitive advantage.

PCS providers have begun to make the switch from the supply of a single equipment type to a comprehensive solutions model. This represents not only the individual development of these companies and the increasing diversity of the industry, but also reflects their technological advantages and accumulation of resources for energy storage applications. As consumers place greater needs on energy storage equipment providers for more comprehensive and diverse services, companies that are able to provide a diversified services model will have the biggest competitive advantage in the industry.

Energy Storage Market Developments in the Middle East

Middle Eastern regions have been famous for their large oil and gas reserves for as long as anyone can remember. Though the region’s solar resources are also plentiful, when it comes to renewable energy, developments in the Middle East have been relatively sluggish. In recent years, as PV prices have dropped and the pressure of relying on a single source of energy has grown, these countries have begun looking beyond their oil and natural gas reserves and have established development goals for renewable energy. At the same time, opportunities for energy storage combined with renewable energy have begun to appear. Beginning in 2017, Middle Eastern countries including Jordan and Saudi Arabia have begun deploying energy storage projects.

Saudi Arabia Combines Energy Storage with Renewable Energy to Cast Off Reliance on Oil

In the past, Saudi Arabia was once the world’s top oil producer. Yet with domestic energy demands increasing, so has the pressure on oil supplies, making development of renewable energy a necessity. Saudi Arabia has previously announced plans for a 100% transformation from fossil fuels to clean energy within the next few decades. According to CNESA data tracking, Saudi Arabia’s National Renewable Energy Program managed by the country’s Ministry of Energy, Industry, and Mineral Resources has announced a goal of 3.4GW of renewable energy capacity by 2020, with an additional goal of 9.5GW of renewable energy infrastructure set for 2023. In 2017, SoftBank Vision Fund and the Public Investment Fund of Saudi Arabia signed a memorandum focused on the development of solar-plus-storage. The memo declares a goal of 3GW of solar-plus-storage projects by 2018, which will contribute to the long-term development of renewable energy Saudi Arabia. In March 2018, SoftBank announced plans to construct the world’s largest solar plant in Saudi Arabia. The plant is intended to contribute to the “Vision2030” plan. Such measures will help alleviate Saudi Arabia’s domestic dependence on oil.

Jordan Harnesses Renewable Energy and Energy Storage to Realize Energy Independence

In contrast to the abundant oil and gas resources of Saudi Arabia, Jordan possesses no oil reserves. Energy shortages have led to overreliance on diesel imports. To avoid reliance on traditional fossil fuels, the demand for development of renewable energy applications has become strong. In 2017, Jordan’s Ministry of Energy and Mineral Resources selected 23 out of 41 bidders as candidates for the 2018 signing of a memorandum planning for a 30MW energy storage project. The project’s total investment is set at approximately 4 million USD, with an anticipated completion date of mid-2019. The project is intended to alleviate fluctuations to the grid caused by large scale wind and solar generation, stabilizing transmission and distribution networks.

Jordan’s solar energy provider Philadelphia Solar has also announced plans to launch a battery storage system at a large-scale solar generation plant in the Mid-East region. In early August of 2017, Philadelphia Solar subsidy Al Badiya signed a 20-year PPA with Irbid District Electricity Company. At present, this is the largest energy storage power station project in the Middle East. Construction is expected to be completed and commercial operations to begin in the 4th quarter of 2018. The project will consist of 34,350 polycrystalline panels and a 12MWh Li-ion battery energy storage system.

Summary

At present, governments in the Middle East are actively pushing for the development and utilization of renewables, with many establishing renewable energy development goals. Egypt, the United Arab Emirates, Saudi Arabia, Jordan, and other countries in the region have all deployed energy storage systems. In the future, as renewable energy continues to grow in scale, demand for energy storage as a method of stabilizing wind and solar generation in the grid will increase. As the use of clean, natural energy sources in the Middle East becomes more prevalent, the region will increase its energy independence while at the same time decreasing consumption of traditional fossil fuels.

Tracking the Storage Industry: Why Have So Many Energy Giants Entered the Storage Market?

The China Energy Storage Alliance’s Industry Tracking database has traced an ever increasing number of new companies entering the energy storage market since 2016. At present, the newest entrants into the energy storage business can be divided into two categories: international oil and natural gas companies such as Shell and BP, and large electric power utilities such as E.On.

This article tracks the recent activities of the above-mentioned companies, tracing their involvement in energy storage and reasons for entering the storage market and using such analysis to help understand the current trends in the entire energy storage industry.

1. Oil and Natural Gas Companies Such as Shell Enter the Energy Storage Market

1.1 Oil and natural gas companies begin transformation into comprehensive energy providers, seeking new business methods to combat poor performance caused by declining oil prices

Oil and renewables have often been viewed as incompatible forms of energy, yet in recent years many leading international oil and gas companies have released plans and targets for development in the renewables sector.

Table 1. New Energy Business Development Plans for Major Oil and Gas Companies

Such conditions have led Shell, BP, and other companies to began putting major effort and investment into New Energy business not only to offset poor performance due to low oil prices, but also to find new opportunities for business growth. For example, in September 2017, Shell acquired Texas-based wind, solar, and fuel gas developer MP2 Energy, planning to expand the company’s distributed energy and demand response businesses. MP2’s New Energy business is expected to grow from 200 million USD to 1 billion USD by 2020.

1.2 International oil and gas companies are also engaging in energy storage as a means to build on strengths and more fully develop New Energy business

Table 2: Summary of Major Oil and Gas Company Energy Storage Activities

Total has concentrated efforts on developing solar power and has been a leader in Europe in biofuel technology. The company’s collaboration with Saft provides benefits for nickel and Li-ion battery design and manufacturing businesses.

Shell has focused efforts on developing wind and hydrogen energy, incorporating electric vehicle charging as a part of such business.

BP is looking towards biofuels as its primary direction for New Energy development. Current collaboration with Tesla on wind farm energy storage allows BP to make more informed decisions when evaluating and developing future battery storage projects. BP has at the same time begun developing new low-carbon business activities to expand its involvements in New Energy development.

Finally, ExxonMobil has emphasized investments in biofuels and carbon capture and storage technology. Collaboration with Fuel Cell Energy has focused on research and development of fuel cell technology. Current fuel cell applications have primarily been concentrated on portable power supplies, mobile power supplies, and small-scale custom power supplies.

2. Large Electric Power Utility Providers Such as E.ON Enter the Energy Storage Market

Table 3: Summary of Major Electric Power Utility Energy Storage Activities

The above table shows that from March 2016 to April 2018, Enel and other electric power utility companies engaged in a variety of energy storage business activities, including the construction and operation of new storage projects. There are two main reasons for these activities:

2.1 Energy storage technology has proven itself beneficial to the energy transition and an important component of large-scale renewable generation and grid integration

The Paris Agreement signed at the Paris Climate Change Conference on December 12, 2015 included China, the United States, Russia, and numerous other countries. The agreement specifies actions for combating global climate change by 2020. The primary goal of the Paris Agreement is to keep this century’s global average temperature from rising more than 2 degrees Celsius while at the same time limiting the global temperature increase to within 1.5 degrees Celsius above pre-industrial levels. The most direct method to combat the rise in temperature is to decrease carbon emissions.

In light of this agreement, power utilities such as E.ON must begin turning their primary business models away from carbon-intensive power generation to low-carbon power generation business models. As a result, Engie, E.ON, and other companies have announced low-carbon power generation plans.

The key to the energy transition is scalable renewable energy. Current global renewable energy resources are extremely abundant, particularly solar and wind power. Data suggests that if earth were able to harness 1/6000th of the energy released by the sun’s rays, or 1/500th of the energy created by the earth’s winds, then the entire global economic demand for energy could be met. Yet despite the enormous potential for renewable energy, its lack of stability hinders large-scale development and applications. Solar and wind curtailment are also common problems. However, with energy storage, renewable energy issues such as variations in voltage and frequency can be managed, and wind and solar curtailment can be reduced.

Application example:

E.ON has recently announced that its two 9.9MW Li-ion battery storage projects in Texas have begun operation. The projects, known as the Texas Waves Energy Storage Projects, are located at E.ON’s Pyron and Inadale wind farms near Roscoe in eastern Texas. The projects provide ancillary services for ERCOT, provide rapid response to power demand changes, and increase the stability and efficiency of the grid.

2.2 Energy storage can provide a variety of services to power grids, including increased grid efficiency, optimization of current resources, and effective integration of newly added renewable resources

In traditional grid planning, rising peak energy demands are handled through addition of new infrastructure to meet capacity needs, leading to issues of excessive construction and a decrease in system efficiencies. Maintenance and upgrade of transmission and distribution infrastructure is the largest expenditure for electric utility companies, yet aside from expensive investments, traditional methods for expanding grid capacity provide no alternative solutions. However, the installation of low-cost, intelligent behind-the-meter distributed resources and energy storage can open new doors for harnessing the full potential of current infrastructure.

Application example:

In order to avoid investing in large-scale grid upgrades, New York state required utilities to research solutions for T&D upgrade deferrals, with energy storage among possible solutions. The Marcus Garvey apartment project is a classic case study arising from the incentive policies of New York state’s climate change bill. In Arizona, APS has made plans to utilize AES’s 2MW/8MWh energy storage project to offset the need for 20 miles of line upgrades in remote areas caused by load increases. The project will cut fixed-asset investment cost by half. Unlike the New York project’s focus on innovation, the Arizona project is focused entirely on economic benefit.

Conclusion

As the global energy transition continues, major global energy companies will continue to devote business to energy storage. The advantages and resources of such large companies is certain to provide many new opportunities and a positive development outlook for energy storage.

CNESA Global Energy Storage Market Analysis – 2018 Q1 (Summary)

1. The Global Market

In the first quarter of 2018, the global electrochemical energy storage market experienced a growth of 94MW, a decrease of 37% from Q1 of last year.

In a regional comparison, the United Kingdom showed the greatest increase in new energy storage capacity, at 54.5MW. The United States followed closest behind in new growth. Installations in the United Kingdom and the United States were primarily devoted to ancillary services applications, with such applications making up 99% and 60% of the United Kingdom and the United States’ total installations, respectively.

In distribution of applications, ancillary services displayed the highest operational capacity at 73.8MW, or 79% of the total, an increase of 228% from Q1 of 2017. Behind-the-meter and renewable integration applications were second and third at 14% and 7%, respectively.

In a comparison of technologies, Li-ion batteries held the highest capacity at 93.7MW, or 99.7%. Li-ion batteries were distributed throughout a variety of energy storage applications, with the largest portion concentrated in ancillary services applications, at 79%.

2. The Chinese Market

China’s newly installed electrochemical capacity was relatively small in the first quarter of 2018, therefore the below analysis focuses only on projects that are newly planned/under construction.

In a regional comparison, projects newly planned/under construction were largely distributed in the areas of Xinjiang, Tibet, Jiangsu, and Inner Mongolia. Of these regions, Tibet and Xinjiang possessed the largest installations, both at 100MW and utilized in renewable integration applications.

In applications newly planned/under construction, the largest capacity was concentrated in renewable integration, at 200MW, or 88% of total applications. Behind-the-meter and ancillary services applications were second and third, at 8% and 4%, respectively. Of these applications, renewable integration and ancillary services both relied completely on Li-ion batteries. Behind-the-meter applications relied primarily on lead-acid batteries, at 89% of the total.

In technologies, projects newly planned/under construction were primarily Li-ion battery and lead-acid battery based, with Li-ion batteries comprising the largest capacity at 211MW, or 93% of the total. Li-ion battery usage was distributed amongst renewable integration, ancillary services, and behind-the-meter applications, with the most prevalent usage seen in renewable integration, at 95%.

3. About this Report

The complete version of our Global Energy Storage Market Tracking Report (2017) can be downloaded from the CNESA ES Research website.

The ES Research website was launched January 18, 2018. The site provides accurate, authoritative, and up-to-date market data analysis and information on the energy storage industry. Please visit the website at www.esresearch.com.cn or scan the QR code below to learn more about the research services we offer.

For questions or concerns, please contact the CNESA research department:

Telephone: +86 010-65667068

Email: na.ning@cnesa.org

ESIE 2018 – Who Should Foot the Bill for Energy Storage? An Immature Market Mechanism Remains the Largest Obstacle to Energy Storage Proliferation

Author: Deng Huiping China Electric Power News

It has been over a year since the release of the “Guiding Opinions on Promoting Energy Storage Technology and Industry Development,” and within the New Energy industry, the lack of a mature market mechanism remains the major factor inhibiting the spread of energy storage. The market mechanism described in the “Guiding Opinions” – “payment according to effectiveness, with the beneficiary covering the cost” is one that still requires ongoing support and development.

Who Should Benefit? A Fierce Debate

Energy storage is a critical component to an “intelligent” grid and an energy system dominated by renewables. Energy storage plays an important role in the stabilization of renewable energy, consumption of clean energy sources, participation in peak shaving and frequency regulation, ensuring grid safety and stability, lowering grid infrastructure costs, and more. However, due to high equipment costs and debates over who should reap the benefits of energy storage, the development of what should be a very popular component to the energy system has instead been slow moving.

Some countries with developed power markets have seen the competitive use of frequency regulation, leading to its widespread applications. Amongst China’s thermal power plants, energy storage as a part of peak shaving, frequency regulation, and other ancillary services has already begun to see some acceptance from the market. The addition of energy storage equipment to thermal power plants allows for more accurate, speedy, and effective peak shaving and frequency regulation response, while also lowering the cost of the services and generating a profit for the plant. The spread of energy storage to thermal power plants has therefore been a relatively smooth process, though applications have still been few and of small scales. The reason for this slow progress has been the lack of enthusiasm amongst electricity generators, the grid, and others involved in the power system to invest in New Energy storage equipment due to the continuing debate over who should receive the profits from energy storage.

During a presentation at ESIE 2018, China Energy Storage Alliance Chief Supervisor Zhang Jing noted that New Energy power generators feel that because energy storage can balance electricity generation, lower off-peak generation, ensure grid safety and stability, and lower investment costs for infrastructure, therefore, the power grid should pay the cost for energy storage. Yet grid operators feel that the price for New Energy electricity is already high enough, and since energy storage helps to promote the production of New Energy electricity, the New Energy electricity generators should naturally foot the bill for energy storage.

Jiang Liping, Vice Dean of the State Grid Energy Research Institute, stated that State Grid has never viewed power generation from New Energy sources as an independent source of power, citing lower stability and higher costs than power generated from thermal plants. Therefore, the grid does not wish to foot the bill to install energy storage technology in New Energy generation stations, as the number one duty and responsibility should be providing stable electricity.

Although at present the price of New Energy is higher than that of thermal power, due to the large investment cost and long rate of return, many New Energy power generation plants still have a low profit margin. In such a case, adding energy storage equipment would not be economical, and therefore there is little enthusiasm to do so.

The Market Mechanism Still Requires Strengthening

On the one hand, most people recognize the potential of energy storage in New Energy generation, ancillary services, microgrids, behind-the-meter applications, the energy internet, and other applications. On the other hand, enthusiasm remains low and popularization remains difficult. Zhang Jing stated that conquering this obstacle will require further work in strengthening energy storage market and pricing models, thereby making the value of energy storage more obvious to everyone.

Many experts share this same view. Currently, much of the value and benefit of energy storage is still unclear. Energy storage’s value must be clarified for all stages, including generation, transmission, distribution, and usage. An open electricity market and flexible market pricing mechanism will help promote energy storage’s commercial value. Xie Kai, Vice Director of the Beijing Power Exchange Center, stated that strengthening the energy storage market mechanism is of utmost importance. As he explained, in countries that have already established a complete energy storage market mechanism, the development of energy storage has been rapid. One example from abroad is a frequency regulation compensation mechanism that shrinks the investment return for energy storage equipment from 5-8 years to 2-3 years.

In this regard, the effects of the Guiding Opinions will gradually make themselves known. The Guiding Opinions clarifies several issues regarding energy storage, including the path for policies that encourage the development of energy storage, the identity of energy storage, the investment and management system of energy storage, and the responsibilities of energy storage demonstrations. This gives a visible outlook for investors, helping to stimulate the market.

A representative from the National Energy Administration described plans to continue to advocate for energy storage development in four ways. First, through improving relevant policies and mechanisms. Second, promoting technological advancements and lowering costs. Third, through organization of energy storage demonstrations encouraging companies to innovate in technologies, business models, and large-scale applications. Fourth and finally, through the improvement of relevant standards.

ESIE 2018 Finishes its 7th Year - Highlights from the Event

ESIE 2018 Opening Ceremony

The 7th Annual Energy Storage International Conference and Expo (ESIE 2018) opening ceremony on April 3 began with a speech by National Energy Administration Vice Director Liu Yafang emphasizing energy storage industry and technology development as key to the energy revolution. Her speech suggested four ways to advance the industry: promotion of government policies and mechanisms, increased technological innovation, launching of new demonstrations, and strengthening of industry management and services. Vice Chairman of the China Energy Research Society Shi Yubo presented four main points of focus for the development of the energy storage industry, including the building of a policy mechanism for energy storage, increasing the participation of energy storage in the electricity market, increasing innovations in energy storage technology, and increases in project demonstrations and dissemination of information on energy storage. Tsinghua University Professor and former State Council Member Wu Zongxin, Chinese Academy of Sciences International Cooperation Department Director Cao Jinghua, and CNESA Chairman and China Energy Research Society Committee Chair Chen Haisheng also delivered welcome addresses. Chinese Academy of Sciences Scholar and China Electric Power Research Institute Honorary President Zhou Xiaoxin delivered a keynote speech entitled “Development Prospects for China’s New Generation of Energy Systems.” Chinese Academy of Engineering Scholar and Chemical Defense Research Institute Researcher Yang Yusheng followed with a keynote entitled, “System Safety Issues in Large-Scale Electrochemical Energy Storage Systems.” CCTV-Finance reporter Ping Fan served as host for the first half of the opening ceremony.

National Energy Administration Vice Director Liu Yafang Delivers the Opening Speech

Tsinghua University Professor and Former State Council Member Wu Zongxin Delivers a Speech

Chinese Academy of Sciences International Cooperation Department Director Cao Jinghua Delivers a Speech

CNESA Chairman and China Energy Research Society Committee Chair Chen Haisheng Delivers a Speech

Vice Chairman of the China Energy Research Society Shi Yubo

Chinese Academy of Engineering Scholar Yang Yusheng

Chinese Academy of Sciences Scholar and China Electric Power Research Institute Honorary President Zhou Xiaoxin Delivers His Keynote Speech

Chinese Academy of Engineering Scholar and Chemical Defense Research Institute Researcher Yang Yusheng Delivers His Keynote speech

“Build a Market Mechanism for Energy Storage, Create a Blueprint for Industry Development” served as the theme for this year's conference. Over 120 domestic and international speakers and over 60 exhibitors were in attendance. The conference focused on three main events—the exhibition hall, innovation competition, and conference forums. The variety of events and programs provided a platform for communication between policymakers, planners, grid managers, power companies, energy service providers, and numerous other businesses and organizations involved in energy storage.

The opening ceremony was followed by the International Innovation Competition Awards Ceremony, industry expert dialogues, and the release of CNESA’s 2018 industry white paper. The April 3 events drew over 3000 industry guests from China, the United States, Germany, Australia, Korea, Japan, and more.

2018 International Energy Storage Innovation Competition Awards Ceremony

Following the opening ceremony speeches came the exciting announcement of the winners of the second International Energy Storage Innovation Competition. This year’s five categories included the “2018 Top 10 Technology Innovations Prize,” “The 2018 Top 10 Applications Innovation Prize,” the “2018 Energy Storage Distinguished Individuals Award,” the “Jury Grand Prize,” and the “Team Participants Award.” The awards honored those companies and individuals who made outstanding contributions to energy storage in 2017. The Jury Grand Prize was awarded to BYD Motor’s 31.5MW/12.06MWh Beech Ridge frequency regulation project in West Virginia.

Winners of the 2018 Top 10 Energy Storage Technology Innovations Award

Winners of the 2018 Top 10 Energy Storage Applications Innovations Award

Winner of the Jury Grand Prize: BYD Motors’ 31.5MW/12.06MWh Beech Ridge Frequency Regulation Project in West Virginia.

Five industry leaders were awarded the 2018 Energy Storage Distinguished Individual Award, including Birmingham University Professor and Founder and Editor-in-Chief of Energy Storage Science and Technology magazine Ding Yulong, Chinese Academy of Sciences Institute of Thermophysics Researcher Huang Xuejie, BYD Electric Power Institute Chief Engineer Zhang Zifeng, Beijing Puneng Energy President Huang Mianyan, and Beijing Ray Power CEO Mou Liufeng.

Winners of the 2018 Energy Storage Distinguished Individual Award

Energy Storage Industry White Paper 2018 Officially Released

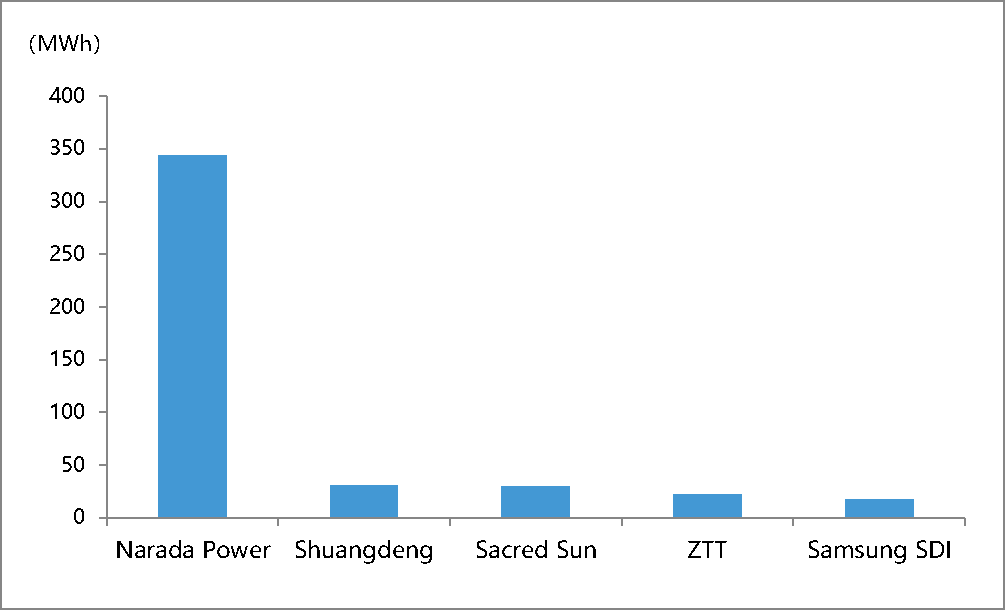

The opening ceremony featured the release of CNESA’s Energy Storage Industry White Paper 2018, announced by CNESA chief supervisor Zhang Jing. Included in the white paper is a list of the companies with the highest operational energy storage capacity for 2017. Of these companies, Narada Power topped all lists. According to white paper statistics, the top five technology providers for newly installed electrochemical energy storage capacity included (from highest to lowest capacity) Narada Power, Shuangdeng, Sacred Sun, ZTT, and Samsung SDI. In terms of MW capacity, the top five energy storage system integrators (from highest to lowest capacity) included Narada Power, Sungrow-Samsung, CLOU, Shuangdeng, and ZTT. In terms of MWh generation, the top five energy storage system integrators (from highest to lowest) included Narada Power, Shuangdeng, ZTT, Sungrow-Samsung and CLOU.

China Energy Storage Alliance Chief Supervisor Zhang Jing Announces the Release of the 2018 Energy Storage Industry White Paper

Industry Leader Dialogues: New Coordinates for the Development of the Energy Storage Industry

Tsinghua University Professor of Electrical Engineering and Deputy Committee Chair of the China Energy Research Society Expert’s Committee Xia Qing hosted the “New Coordinates for the Development of China’s Energy Storage Industry” dialogue. Distinguished industry leaders such as State Grid Electric Vehicle Service Co. Vice General Manager Que Shifeng, National Energy Administration Division of Technology Director Qi Zhixin, Beijing Power Exchange Vice Director Xie Kai, State Grid Energy Research Institute Vice Dean Jiang Liping, Sungrow Power General Manager Wu Jiamao, Chinese Academy of Sciences Institute of Physics Researcher Huang Xuejie, Narada Power President Chen Bo, and Beijing Soaring Electric Technology Co. Chairman Wang Shicheng attended the panel discussion, sharing thoughts on technological development, market needs, and policy mechanisms for the energy storage industry. The discussion provided those in attendance with an insider look at the state of energy storage development, how market mechanisms can be created, and how local markets are expected to develop in the future.

Industry Leaders Take Part in the Expert Dialogue

ESIE 2018 Expo: An Exhibition of the Top Names in Energy Storage

ESIE’s three-day energy storage expo officially opened on April 2. This year’s exhibitors included displays from upstream energy storage equipment manufacturers, systems integrators from a variety of applications, power grid representatives, testing organizations, and energy storage research institutions. Leading energy storage enterprises domestic and international set up booths, including domestic enterprises such as State Grid Electric Vehicle Co., Sungrow, Shuangdeng Group, Dynapower, Narada, Tianjin Lishen, Soaring, CLOU, BYD, ZTT, Hyperstrong, Today Energy, and more. International enterprises and organizations such as NEC, ABB, TÜV SÜD, NGK, the India Energy Storage Alliance, and Primus Power also brought their technologies, products, and services to the expo hall.

Industry Experts and Leaders Tour the Expo Hall

Thank you to all the exhibitors, sponsors, and attendees who helped make ESIE 2018 a success! We will see you again next year at ESIE 2019!

ESIE2018: CNESA Releases the 2017 Chinese Energy Storage Company Capacity Rankings, Narada Power Tops the List

On April 3, the China Energy Storage Alliance kicked off the 2018 Energy Storage International Conference and Expo at the National Convention Center in Beijing. The opening ceremony featured a presentation by China Energy Storage Alliance Chief Supervisor Zhang Jing announcing the release of CNESA’s Energy Storage Industry White Paper 2018. This year's white paper features a list of the top five technology providers and systems integrators both domestic and international.

China Energy Storage Alliance Chief Supervisor Zhang Jing Announces the Release of the Energy Storage Industry White Paper 2018

The lists rely on data provided primarily by the CNESA Global Energy Storage Project Database, as well as publicly available project information and information provided voluntarily by companies. The lists are focused on the newly installed capacity of energy storage technology providers and systems integrators in the year 2017.

The “technology providers” category, as defined by CNESA, includes companies that provide energy storage technologies, battery modules, and battery systems. The “systems integrators” category includes companies that are involved in the energy storage systems integration business, providing customers with a complete energy storage system. Such products include BMS, PCS, EMS and all other components that are needed for a complete set of equipment.

China’s Energy Storage Market List

In 2017, among China’s newly added electrochemical energy storage projects, the top five technology providers with the largest new capacity included Narada Power, Shuangdeng, Sacred Sun, ZTT, and Samsung SDI.

China’s Top Technology Providers for 2017 (MWh)

In 2017, among China’s newly added electrochemical energy storage projects, the top five systems integrators in terms of MW capacity included (in order from greatest to least) Narada Power, Sungrow-Samsung, CLOU, Shuangdeng, and ZTT. In terms of MWh capacity, the top five systems integrators included (in order from greatest to least) Narada Power, Shuangdeng, ZTT, Sungrow-Samsung, and CLOU.

China’s Top Systems Providers for 2017 (MW)

China’s Top Systems Providers for 2017 (MWh)

From the rankings, it is clear to see that the 2017 Chinese energy storage market’s most active areas continued to be Li-ion battery and lead-acid battery manufacturers and systems integrators. Also of note is that the companies making the lists are predominantly those that serve the role of both technology provider and systems integrator. Of these, Narada Power stands out as the clear leader in installed capacity, sitting at the top of all three lists. ZTT occupied the top spot in energy generation (MWh) as both technology provider and systems integrator, while Sungrow-Samsung occupied the top of the list of Li-ion battery systems integratiors in terms of power (MW) capacity.

Customer-sited Grid Integrated Energy Storage Systems Break the Ice, Bringing a Boost to China's Energy Storage Industry

Background

In recent years, Jiangsu Grid has experienced an increasing expansion in the gap between peak and off-peak loads, creating an urgent need for new methods to balance generation and demand. There are two reasons for the problem. First, through the support of national and local subsidy policies, Jiangsu province’s distributed PV has seen rapid development. The intermittency and instability inherent with distributed PV power stations has caused Jiangsu Grid significant difficulty balancing demand and generation. Second, due to the increased need for electricity caused by rapid economic development, power load cycles inevitably face growing in the gaps between peak and off-peak grid loads. Although TOU policies have played an important role in load shifting, they cannot restrain the ever-widening peak and off-peak load gap.

With customer-sited energy storage beginning to take shape and its potential increasing, it has become a reliable source of generation and demand balance for the grid. According to State Grid of Jiangsu statistics, as of October 2016, Jiangsu province possessed operational and potential energy storage projects at a total capacity of 886,000 MWh. Of this total, 16,580 MWh of storage had already been constructed, 154,250 MWh was under construction, and 715,170 MWh of storage was in negotiation. As energy storage battery costs continue to drop, the potential for future energy storage markets continues to grow. How customer-sited storage will be used, how control of systems will be coordinated, and how the technology can be used in balancing generation and demand are all unavoidable questions that grid companies must face.

Energy storage systems possess advantages such as a quick response speed, precise load control, a short construction period, non-consumption of fossil fuels, no emissions, and other features. At the same time, they encourage the use of renewable resources and regional T&D deferral for grid construction. Therefore, the use of customer-sited grid integrated energy storage controlled by a unified dispatch center is a worthy method of balancing the grid.

Key Points

Recently, State Grid Jiangsu released the Customer-sited Energy Storage System Grid Integration Management Regulations (hereafter known as Regulations). The Regulations are focused directly on the development of Jiangsu province’s customer-sited energy storage, with support for such systems as the central goal. The Regulations focus on ensuring safety, increasing efficiency, and standardizing the division of responsibility for workers as well as the work procedure. Below are some of the notable characteristics of the Regulations:

1. Categorical management based on capacity

The Regulations divides customer-side energy storage in two categories. The first category includes customer-side storage systems rated at 6MW or less connecting to the grid at 10 KV or less. The second category includes customer-side storage systems rated above 6MW connecting at 10KV, or any system connecting at 35 KV. Equipment of both categories is required to undergo inspection by the power company before installation, and metering equipment and information collection systems must also be installed. Finally, a dispatch agreement must be created with the grid company. The difference between the two categories is that for the first category, in which capacity is rather small, a “stand back and observe” model is used, in which city/district companies will facilitate supervision of the system. Items to be monitored include the voltage, current, active power, inactive power, charge capacity, and discharge capacity of the customer-sited energy storage system. For the second category, in which capacity is rather large, a different model of combined monitoring and control is used. City/county dispatch centers are responsible for operation and management of the energy storage equipment.

2. Safety standards as the first step for grid integration

Customer-side energy storage systems are largely battery systems, with DC input and output, and transforming to DC/AC through the use of a converter. Such a system is certain to cause harmonics that will affect power quality, while misuse of battery systems carries the risk of fires or explosions. To ensure the safety of the grid, the Regulations stipulate: “Connections to the grid must meet national power quality standards, and engineering design and construction must satisfy such standards as the Technology Regulation for Energy Storage Systems Connecting to the Power Grid (Q/GDW564-2010) and Battery Energy Storage Power Station Design Standards (Q/GDW11265-2014). In other words, customer-side energy storage has a fair chance to participate in the grid as long as systems meet the standards already in place for grid technology

3. Processes, work distribution, and time limits are clearly specified

The Regulations divide grid integration of customer-sited energy storage into 5 processes: application and site surveying, engineering and construction, grid integration inspection and debugging, meter installation, and contract signing. Tasks in each stage are designated to specific units or persons. City/district company business applications managers are responsible for the acceptance of new applications, and a development and planning department are responsible for approval of grid integration plans. Accounts managers are tasked with inspection of engineering designs for energy storage systems, with customers choosing appropriate construction companies. Accounts managers and dispatch centers of prefectural and municipal companies are responsible for acceptance and debugging of projects of varying capacity, and can provide one-time suggestions on the acceptance and verification of new grid integration proposals. City/district companies also designate a specific department to the installation of metering and data collection systems. The Regulations defines a detailed timeframe for the completion of each stage to combat delays or procrastination.

Conclusion

State Grid Jiangsu’s Customer-sited Energy Storage System Grid Integration Management Regulations stands as China’s first regulation for customer-sited grid integration. The policy is certain to facilitate new large-scale grid integration of customer-sited energy storage equipment, alleviating some of the demand pressure on the grid, and guaranteeing that energy storage customers will receive reasonable benefits—a win-win situation for both sides.

CNESA Storage Market Analysis – 2017 Q4

1. The Global Market

Electrochemical Storage Projects Continue a Steady Growth

According to partial statistics provided by the China Energy Storage Alliance (CNESA) Global Energy Storage Database, at the 2017 year’s end, global energy storage projects reached a total operational scale of 175.4GW. Pumped hydro storage occupied the largest portion of the capacity at 96%, a decrease of 1 percentage point from the previous year. Electrochemical capacity occupied a total of 2926.6MW, or 1.7% of the total, an increase of 0.5 percentage points from the previous year. 2017 saw the installation of a total of 914.1MW of new electrochemical capacity, an increase of over 20% compared to 2016.

In comparing energy storage distribution by region, the United States saw the greatest increase in new capacity at 210.3MW. Australia saw the greatest increase in comparison to 2016, at 1277%

In comparing energy storage distribution by application, renewable integration saw the largest increase in new capacity in comparison to 2016, at 300.8MW, a 119% increase.

In comparing the distribution by technology, Li-ion batteries had the greatest installed capacity at 845.9MW, or over 90% of the total. Growth in lead-acid batteries was highest in comparison to 2016 Q4, at nearly 100%, over three times that of Li-ion batteries.

2. The Chinese Market

Electrochemical Storage Capacity Continues to Grow Steadily

According to partial statistics provided by the CNESA Global Energy Storage Database, as of the 2017 year’s end, China achieved a total of 28.9GW of operational energy storage capacity. Pumped hydro storage occupied the greatest percentage of storage capacity, at nearly 99%. Electrochemical storage capacity occupied 389.8MW, or 1.3% of the total, an increase of 0.2 percentage points since the previous year. In 2017, China put into operation a total of 121MW of new electrochemical capacity, an over 15% increase compared to 2016.

In comparing China’s energy storage distribution by region, the majority of operational capacity was concentrated in east, north, south, and northwest China. Jiangsu province possessed the largest scale of operational capacity at nearly 50MW.

In comparing distribution by application, renewable integration, ancillary services, and behind-the-meter energy storage occupied the entirety of all new capacity. Of these, behind-the-meter applications were of the largest scale, at over 70MW. Ancillary services saw the largest increase from the previous year, at nearly 1000%.

In comparing the distribution by technology, Li-ion and lead-acid batteries were at a relatively equal scale of 51% and 49%, respectively. At the same time, lead-acid batteries saw the greatest increase since the previous year, at over 81%.

3. About this Report

The complete version of the Global Energy Storage Market Tracking Report (2017) can be downloaded from the CNESA ES Research website.

The ES Research site was launched January 18, 2018. The site provides accurate, authoritative, and up-to-date market data analysis and information on the energy storage industry. Please visit the website at www.esresearch.com.cn or scan the QR code below to learn more about the research services we offer.

For questions or concerns, please contact the CNESA research department:

Telephone: +86 010-65667068

Email: na.ning@cnesa.org

The Ten Events that Defined China’s Energy Storage Industry in 2017

In 2017, China’s energy storage industry began to heat up. October marked the release of the first national-level policy on the energy storage industry, and the energy storage market took big steps towards commercialization. Based on long-term industry tracking, CNESA’s research department has gathered together the top ten energy storage news events to occur in China in 2017. Let’s hope for an even better year for energy storage in 2018!

1. The Release of the “Guiding Opinions on Promoting Energy Storage Technology and Industry Development” Clarifies the Key Goals for the Next Ten Years of Energy Storage Development

On October 11, 2017, the Chinese government released the “Guiding Opinions on Promoting Energy Storage Technology and Industry Development.” The policy, which is the first of its kind for China’s energy storage industry, focuses on current issues related to China’s energy storage technology and development, such as lacks in policy support, research demonstrations, standardization, and other issues. The policy proposes an energy storage development goal for the next 10 years and five major tasks for China’s energy storage development. The policy is a milestone for China’s energy storage industry, certifying energy storage’s place in the energy revolution and its use as a key strategy for a clean, low-carbon modern energy system.

2. The “Workplan for the Improvement of a Subsidy (Market) Mechanism for Ancillary Services” Encourages Energy Storage Equipment to Provide Ancillary Services

The National Energy Administration released the “Workplan for the Improvement of a Subsidy (Market) Mechanism for Ancillary Services” in response to new challenges in operations management for electricity systems. The workplan seeks to improve and develop the subsidy (market) mechanism for ancillary services, and formulates a detailed, multi-stage development goal and key tasks. The policy continues the “Grid-Connected Power Plant Ancillary Services Management Interim Measures” from 2006, serving as another important outline for the promotion of ancillary services nationwide. The workplan puts forth an increase in ancillary services according to need, encouraging energy storage equipment and demand-side resources to provide ancillary services, and permits third parties to participate as providers in ancillary services.

3. Shanxi Province Begins Initial Trials of Energy Storage for Peak Shaving and Frequency Regulation Ancillary Services

The Shanxi Energy Regulatory Office released the “Notice on Encouraging Energy Storage in Peak-Shifting and Frequency Regulation Ancillary Services in Shanxi Province.” The notice is the country’s first administrative regulation focused on energy storage for ancillary services. In order to ensure that energy storage will be able to participate in the ancillary services market smoothly, the notice includes a workplan for program management, power pricing policies, grid dispatch strategies, and other areas. Shanxi province’s trial period for energy storage in ancillary services will consist of peak shaving and frequency regulation services utilizing both integrated and independent energy storage facilities. Initial peak shaving trial units are set for a total capacity not to exceed 300,000KW, while initial frequency regulation trial units are set for a total capacity not to exceed 120,000KW.

4. Grid-integrated Energy Storage Sees Support through Jiangsu Province’s Release of the “Customer-side Energy Storage Grid Integration Management Regulations”

State Grid Jiangsu Electric Power Co. released the “Customer-side Energy Storage Grid Integration Management Regulations.” The policy provides regulations for grid integration of customer-side energy storage systems connecting to the grid at 3,500 volts or less and a storage power rating of 20MW or less. Customer-side storage systems of 10 (6,20) thousand volts or more require local company control centers to conduct the necessary grid integration tests and configurations. 380 (220) volt customer-side energy storage systems require city/county company customer managers to be responsible for organizing the appropriate department to conduct the necessary grid integration tests and configurations.

5. Energy Storage Enterprises Increase Deployment of Industrial and Commercial Storage Projects, with Jiangsu, Beijing, and Guangdong Becoming Hot Spots

According to statistics from CNESA’s project tracking database, Jiangsu, Beijing, Guangdong were 2017’s hot spots for planning, constructing, and implementation of new energy storage projects. These three areas are notable for their developed economies, numerous industrial and commercial parks, and heavy power use. Industrial and commercial users in these areas also engage in large degree of energy arbitration, and can make use of load shifting for electricity price management. Narada, Sunwoda, Clou, and ZTT represent the key companies that have continued to increase deployment in the above three regions, both through increased activation of projects and the continuous release of contracts and construction plans for projects at 100 MWh and above.

6. Local Ancillary Service Markets Continue to Open, Encouraging Energy Storage to Be an Independent Market Player

According to statistics from CNESA’s policy tracking database, following the lead of the special market reform trials for ancillary services in the northeast region beginning at the end of 2016, Shandong, Fujian, Xinjiang, and Shanxi each released their own marketization trials and operations regulations for ancillary services in 2017. Each area has created its own peak shaving and frequency regulation market trading mechanism based on their unique power generation and load needs. Each area has also defined an equal role for market players, including power generation companies, power sellers, and power users. Energy storage can provide ancillary services to power systems as an independent market player, or integrate with power generators at the generation side to share market benefits.

7. Problems in the Use of Renewable Energy Peak Shaving Become More Apparent, Energy Storage’s Flexibility for Generation-side Applications Continues to Attract Attention

Due to the limited peak shaving abilities of power systems, lags in the planning and construction of transmission channels, and other reasons, problems in China’s use of renewable resources has become an increasingly urgent issue. As a result, the flexibility of energy storage applications for generation-side applications became an area of increased interest in 2017. Construction began on large-scale integrated “resource bases” combining wind, solar, water, thermal, and energy storage. Power generators and energy storage enterprises also teamed together to explore solar+storage models, wind+storage models, and dispatch solutions, with Huaneng’s solar+storage project in Qinghai, Beikong Renewable Energy’s Energy Storage plant in Yangyi, Tibet, and the Yellow River wind+storage farm project in Qinghai serving as examples of renewable energy generation-side storage projects either in operation or under construction.

8. EV Battery Recycling Programs Take Off, Second-Life Battery Markets Begin to Form

With China’s EV sales continuing to climb, a large number of batteries will soon face retirement. The State Council’s release of the “Manufacturer Extended Responsibility Plan” extends responsibility to EV manufacturers and establishes a system for the use of recycled batteries. According to CNESA statistics on second-life battery markets, in 2017, new energy vehicle enterprises, energy storage system aggregators, EV manufacturers, PACK and BMS enterprises, battery recyclers, and other industry chain members have all increased efforts to create a second-life energy storage market. The establishment of second-life trial programs at the megawatt level in industrial and commercial parks, China Tower Co.’s release of an EV recycling bidding program, and other trends have created popularity for second-life energy storage markets.

9. Four Energy Storage Technologies Receive National Support and Become Key Research Focuses for 2018

The Ministry of Science and Technology’s release of the “Smart Grid Technology and Equipment” special guidelines in 2018 reveals five technology focuses. These include the use of large scale renewable integration, flexible large-scale energy internet, diversified customer supply and demand interaction, multi-resource distributed energy supply and microgrids, and smart grid foundations. In total, 23 key research tasks have been created. In 2018, the key energy storage technology research areas include technologies for scaling applications of second-life EV batteries, foundational research on high safety long-life solid state batteries, research of megawatt scale flywheel energy storage key technologies, and research of liquid metal battery storage technologies.

10. The First Batch of New Energy Microgrids and Energy Internet Demonstrations are Released, Energy Storage Plays a Critical Support Role

In 2017, China’s National Development and Reform Commission and the National Energy Administration each released the “New Energy Microgrid Demonstration Programs List” and the “‘Energy Internet+Smart Energy’ Demonstration Projects List,” respectively. 28 new energy microgrid demonstration projects and 56 energy internet demonstration projects were included on the lists. Out of the 28 projects, 25 are focused on electric energy storage or heat energy storage. Of the energy internet projects, the majority are energy storage facilities. Energy storage has already become a critical technology for the support of new energy microgrids, the energy internet, and other new energy applications.

The CNESA research department conducts continuous tracking of energy storage industry development both in China and around the world. A comprehensive summary and analysis of the 2017 energy storage industry’s projects, manufacturers, and policies will be available in CNESA’s “Energy Storage Industry White Paper 2018,” to be released during the 7th Energy Storage International Conference and Expo scheduled for April 2018.

A Look Back on the Energy Storage Industry in 2017

2017: An Unexpectedly Busy Year for Energy Storage Development Around the World

Amongst the variety of energy storage technologies, electrochemical storage technologies have developed more speedily than any other. Li-ion batteries, NaS batteries, lead-acid batteries, and flow batteries have all entered the fast lane of development. According to statistics from the China Energy Storage Alliance (CNESA), worldwide total capacity for electrochemical energy storage from 2000-2017 was 2.6GW, or 4.1 GWh. These numbers represent a growth of 30% and 52% from 2016, respectively. 2017 saw a total increase of 0.6GW, or 1.4GWh, with over 130 new projects put into operation.

Beginning in 2016, electrochemical energy storage began to see rapid new applications. Construction of new energy storage programs became “large, numerous, and popular.” According to CNESA statistics, from 2016-2017, the global combined total scale of projects planned or under construction was 4.7GW, with an increasing number of projects hoping to be implemented in the following year to two years. In order for large-scale electrochemical storage to meet the needs of power systems, the capacity of independent electrochemical storage systems has been ever increasing. Over 40 projects with a capacity of 10MW or more were recorded between 2016-2017. Popularity for energy storage applications has increased worldwide. According to CNESA statistics, in 2015, ten countries including the United States, China, and Germany deployed electrochemical storage systems. By 2017, close to 30 countries had implemented energy storage projects, demonstrating how energy storage has become increasingly globalized.

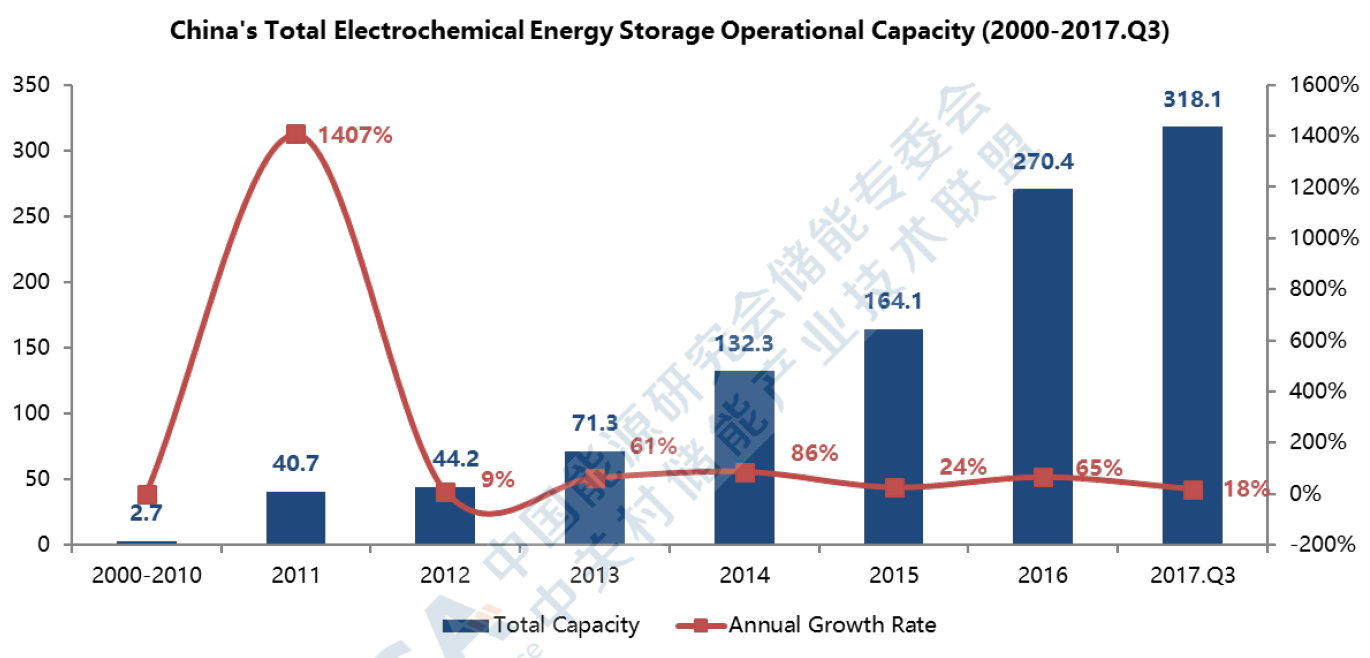

Yet it is the speed of China’s electrochemical energy storage development that catches the most attention. According to CNESA statistics, from 2000-2017 China’s total electrochemical storage capacity was close to 360MW, 14% of the world’s total, with an annual growth rate of 40%, surpassing the global growth rate. Between 2016 and 2017, China had nearly 1.6GW of capacity planned or under construction, 34% of the world’s total. China hopes to lead the industry’s development in the next few years.

2017: A Year of Policy Support for Energy Storage Around the World

As a country that developed policy support for energy storage at a relatively early stage, the United States has seen policies emerge across many states, starting in California and stretching to over 10 others, including Massachusetts, Oregon, and Hawaii. The United Kingdom, Austria, Czech Republic, Italy, Australia, India, and China all released energy storage development policies in 2017. Policy support, both in its depth of detail and breadth across regions, has proven beneficial for the rapid development of energy storage in 2017.

In October 2017, China released the first national-level energy storage policy for technology and applications support, the “Guiding Policies on Promoting Energy Storage Technology and Industry Development.” The “Guiding Policies” lays out support plans for energy storage in five different areas: support for energy storage equipment research, support for energy storage’s utilization of renewable resources, support for the use of energy storage in the stabilization and flexibility of power systems, support for energy storage in increasing smart-energy applications, and support for energy storage as a means of diversifying the energy internet. At present, Dalian, Yichun, Beijing, Handan, and other areas have already released local policies supporting energy storage. In the future, it is likely that more policies will emphasize the use of local resources and industry advantages at the provincial and city level. It is also expected that future policy emphasis will be placed on the creation of electricity market entrance mechanisms and price compensation mechanisms for energy storage.

Following California’s declaration of a 1.325GW procurement plan, Oregon, Massachusetts, and New York released their own energy storage procurement plans for electric utilities. New Mexico has already added energy storage to its list of resources for public utilities. Maryland has designated sites across the state for the design, construction, investment, and operation of renewable resource and energy storage programs. The United Kingdom and Australia are two countries that have seen rapid development of energy storage recently, with policy support following quickly behind. The British government has emphasized the use of energy storage as part of the strategy for its “smart systems and flexibility plan,” providing recognition for energy storage as part of the nation’s electricity market. Multiple regional governments in Australia have released incentive plans for storage installations, using subsidies to support behind-the-meter energy storage systems.

2017: A Year of Energy Storage Systems and Market Needs

Although industry development has intensified and policy support has gradually opened the market to energy storage, we cannot ignore the fact that the current driving factor for energy storage development is still policy. The road to profitable and commercialized energy storage is still full of challenges and uncertainties. Energy storage has become a closely watched “blue ocean” market. In 2016, worldwide investment in energy storage exceeded 4.33 billion dollars. Public acknowledgment and participation has given the industry confidence, yet as demonstrations gradually become marketized, independent, non-market demonstrations will end, and policy support will weaken. Energy storage must then operate and compete in the real market, and technological performance, system configuration, application models, the profit feasibility, and scientific methods must all come under market scrutiny. Energy storage has now entered the stage in which it must began to mature in the market.

In 2017, two separate battery storage projects, sized at 2.1GW and 4.8GW, were granted the opportunity to participate in the UK’s T-1 and T-4 capacity market auction. Yet controversy arose regarding the relatively short dispatch duration of battery installations, which limits their ability to handle pressure on electricity systems. After considering the fairness to long dispatch duration, non-energy storage technologies, the UK’s BEIS (Department for Business, Energy, and Industrial Strategy) conducted an evaluation, and, in December of 2017, decided to lower the de-rating factor for 30-minute duration batteries in the T-4 and T-1 capacity auctions. The ruling put new demands on energy storage systems that can provide flexible response in a short time duration. In the short term, the ruling can be viewed as a restriction on short duration storage in the capacity market, yet such a ruling also provides motivation for energy storage providers to develop long duration energy storage solutions.

The PJM market, which currently possesses 265MW of energy storage capacity in frequency regulation, has also recently update its regulations for the frequency regulation market. During periods of high ramp rate, the RTO requires large-scale generators or load switching to maintain balance. While decreasing the purchase of services classified as RegD (those that have fast ramp rates but limited power), the RTO has also increased the charge and dispatch rates for grid energy storage systems. This regulation update demonstrates how energy storage must now compete with other resources in a balanced market. How energy storage will profit and find a suitable place in the market under these new regulations remains to be seen.

The standardization of energy storage products is a much needed development. In Germany, 52,000 residential energy storage systems were installed in 2017. Demand for solar+storage systems for industrial and commercial applications is also quite high, yet growth has been challenged by a lack of product standardization, technological standardization, interface standardization, and standardization of commercial models. Additionally, standardization is needed for fire protection, health, safety, and other factors. If such issues are ignored, it will be difficult for energy storage to spread throughout Germany at a large scale.

As energy storage continues to marketize, market demands and technological capabilities will continue to conflict. As technology continues to become more feasible in the market, hardware, software, and interface performance will continue to not only improve but become more compatible with other equipment. In the electricity market, energy storage’s position, applications, and value will continue to shift and rectify itself in a positive direction. Within the power price mechanism, energy storage will continue to gain recognition as a means of replacing other power equipment. Energy storage will also need to work faster to create standards and regulations to satisfy the environmental and safety demands of users. These issues will, in the short term, cause energy storage’s development to slow, yet this is not a negative. The development of energy storage requires continuous exploration, trials, and even failures to fight for its place in the market and move increasingly forward. An industry that has passed the tests of the market is one that possesses the greatest competitiveness and ability to survive.

Ten Events that Defined Energy Storage in 2017

2017 was an exciting year for the development of the energy storage markets and projects. Looking back, the China Energy Storage Alliance (CNESA) has compiled a list of the 10 biggest events in the international energy storage industry for 2017.

1. United Kingdom: Capacity Market Regulation Reforms Deal a Blow to Short-duration Storage Systems

In July 2017, British electricity market players put pressure on the Department for Business, Energy and Industrial Strategy (BEIS), stating that battery storage could pose possible risk to the safety of electricity supply systems due to the fast speed in which such batteries discharge. In response, BEIS evaluated the possibility of such a risk and considered a reduction in the de-rating factor of short duration energy storage systems. In December of 2017, BEIS confirmed that T-4 and T-1 capacity auctions would receive sweeping reductions in de-rating factors for 30 minute duration batteries. This regulatory change is expected to severely reduce the benefit of short-duration energy storage projects and delivers a sharp blow to the future development of the capacity market for short-duration energy storage.

2. Australia: Announcement of 5-Minute Settlement Period Helps Compensate Fast-Response Systems

Australia’s electricity system operates at a five-minute power dispatch interval, yet prices are calculated at intervals of 30 minutes. Such a system is unable to distinguish between rapid and slow responses, meaning that systems that respond after 25 minutes would receive the same remuneration as those that respond immediately. The new five-minute dispatch interval changes the way in which power generation companies are paid for the electricity they provide, and supports those technologies, such as energy storage technologies, that provide fast response to electricity needs.

3. United States: Energy Storage Provides Power to the Grid After Southern California Gas Leak

The Aliso Canyon gas leak was the worst natural gas leak in the history of the United States, causing a severe electricity supply crisis in Los Angeles and San Diego. In 6 months, over 100MW of storage capacity was installed in southern California in response to the crisis. The incident served not only to highlight energy storage as a viable solution for grid emergencies, but also helped to decrease the dependence of the area’s power plants on natural gas.

4. Europe: More Energy Storage Subsidies/Incentive Plans Appear, Promoting Behind-the-meter Solar Storage

Following California’s SGIP policy and Germany’s solar storage subsidy policy, other countries and regions in Europe have released subsidies or incentive plans for distributed energy storage. Such measures promote large-scale applications of behind-the-meter storage. Austria’s parliament voted to provide long-term funding for countrywide PV projects from 2018-2019. Lombardy, Italy’s most economically developed region, now provides subsidies to customers who purchase and install energy storage systems. The Czech Republic’s Ministry of Industry and Trade has agreed to appropriate funds to support solar energy storage. These and other subsidy policies will help to stimulate the commercial development of behind-the-meter storage in Europe.

5. India: India’s Energy Storage Market Suffers Many Setbacks, But There is Potential for the Future

2017 was not a great year for India’s energy storage market. Although India holds a positive attitude towards energy storage development, many planned energy storage projects have been shelved or postponed due to a lack of sufficient funding or specifications. Such projects include the Pavagada and Kadapa solar storage project, which canceled bids after a sudden drop in PV prices, as well NTPC Ltd’s solar storage project on Andaman and Nicobar islands, which has seen continuous shelving of bids. The situation only began to improve during the latter half of 2017. In the future, as population rises, urbanization continues, and extreme weather conditions lead to more frequent electricity supply issues, India will face tough challenges in generating capacity and T&D infrastructure. Groups including the Indian government, distribution network operators, and public utilities, among others, are actively working to develop energy storage plans, industries, and business layouts. Looking forward, energy storage shows much potential for growth in India.

6. Global Policy Promotion: More Energy Storage Procurement Plans Released, Encouraging Rapid Deployment of New Projects

Following the opening of procurement planning after California’s AB 2514 bill, the U.S. states of New Jersey, Massachusetts, and Oregon, as well as Australia’s Victoria, Queensland, and South Australia, among others, have all enacted their own energy storage procurement goals for the support of establishing public utility-side storage projects. New York state is also in the process of enacting their own procurement goals. The creation and announcement of these public utility procurement plans is an important step in the promotion of large-scale grid-side energy storage.

7. Global Market Transactions: Mergers/Project Ownership Changes Fuse Technology and Capital

Large energy enterprises continued acquisitions of energy storage companies in 2017, including the acquisition of Demand Energy by European public utility company Enel, the acquisition of sodium-ion battery producer Aquion by China Titans, the acquisition of demand response company Restore by Centrica, and many other purchases. At the same time, many promising energy storage projects saw a change of hands, such as the purchase of RES and Belectric’s UK frequency regulation project by Foresight, and Enel’s purchase of another UK frequency regulation project through a contract signing with Element Power. Acquisitions of energy storage companies and projects by large energy groups reflects their recognition of energy storage’s potential and helps to encourage a merging of technology and investment in the market.

8. Popular Global Models: Virtual Power Plants Grow, Distributed Energy Storage’s Value Continues to Develop

Virtual power plant models have generally been easy to plan yet hard to construct. 2017 saw the implementation of a series of virtual power plants across the globe. Sonnen released a virtual power plant project involving 2900 Arizona homes. Sunverge implemented two separate virtual power plant programs, one in Australian public utility AGL’s service area, the other in Japan’s Tepco service area. Ireland’s International Energy Research Center announced plans for a community-level virtual power plant project. The popularity of these and other virtual power plant projects across the globe highlights the value of distributed energy resources to the grid.

9. Global Project Scale: The Value of Large-scale Projects to the Grid Becomes Clear

As the price of energy storage technology continues to fall, in 2017 planned or constructed energy storage projects have become less limited by initial capital, and project scales have become larger. These projects include developer Deepwater Wind’s large-scale wind energy storage project in coastal Massachusetts, the KEPCO and LG CNS plan for a large-scale solar plant in Guam, and Australia’s large scale combined renewable resource and energy storage projects. These projects are all within the tens of MWh or above, some even reaching 400MWh. The expansion of energy storage projects to a larger scale helps to verify how large-scale storage projects can add value to power systems.

10. Global Model Projects: Tesla Delivers World’s Largest Battery Storage System in Less Than 100 Days

On Dec 1, 2017, Tesla officially activated the world’s largest Li-ion battery system in South Australia. The project operates at 100MW/129MWh and utilizes a Samsung SDI Li-ion battery system. The project is connected to French renewable energy provider Neoen’s Hornsdale wind farm, providing stable clean power for South Australia. The project received much attention for its completion in under 100 days, and served to demonstrate how energy storage can alleviate power system emergencies in a short period of time.

Summary

The development of the international energy storage market has served to help China map its own technology developments, search for new business models, and reform related policies and mechanisms. Detailed information on how the international markets have developed will be included in the China Energy Storage Alliance’s 2018 White Paper, to be released at the 7th Annual International Conference and Expo scheduled for April 2-4, 2018

CNESA Storage Market Analysis Q3 2017

1. The Global Market

Electrochemical Energy Storage Programs Continue a Steady Growth

According to partial statistics of the China Energy Storage Association (CNESA), as of 2017 Q3, energy storage projects have reached a total worldwide operational scale of 169.2GW. Among these, pumped hydro occupies the largest number of installations at 97%. Electrochemical energy storage systems rank third in scale, at 2244.4MW, or 1.3% of the total, an increase of 15% from last year.

The third quarter of 2017 has seen a worldwide increase of 94.4MW in the total number of operational electrochemical energy storage projects, a 551% increase from Q3 of 2016, and 50% increase since Q2 of 2017.

Q3 Markets in the United Kingdom, Australia, United States, and China are Active

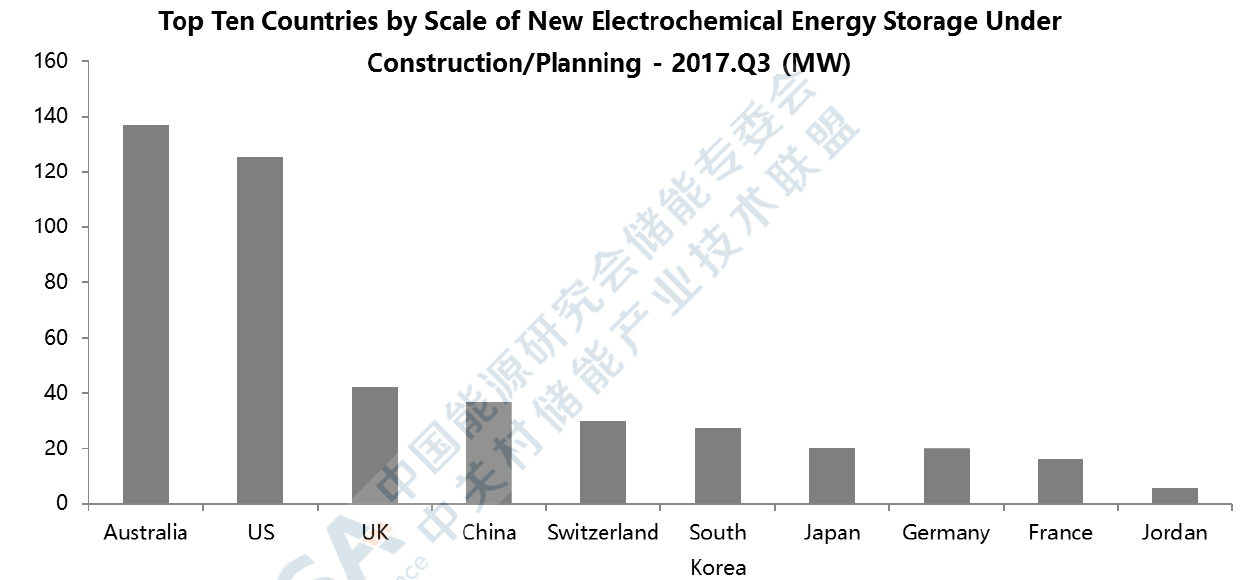

A comparison of worldwide Q3 increases reveals the UK, China, and Japan to be the top three countries with the largest scale of projects in operation. Projects in these three countries have all been dedicated to the renewable integration and ancillary service sectors. Australia, the US, and the UK rank top three in scale of projects under construction/planning, with 91% of such projects in these countries dedicated to renewable integration and the ancillary service sectors.

Ancillary Services Occupy the Largest Proportion of Q3 Market

In quarter three of 2017, the scale of global increase in energy storage projects has been largest in the ancillary services sector at 31.5MW, or 33% of the total global capacity. This is a 6200% increase since Q3 2016, and 75% increase since Q2 2017. Projects have largely been concentrated in the UK, Germany, and Belgium, such as the UK’s frequency regulation projects in Bristol and Darlington. The energy storage systems operate as independent electric stations, or in conjunction with gas turbines to provide a primary frequency control service for the European market.

Lithium Battery Enterprises Occupy the Top Four Spots in the Q3 Market