CNESA White Paper 2017

CNESA White Paper 2017

CNESA has published the 2017 English version of its annual Energy Storage White Paper, a comprehensive review of the storage industry in China and abroad. This year's report takes a special focus on the Chinese market, including China's top manufacturers and an overview of the power sector reforms laying the groundwork for the world's largest upcoming storage market.

Key topics include:

- China's storage market drivers

- Market breakdown by application, region, and technology

- Overview of key power sector policy reforms

- Global markets summary

We're happy to release this English summary version white paper for free. For more detailed and in-depth analysis, please refer to our Chinese-language version, available for purchase on our Chinese site.

To learn more about the Chinese energy storage market, please contact us.

CNESA Storage Market Analysis 2017 Q1

Global Movements:

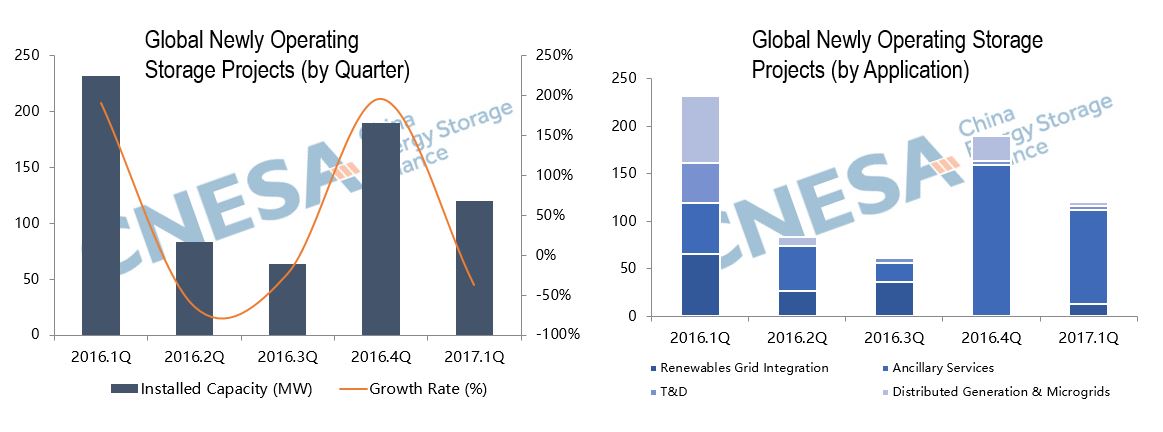

In the first quarter of 2017, newly operating electrochemical energy storage projects totaled 120 MW, a 48% increase compared to the same period last year, and a 37% increase compared to Q4 of last year. Projects were largely located in the United States, England, Finland, China, Australia, Denmark, and India.

Most of Q1's newly added capacity is devoted to ancillary services applications with over 99.1 MW. This represents a 87% increase since the same period last year and a 38% increase since Q4 of 2016.

Global Markets:

The most active states in the US include, California, New York, Texas, Hawaii, and Massachusetts, mainly addressing grid power shortages and increased grid flexibility. England placed emphasis on storage participating in frequency regulation and grid capacity services. German projects focused on large scale storage stations involved with balancing storage renewable energy generation output. Australian projects were mostly located in South Australia and focused on improving grid stability.

China Market Updates

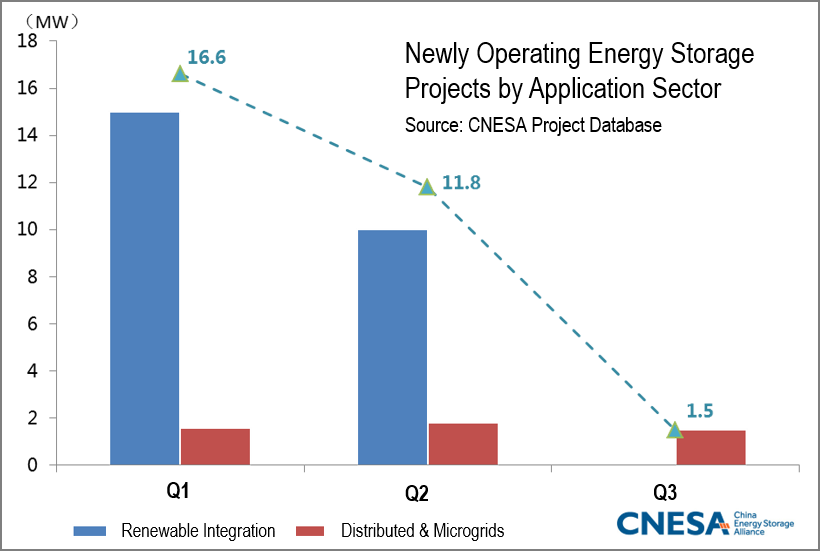

In Q1 of 2017, China added 1.25 MW of newly operating energy storage facilities, a 92% decrease from the same period last year and a 93% decrease since Q4 of last year. Newly added projects were all in the Eastern China region.

Nearly all of added capacity was in distributed energy and microgrids applications, growth in this sector increased 1150% from Q4 of 2016 decreased 93% since Q4 of 2016.

China Market Movements:

After the release of several national level “13th Five Year Plans” covering development and technology innovation roadmaps across energy sectors, several provinces began releasing provincial-level "13th Five Year Plans" and guiding opinions to cover future implementation plans.

Innovation Competition Winners Announced

This year, CNESA in collaboration with the China Association for Science and Technology, National Energy Administration, and China Energy Research Society kicked off the first annual energy storage Innovation Competition to recognize outstanding storage projects, technologies, and individuals for their contributions to the industry. The evaluations committee comprised of experts from Tsinghua University, the Chinese Academy of Sciences, and North China Electric Power University selected finalists from an open nominations process taking place from December 2016 to March 2017. Finalists chosen in each category were entered into an online voting platform via the Chinese messaging service, WeChat, where public votes accounting for a portion of the final score, the remaining portion of the score coming from the evaluation committee’s final deliberations in May of 2017.

On May 23, 2017, the winners were announced during the opening ceremony of the 6th Annual Energy Storage International Conference & Expo. CNESA offers congratulations to the entries listed below and a heartfelt thanks to all who participated in this year’s competition.

Applications Prize - Top 10

| Company Name | Project Name |

|---|---|

| Guangdong Power Grid | Model Demonstration Multi-Purpose Energy Storage Systems and Internet Operations |

| Sacred Sun | Sacred Sun Nima Storage Project |

| Dalian Constant Current Energy Storage Co., Ltd. | Dalian Flow Battery Peak Shifting National Demonstration Project |

| ABB | Hokkaido Island Project (Japan) |

| Shenzhen Advanced Clean Power Technology Research Co., Ltd. | Relzow 100/200MWh Li-ion Battery Project (Germany) |

| Pride Power | Mobile EV Charging Station System |

| State Grid EV Service Co., Ltd. | Highway Service Station “Solar + Store + Charging” Demonstration Project |

| Huaneng Clean Energy Research Institute Co., Ltd. | DC PV + Storage System Develop and Coordinated Operations Research |

| Jinhe Energy | Altay, Xinjiang Wind Clean Energy District Heating Model Demonstration |

| Narada Power | Xuzhou Silicon Industries Peak Shifting Storage Station |

Technology Prize - Top 10

| Company Name | Technology Name |

|---|---|

| Chinese Academy of Sciences Institute of Thermal Physics | Advanced Compressed Air Energy Storage System |

| Tsinghua University-Affiliated Petroleum Resources and Engineering Co., Ltd. | 1MW/60MJ Flywheel Storage System |

| Ningbo New Energy Technology Co., Ltd. | Supercapacitors for City-Wide Public Transportation Applications |

| Chinese Academy of Sciences Shanghai Institute of Ceramics | High energy density Li-ion battery ceramic-based ion conducting electrolyte |

| Shuangdeng Group | Super Carbon Battery |

| SPS-Cap | New High Energy Density Supercapacitor Applications in Rail-Based Vehicle Energy Storage |

| Soaring Energy | Black Start Key Technology and Applications |

| Jiangsu Smart Energy Storage Technology Co., Ltd. | Molten Salt Thermal Storage in Thermal Power Plant Applications |

| C&D Technologies | Novel Lead-Carbon Battery Technolgoy |

| Nova Greentech, Inc. | Restructurable Battery Network and Software Defined Battery Control and Management System |

Leadership Prize

陈海生 Chen Haisheng Vice-Director, China Academy of Sciences Institute of Thermal Physics/ Chair, China Energy Research Society Energy Storage Committee

张华民 Zhang Huamin Head Scientist, Chinese Academy of Sciences Dalian Physical Chemistry Research Institute

王仕城 Wang Shicheng Chairman, Beijing Soaring Electronics Co., Ltd.,

陈博 Chen Bo General Manager, Narada Electric

魏银仓 Wei Yincang Chairman, Yinlong Energy

Innovation Grand Prize

| Company Name | Project Name |

|---|---|

| Sacred Sun | Sacred Sun Nima Storage Project |

Lifetime Contribution Prize

杨裕生 Yang Yusheng Scholar, Chinese Academy of Engineering

ESIE 2017 Wraps Up 6th Successful Year

CNESA’s 6th Annual Energy Storage International Conference & Expo ESIE was held May 22-24, 2017 at the China National Convention Center. Our biggest event to date included 2000+ representatives hailing from 20 countries convening in Beijing for three full days of expo hall activities, conference forums, and business networking.

This year’s event was guided by the National Energy Administration and supported by the Zhongguancun Park and China Energy Research Society.

Day 1 Pre-Conference Events

APEC workshop speakers and attendees

Pre-conference events included the culminating workshop of CNESA-organized APEC-sponsored research project, “Research on Energy Storage Technologies to Build Sustainable Energy Systems in the APEC Region.” Expert speakers from the Pacific Northwest National Laboratory, Asia Development Bank, World Energy Council, China’s Development Reform Commission, and ABB all presented on the status of energy storage development, policies, and recommendations for implementing Energy Storage technology in the APEC region. Government representatives from Chile, Malaysia, and Thailand were also present.

Representatives from CNESA's 160 member companies attend the annual member's meeting

Monday’s events also included the CNESA annual member’s meeting where alliance leadership briefed members on the accomplishments to date set the strategic development plan for the upcoming year.

Day 2 Events

The opening ceremony with an attendance exceeding 2,000 included keynotes from government leaders from the National Energy Administration, Chinese Academy of Sciences and National Center for Climate Strategy. CNESA Secretary General Tina Zhang also announced the publication of the 2017 Energy Storage Industry White Paper along with the report’s key findings, including the CNESA forecast for 44 GW of energy storage across all technologies by 2020.

CNESA Secretary General, Tina Zhang, presents key findings from the 2017 white paper

Government leaders tour the expo floor and connect with industry representatives to learn about new technologies

It was also during the opening ceremony where results from the 1st Annual Energy Storage Innovation Competition were announced.

Meanwhile on the expo floor, team of government representatives from regulatory and rule-making bodies made an official tour, connecting with industry players to better understand the promises energy storage technology can offer China’s power system.

International panelists discuss storage markets across the globe

Afternoon sessions included break-out forums on solar + storage and the analysis of global markets and policies. The international forum, drawing from CNESA’s vast international network of association partners included speakers from the US Department of Energy (USA), Asia Development Bank (Korea), the European Association for the Storage of Energy (Belgium), CSIRO (Australia), Germany Trade & Invest, and the India Energy Storage Alliance.

Day 3 Events

The culminating conference day was organized around parallel discussion tracks covering technology frontiers, grid-side applications, the “Internet of Energy,” and the economics of storage.

CNESA researcher Ning Na discusses storage economics

Christopher Molnar of American company, Chromalox, presents on thermal storage solutions

Next year's event is scheduled for April, 2018 in Beijing, China. We hope to see you there!

CNESA Delegation Completes US Visit

This April, a CNESA-organized group totaling 15 representatives from Guangdong Power Grid and CGGC-UN Power traveled to Denver, Colorado as part our alliance partner's event, the Energy Storage Association 27th Annual Conference & Expo. Over a packed seven-day itinerary, our delegates attended conference seminars, toured national research facilities, and met with some of the country’s leading figures in the storage industry.

The conference, sponsored by RES and Xcel Energy, included over 2,000 attendees, 70 exhibitors, and 160 speakers in three days of official events. Our trip also came at a crucial time during the US industry development. As AES Energy Storage co-founder and President John Zahurancik noted, “While it took us 9 years to install the first 100 MWh's of energy storage capacity in PJM, we just completed more than that in California in under 5 months. This growth and acceleration are immense, in the US and around the globe. We are changing the way that utilities and grid operators think about the grid - building towards 35 GW's by 2025 and beyond."

Colorado Governor Mark Hickenlooper (left) discusses Colorado's energy future with ESA Director Matt Roberts.

ESA Director, Matt Roberts, continued with a call for 35 GW of installed energy storage in the United States by 2025.

On the Expo Floor:

Among ESA’s 70+ exhibitors Guangdong Power Grid benefitted from a booth providing a platform to meet with representatives from national laboratories, non-profits, and leading industries. In particular, it was intriguiging to see so many storage providers working outside of the battery-sphere, which currently dominates both the Chinese and global energy storage market.

Of CNESA’s 140+ alliance members, we also ran into representatives from member companies BYD, Sunwoda, NR Electric, LG Chem, Samsung, Sungrow, ABB, Parker Hannafin.

Panasonic Pena NEXT Station and Microgrid:

Our first site tour of the trip brought us to Panasonic’s Pena NEXT Station and Microgrid demonstration project. Located along the rail line linking Denver International Airport with downtown Denver, Pena NEXT has become a testing ground for energy storage, renewables grid integration, and smart network microgrids under a newly forged public-private partnership among Panasonic, Xcel Energy, and the City of Denver. The first stage of the project development includes an 800-space PV-covered carport owned by the Denver International Airport and Panasonic’s U.S. operations hub. The site also features smart, IoT-enabled street lights operated in conjunction with the University of Chicago/Argonne National Laboratory and 1 MW/2MWh lithium-ion battery system installed by Younicos.

The project has been granted $10.3 million in funding Colorado Innovation Clean Technology (ICT) Program. Denver International Airport in turn purchased ownership of the carport for $2.7 million and Panasonic contributed $1.7 million in the rooftop solar PV installation along with other consruction, maintenance, and labor costs (excluding the new Panasonic facility).

National Renewable Energy Laboratory (NREL):

The National Renewable Energy Laboratory, with its main campus in Golden Colorado, is the Department of Energy’s central laboratory for renewable energy research in the United States. During our visit we had the pleasure of speaking with the head of international programs, Dr. John Barnett, who introduced scope of NREL’s international projects including their collaborations with the Chinese National Energy Administration and the National Development and Reform Commission. We then listened to presentations from two researchers focusing on optimizing lithium-ion batteries and the laboratory’s work in hydrogen fuel research.

Our visit wrapped up with a tour of the NREL’s Energy System’s Integration Facility which provides a controlled laboratory environment in which the properties of integration of both residential and commercial loads can be investigated and optimized.

NREL National Wind Technology Center:

The NREL also maintains the National Wind Technology Center focusing on wind technology and comprehensive equipment testing and certification. During this visit we saw the world’s sole facility with two dynamometers fully integrated with wind and solar in the field. The site also includes a 1 MW/1 MWh lithium-ion battery system installed by RES.

University of Colorado Boulder:

During our final visit we headed to University of Colorado, Boulder campus to speak with Professor Frank Barnes who previously headed the Electrical Grid and Energy Storage Research Group at the university. During the visit our representatives discussed the status of compressed air energy storage systems development in the United States along with potentials for CAES systems in China.

Energy Storage Association is America’s nation-wide industry association representing over 225 companies. As co-founding members of the Global Energy Storage Alliance, ESA and CNSEA have worked closely together and look forward to future collaborations. We would like to extend a big thank-you to our hosts at ESA, the NREL facilities, Panasonic, and University of Colorado Boulder.

It's Time for Storage: CNESA Chairman Johnson Yu

CNESA Chairman Johnson Yu

CNESA Chairman Johnson Yu has been a key player in China's burgeoning energy storage industry, first beginning in 2006 when his vanadium flow battery company was awarded tender in one of the world's largest projects of its kind, the Zhangbei Hybrid Wind & Solar Pilot Demonstration. His next venture provided ancillary services to China's national grid operator State Grid. It was during this time he also founded the China Energy Storage Alliance.

The following is a recent interview with NengJian App. The interview has been translated from the original Chinese.

Q1: HOw would you describe the current stage of china's storage industry development?

We can divide the industry development into three stages. The first was technology verification (2000-2010) mostly consisting of launching basic R&D and technology demonstrations. The second stage (2011-2015) was the demonstration stage. As technology advanced, new ways to apply storage became increasingly clearer. Starting in 2015, energy storage entered a transition period, from demonstration to commercialization.

With regards to technology itself, the development of electric vehicles has brought about substantial drops in costs. Last year, storage commercialization began in China.

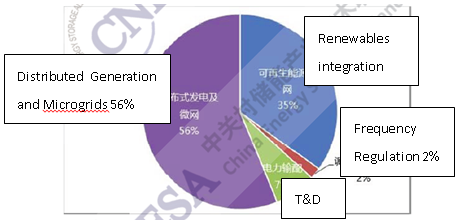

With the myriad of demonstration projects underway, the applications for storage technology are taking shape. China's main application sectors are currently distributed generation & microgrids, large-scale renewable energy integration, frequency modulation, in addition to ancillary services.

In the upcoming year, we expect China's installed capacity to double - both behind and in front of the meter.

Just recently the NEA published the “2017 Guiding Opinions on Energy Development” highlighting several projects expected to be completed by the end of the year. These include projects in Suzhou (Huiteng), Tibet (Nima), Dalian (Dalian Rongke), Changsha (BYD), Shanxi (Sungrow), and in Bijie, Guizhou.

Q2: How effective has policy support for energy storage been in 2016?

In 2016, several industry-focused Five Year Plans, including the “13th Five Year Plan for Energy Development,” “13th Five Year Plan for Renewable Energy Development” and the “13th Five Year Plan for Power System Development” all clearly indicated support for increased efforts in research & development and model demonstrations both in large-scale and distributed storage applications.

The NEA also issued policy documents with significant implications for storage industry commercialization. In February there was the “Guiding Opinions on Promoting the ‘Internet+’ Smart Energy Development” (关于推进“互联网+”智慧能源发展的指导意见) which included sections directly related to storage, including "Promoting Centralized and Distributed Storage Collaboration" and "Developing Storage Networks and Informatization." While these documents may be of a "guiding nature," they have had a clear impact on industry growth and are responsible for a surge in storage technology companies applying for authorization of project demonstrations. If you take a look at the recently released roster of approved "Internet of Energy" projects you see many projects with storage directly mentioned in the title.

In June the NEA released its first policy that directly supported energy storage: “Announcement on Promoting Electrical Storage Participation in Ancillary Service in the ‘Three Norths’ Region.” This allowed storage resources to be constructed at power generation sites to provide peak services and frequency modulation, or participate as an independent resource in the ancillary services market. The "Three Norths" policy is similar to the U.S. FERC Order 755, instituting a “mileage-based’ payment mechanism based on performance to increase the effectiveness of the compensation mechanism.

Q3: What are CHina's most profitable storage applications?

Pumped hydro can generate earnings through both capacity and electricity pricing schemes. Non-pumped hydro technologies can combine local storage subsidies with strategically storing and discharging energy during peak and off-peak times to save on power bills. This is currently the most profitable storage scheme in China.

In northern China ("Three Norths" Region), storage can provide frequency modulation services for thermal power generation plants through compensation and penalty schemes for profit.

Q4: What work remains in order to commercialize energy storage?

In the industry's early stages, subsidies are a must. However, in the long term a healthy industry development also needs to rely on free-market principles.

Power systems and the storage industry are also interconnected. China is currently enacting broad-reaching electricity system reforms. However, despite storage's widely acknowledged importance, the market mechanisms that make storage commercially viable, like spot markets and ancillary service compensation, have yet to be instituted nation-wide.

Under ideal market conditions, storage companies would only need to work on optimizing the quality-to-price ratio. America has reached this stage. China's storage players have to gain government approval for project demonstrations while also lobbying for policies to allow them to eventually enter the market.

Q5: In the 13th Five Year Planning Period What kind of DEVELOPMENTS can we expect to see?

Energy storage currently has an investment return period between 7 to 9 years. In addition to this, its ROI, usually less than 10%, limits the attractiveness of investing in storage technology to low leverage companies or banks. Due to continuous breakthroughs in battery technology, we do foresee that 2017 will be a break even point for storage investment; at the latest this would happen by 2018.

CNESA expert committee member, Lai Xiaokang, from the Chinese Academy of Sciences predicted back in 2012 that to in order to break even, storage systems need to exceed 5000 cycles with costs below CNY1500 per kWh. I agree with this prediction.

Coming up in 2017 we have several projects under first round of "Internet of Energy" pilot demonstrations as well as many hybrid energy optimization projects. Following this trend towards distributed energy resources, storage applications will also have a corresponding increase. During the National People's Congress that just convened in March we were also very pleased to see a proposed development plan titled "Distributed Energy + Storage."

Q6: Do you think one storage technology will become dominant in the upcoming years?

It's hard to answer this question without considering specific applications. As a whole, I believe that in the upcoming 10-15 years many storage technologies will co-exist. Just look at Li-ion, which in itself already includes several other technologies like lithium iron phosphate, lithium titantate, lithium sulfur, lithium metal, etc. These all will continue to develop. Aside from the lithium chemistries and advanced lead batteries, there's also compressed air, flow batteries, Na-ion, aluminum, and magnesium batteries we should also keep an eye out for in the future.

Q7: What are your thoughts on the latest lithium Titante batteries?

Again, to properly evaluate a technology you have to consider its application context. Lithium titanate batteries are relatively safe and long-lasting. If users can accept using these batteries over a long period then they are very competitive. However, if the user only wants to make a single investment and recover costs within 3-5 years, traditional Li-ion batteries are more appealing.

Q8: What has CNESA done to Promote energy storage commercialization?

CNESA is currently organized into four branches: our alliance members, expert's committee, research think tank, and financial services assistance.

We work closely with Chinese industry leaders and government agencies along with collaborating with foreign companies and alliance organization partners. From the laboratory to marketplace, from domestic to international, we follow it all. Our research results are summarized in our annual white paper.

With respect to promoting policy change, we are highly engaged in this field. Last year, on April 7, 2016, the NDRC and NEA jointly published the "Energy Innovation Action Plan (2016-2030)" to delineate China's energy innovation goals. CNESA organized our alliance expert's committee and industry members to contribute to the content and editing of the section titled, "Innovation in Advanced Storage Technology."

Our alliance also firmly believes that acquiring capital investments should not limit promising emerging technologies, and as such we are committed to helping startups build relationships with investors. Next month at our annual Energy Storage Conference & Expo, we will be holding the First Annual Energy Storage Innovation Competition. Our investment partners will be in attendance to learn more about promising technologies.

Q9: Any advice for upcoming storage entrepreneurs?

There are no set rules to be an entrepreneur, everything depends on your ideals and convictions. At present, industry observers often say that whoever can establish a viable business model before power markets are established will become successful once these power markets begin operating. Companies with a wide-range of resources, say for example microgrid design or business/construction management, if these companies expand to include storage operations it will be easier than for companies emerging directly from the laboratory. However, uncertainties in markets and emerging storage technologies still bring opportunities (as well as risks) to startups.

All this uncertainty is a good thing since uncertainty is a prerequisite for creativity. I'd say now is the time to get in the market, since things will only pick up from here. You need to have three key requirements: a team, a technology, and a business model. Even if you only have one of these components, you can still enter the market and work on building up the others.

CNESA Storage Market Analysis 2016 Q4

Global Movements:

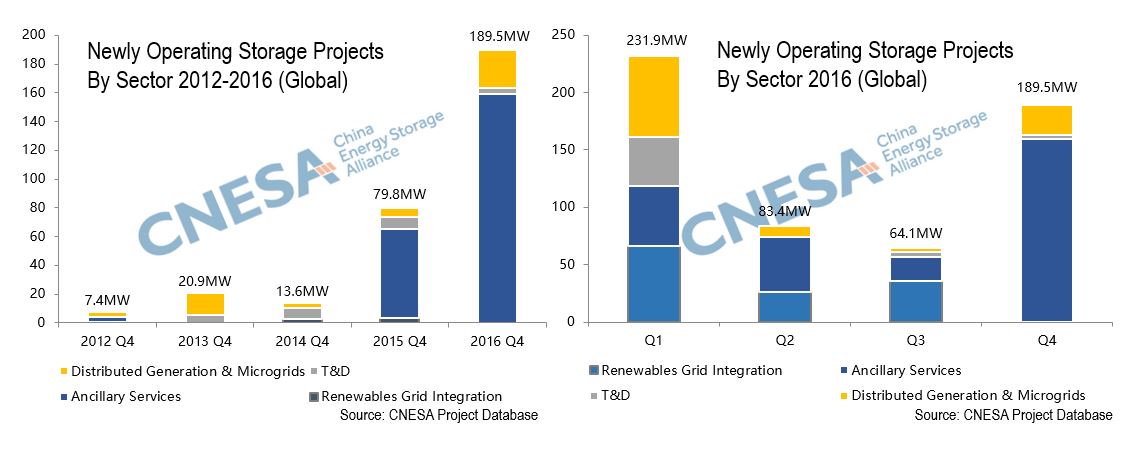

In the 4th quarter of 2016, 37 storage projects totaling 189.4 MW began operating across the world. This represents a 95% increase over Q4 of 2015 and a 164% increase compared to Q3 of 2016. Over the past five years 2012-2016, installed storage capacity showed a CAGR of 125%. Total capacity installed during Q4 of 2016 also marked a 137% increase when compared to the same period last year, and a 196% increase since the previous quarter.

In 2016 Q4 84% of installed capacity was in the ancillary services sector, while distributed generation and microgrids came in 2nd with 14% of installed capacity. The ancillary service sector saw a 155% increase compared to Q4 last year and a 677% increase since last quarter, while the distributed generation and microgrid sector increased by 317% since Q4 last year and 748% since last quarter.

Global Markets:

US: California and New York state were the most active markets this quarter. Market developments were also accompanied several announcements of storage-related policy.

Europe: England saw the most activity in Q4 especially with storage's participation in grid-side applications and capacity markets.

APAC: Australia's storage deployments focused on residential solar + solar and centralized large-scale solar fields. Japan and India also deployed storage in large-scale solar fields.

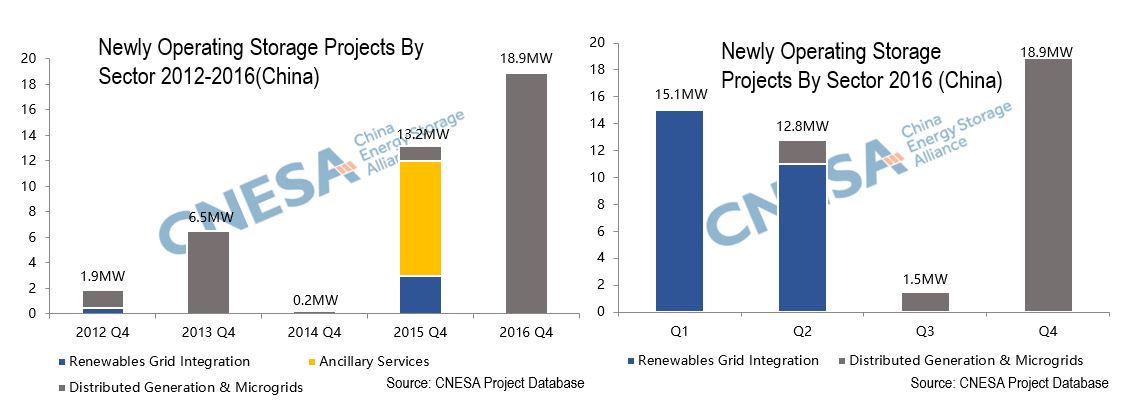

China:

In Q4 of this year 10 projects came online with representing a total capacity of 18.9 MW. This marks a 25% increase over same period last year, and a 233% increase compared to Q3 of 2016. China's five-year installed storage capacity CAGR from 2012-2016 is 78%.

Q4 storage projects were largely in the distributed generation and microgrids sector, this sector has a five-year capacity CAGR of 92%, Distributed gen. & microgrid capacity increased by 147 % compared to Q4 last year and 116% compared to Q3 of this year.

This quarter, 85% of of operating capacity came online in China’s southwestern region, 9% in the East China, and 6% in South China. Projects along the coastlines of Southern and Eastern China focused on price arbitrage helping commercial users looking to save on energy bills. Projects in Western China aimed at increasing renewables consumption.

China Market Movements

Policy: on the national level several major related policy documents were released including the 13th Five Year Plan for Power Sector Development and 13th Five Year Plan for Renewable Energy Development as well as the National Electricity Demonstration Project Management Guidelines. Provincial and local policy developments were largely focused on multi-province electricity reform trials along with announcing ancillary service market operation regulations in China’s northeast.

Industry: Domestic market activity centered around construction of production centers, and launching project demonstrations individually and in coordinating with local governments, design institutes and other work units. Chinese engagement in the foreign markets largely involved establishing subsidiary companies and joint ventures as a means to enter local markets abroad and increase sales volume.

About the Tracking Project

CNESA began the "World Tracking Report" in 2017 to synthesize and share the data collected in the CNESA project database. Interested parties are welcome to contact the CNESA research department to understand more.

Beijing’s Demand Response Pilot: A Review

Since the launch of city-wide demand-side electricity management trials across China in 2013, the cities of Beijing, Shanghai, Suzhou, and Foshan have established their own demand response resource pools. Jiangsu Province also began demand response pilot spanning the entire province, and in the summer of 2016, implemented the world’s single largest (by load volume) demand response event to date. Through three years of trial periods, China’s demand response programs have largely been co-administered by the government and grid enterprises. Large-scale load aggregators have also played a supporting role integrating both business and residential power users, and several business and residential users have also taken the initiative to participate in demand response programs directly. In this article, we will provide an overview of Beijing’s city-wide demand response pilot as well as provide an outlook for the implementation of future demand response programs in China.

Beijing's demand response program was coordinated through the online DSM platform.

Beijing Demand Response Pilot Implementation:

Large-scale load aggregators played an important role in systematically organizing Beijing’s demand response participants who opted-in to the program. Users with the capabilities to manage their own energy resources, however, were encouraged to participate independently to encourage the spread of energy informatization. The program was modeled on a six-step system: 1) contract agreement; 2) demand response event dispatch; 3) load allocation; 4) response feedback; 5) load reduction implementation & monitoring; and 6) verification.

The efforts of the 2015 pilot focused on the best ways to ensure stable grid operations and air quality during high-pollution periods. In the 2015 pilots, Beijing’s Municipal Electricity Demand-Side Management Platform served as the base for data collection and implementation of demand response events, though, alternative models comparing government-lead versus grid enterprise-lead implementation were also considered and explored.

Beijing DR trial implementation organization.

Platform Organization:

The demand response software accessible via Beijing’s Municipal Electricity Demand-Side Management online platform was used to serve load aggregators, collect the 15-minute interval real-time monitoring of user responses, set day-ahead response plans, notify aggregators of demand response plans, and request feedback to allocate the demand response load volume. In the event that demand response feedback indicated the currently allocation could not meet dispatcher needs, the demand response software automatically adjusted the allocations to meet the requirements and implement the plan. After the end of a demand response event, the software system calculated the baseline load volume and carried out secondary calculations to correct for incomplete data or errors.

Compensation:

In the 2015 pilot, compensation levels were determined by participation category, providing compensation based on how far in advance users were notified before a demand response event. Notice times were 30-minute advance notice, 4 hours advance notice, and 24 hours advance notice. The 30-minute advance notice group received a payment of CNY 120/kW, the 4-hours advance notice received CNY100/kW, while the 24-hours advance notice group received CNY80/kW.

Program Principles:

The 2015 demand response commitment contract clearly states that the number of demand response events will not exceed 10, with each event’s load reduction to not exceed the total capabilities of the aggregated resource pool. The compensation was allocated according to the actual hourly response during each demand response event. Demand response events occurred only during the summer and winter seasons, with compensation calculated individually per season, with the total payment made after the end of the winter season. The total demand load was calculated according to the principles set forth by the National Development and Reform Commission in conjunction with the Beijing Municipal Power Demand-Side Management Service Platform. A third-party made additional verifications of response implementation, and payments were made in line with the established payment methods.

Implementation Highlights:

In the summer of 2015, the Beijing Municipal Grid experienced record-breaking grid loads.

On August 12 and 13, grid dispatchers organized 17 load aggregators and 74 individual users to participate in a demand response event, shaving 57 MW off of the peak load.

Between August 20 and September 2, 2015 two large events hosted in Beijing, the 70th Anniversary Celebration Commemorating the end of WWII along with the World Track and Field Championships represented a massive strain on the grid load. Beijing officials organized load aggregators and individual users to decrease demand during peak hours 2-3 hours each day over a 10-day period, ultimately shaving an accumulated 430 MW from the grid load.

Additionally, in winter 2015, the city municipal government issued several severe smog alerts. Beginning December 1st, officials organized 19 load aggregators and 136 individual users participated in seven demand response events lasting 14 hours each. According to preliminary estimates, this achieved a largest single-event load reduction of 170 MW.

User Analysis:

Power users participating in the 2015 Beijing demand response pilot were divided among industrial users, public facilities, and residential users. According to the cumulative data for the year, industrial users represented 93% of response volume, mainly in the manufacturing and mining sectors. Public facilities, including office buildings, hotels, business buildings, and sports arenas made up the other 7% of response volume. Residential users made up a relatively small portion of the 2015 resource pool with 0.4% of response volume, but this does not diminish the value of integrated residential response resources as a meaningful and important asset in future demand response programs.

Response Strategy:

During response events, industrial users controlled their electricity use through adjusting the use of manufacturing equipment. A portion of industrial users also adjusted climate controls, lighting, and ventilation. Public facilities generally acted in demand response events by modifying temperature controls and lighting, some even drawing from energy storage reserves to power their operations.

There were three load aggregators that combined residential users as a demand response resource. Among them, one aggregator used heating and cooling controls to organize residential users in a small apartment block to participate in demand response. The other two residential aggregators used smart controls of electric appliances including air conditioners, hot water heaters, and water coolers to coordinate response steps remotely.

Thoughts on Next Steps:

As China is in the midst of upheavals reforming the electricity system and demand-side management, demand response is very likely to remain in the trial mode for the near future. As they stand, current electricity markets are unable to support full adoption of demand response markets, meaning governments and grid enterprises will still play a key role in the upcoming years.

The trial stages have afforded provincial and municipal governments the chance to experiment with different implementation methods. One innovative policy in Jiangsu Province collects revenue from electricity sales during critical-peak times* to support the implementation of demand response programs. This reflects an economic equality among electricity price earnings and demand response value. Based on this method, many other cities could set up demand response program funds, and ensure applications of demand response.

The Need for Marketization:

Not all participants in demand response are driven my free-market principles, as in some administrative regions some users are effectively forced to participate to avoid even greater economic losses through imposed fines and penalties. While on the one hand, it’s important to begin the transformation to increase marketization of demand response instead of emphasizing fine-tuning the operational logistics, there remains much work to be done regarding investment costs, earnings calculations, and economic incentives as China undergoes series of power system reforms.

Conclusion:

During the trial period each trial city called upon load aggregators and electricity users to carry out demand response events but cutting down on their respective loads. Promising future directions include, participation via price competition, and the use of smart technology to coordinate alerting users of an event, the duration of the event, and controlling electric appliances. The demand response platform likewise can improve through providing more concrete services for government agencies, load integrators, and electric users in order to achieve an optimal and efficient coordinate demand response effort and ultimately ensure safe grid operations.

2016 and Beyond:

The Beijing municipal government has spent the 2016-year reviewing data from the 2015 trials. There was no demand response program for the 2016 period. We are awaiting announcements for plans for a potential 2017 demand response pilot continuation.

*Electricity price designation for the most expensive portion of “on peak” electricity.

This article has been translated from the original Chinese.

Energy Storage Innovation Competition - Calling for Entries

International Competition for Innovation in Energy Storage

The China Energy Storage Conference and Expo was founded in 2012 with the support of the National Energy Administration and Zhongguancun Science Park. Now China’s most influential exhibition and conference covering the energy storage industry, China Energy Storage Conference and Expo serves as a platform to showcase the latest developments in storage solutions as well as promote policy changes and commercial applications of storage technology. In 2017, the International Competition for Innovation in Energy Storage was founded to recognize outstanding technologies, projects, and individuals for their contributions to the industry.

Entry Categories:

Prizes will be awarded to outstanding entries in the following categories:

Technology Prize:

To be awarded to the top 10 energy storage technologies/products. Nominations open to the general public for entries in the following categories:

- Physical storage

- Chemical storage

- Other storage technologies (supercapacitors, fuel cells, etc.)

- Battery systems (inverters, management systems, software, systems integrators)

- Energy storage solutions

Applications Prize:

Will be awarded to the top 10 applications in energy storage projects. Nominations will be open to the general public for entries in the following categories:

- Utility-scale, centralized, grid-connected applications (distribution/transmission-sited, ancillary services, etc.)

- Distributed projects (industrial, off-grid island storage, etc.)

- User-sited projects (residential systems, EV charging stations, military, data centers, etc.)

Leadership Prize:

Will be awarded to 5 outstanding individuals in the energy storage industry. Nominations will be open to the general public

Lifetime Contribution Prize:

Will be awarded to 1 individual who over his or her lifetime has made outstanding contributions to the progress and development of the energy storage industry. Nominations will be made by the expert’s committee, voting open to the general public.

Innovation Grand Prize:

Will be awarded to 1 entry from the Technology and Applications categories, as selected by the Evaluation Committee.

Winner Benefits

Innovation Grand Prize: The Innovation Grand Prize winner will receive an award of CNY 10,000

Promotion and Exposure. Winners will be given several opportunities to increase their exposure. At the 2017 International Energy Storage Conference and Expo conference, winners will be featured in the exhibit hall, connecting them to over 4,000 energy storage professionals from around the world. Select winners will also be invited for speech opportunities at the awards ceremony. Outside of the conference, winners will also have promotion opportunities through conference media partners, who will feature winning entries, as well as through official releases on CNESA media channels, including the conference website, WeChat, Twitter, etc.

Financial Support. Winners will have the opportunity to schedule one-on-one consulting services with Northern Light Venture Capital, Kaiwu Investments, Tus Holdings, Tsing Capital, DGJ, IDG Capital, and Sequoia Capital.

Project Recommendation. Winning projects will be directly forwarded to related government agencies to assist in gathering government-backed support. Winning projects will also be nominated for the China Energy Research Society’s “China Energy Innovation Prize.”

CNESA Membership Services. Winners will receive a free year of membership in CNESA, a copy of the complete edition of the 2016 white paper, and CNESA project evaluation services.

How to Nominate:

The nomination form and submission instructions can be accessed on the official competition website.

Competition Timeline:

January 6, 2017 – March 10, 2017: nomination period opens. Nominations for the Technology, Applications, and Leadership Prizes can be submitted on the official conference website

March 11, 2017 – April 30, 2017: Voting period opens (all categories)

May 22, 2017: Winners chosen

May 23, 2017: Awards presented

The nomination forms and voting portals will be hosted on the official conference website. Winners will be selected by both the recommendations of the Experts Evaluation Committee along with online votes (accounting for 20% of total score).

Competition Organization:

Guiding Organizations: Chinese Association for Science and Technology, National Energy Administration

Hosting Organization: China Energy Research Society

Undertaking Organization: China Energy Research Society Energy Storage Committee/China Energy Storage Alliance

Supporting Organizations: Global Energy Storage Alliance, California Energy Storage Alliance, Zhongguancun Advisory Board, Beijing Haidian Science Park, Tsinghua University Department of Electricity Systems, China Academy of Sciences Institute for Thermal Physics, Chinese Academy of Sciences Physics Research Institute, China Academy of Sciences Dalian Physical Chemistry Research Institute, China Electric Power Research Institute Department of Electrical Engineering and New Materials, Tsinghua University Energy Internet Innovation Research Institute, ENF Nengrongwang

Advisory Committee: Shi Dinghuan, Yi Baolian, Wu Zongxin, Yang Yusheng, Chen Liquan, Zhou Xiaoxin, Cheng Shijie, Yu Zhenhua (chair)

Experts Evaluation Committee: Chen Haisheng, Lai Xiaokang, Xia Qing, Zhang Huamin, Li Hong, Hu Xuehao, Jiang Liping, Wang Zhiming, Yue Jianhua, Guo Jiabao, Wang Zidong, Wen Zhaoyin, Yi Jin, Janice Lin, Mou Liufeng, Zhao Bo, Li Junfeng, Gao Feng.

China's Top 10 Storage Headlines of 2016

China's domestic storage industry made steady progress in 2016. Electricity system reforms continued to roll out while new regulations in China’s "Three North" Region (三北) allow storage to provide and receive compensation for ancillary grid services. All of these and more contributed to the industry's continued growth as well as carving out market space for future storage technologies. China Energy Storage Alliance (CNESA) has closely followed the market developments this year, and here are the top 10 take-aways.

1) Storage Listed as "Key Technology" in National Energy Action Plan

On April 7, 2016, The National Development and Reform Commission (NDRC) along with the National Energy Administration (NEA) jointly released the “Action Plan for Innovation in the Energy Technology Revolution (2016-2030)” 《能源技术革命创新行动计划(2016-2030年)》classifying energy storage as one of the 15 “key technologies” to develop over the upcoming 15 years. CNESA’s Expert Committee along with Alliance industry members worked together providing contributions to the “Innovations in Advanced Storage Technologies” section.

The Action Plan laid out goals for 2020, 2030, and an outlook for 2050 regarding thermal storage, compressed air storage, flywheel storage, high temperature superconducting storage, high capacity supercapacitor storage, as well as battery storage technology.

2) Liaoning Province Announced Plans for the World’s Biggest Chemical Storage Project

Dalian City's reform commission, in order to increase city and province-wide load shifting ability as well as curb curtailed wind energy, submitted plans for a 200 MW/ 800 MWh vanadium flow storage project. Once approved, this marked the first time the NEA has signed-off on a national-level large scale chemical storage project. Total investments for the project are at US$500 million with construction to begin by the end of 2016. The first 100 MW capacity is expected to be installed by the end of 2017 with the the remaining 100 MW coming in by 2018.

3) Energy Storage Conference & Expo 2016 Successfully Completed its 5th Year

On May 11, 2016 CNESA wrapped up the 5th annual Energy Storage Conference & Expo in Beijing. The event brought together policymakers, industry leaders, and technology experts for three days of high-level talks, networking, and collaboration. CNESA also released its 2016 White Paper announcing predictions for China's storage market to reach 24.2 GW by 2020 under ideal conditions, and 14.5 GW with business as usual conditions (all figures excluding pumped hydro storage).

CNESA is pleased to further announce the 6th Annual Energy Storage Conference & Expo is set to take place in Beijing May 22-24, 2017, with plans to release the 2017 White Paper at that time.

4) China's North Opened to Energy Storage

On June 7, 2016 the NEA released “Announcement on Promoting Electrical Storage Participation in Ancillary Service in the ‘Three Norths’ Region” 《关于促进电储能参与“三北”地区电力辅助服务补偿(市场)机制试点工作的通知》 opening up power markets in China's North to energy storage. The announcement states that that up to five projects will be eligible to participate in peak regulating and ancillary services compensation mechanism trials. Payment, similar to United State's FERC Order No. 755 “mileage” payment mechanism, is based on services provided to increase effectiveness of the scheme. This announcement was a milestone in storage related policy, marking the first time storage received recognition to participate in providing grid services.

5) CERS Established Storage Committee, Naming CNESA Secretariat

The China Energy Research Society, a research body formed under the China Association for Science and Technology, founded an Energy Storage Committee in May of 2016 in order to promote academic exchange in the energy storage field, promote innovation, and provide a platform for collaborations and research discoveries. Soon after, the committee named CNESA as secretariat, together aiming to promote the implementation of industry-related policy, encourage exchange, and develop business models. On September 9th, 2016, the Committee convened for the inaugural meeting with attendees representing industry as well as high-level government agencies.

6) Chinese Premier Calls for Storage Technology Breakthroughs

On November 17, 2016, Chinese Premier, Li Keqiang, emphasized the need for technology breakthroughs in energy storage and microgrid technology. In order to meet China's goals to increase adoption of renewable energy resources, Premier Li stressed the need for energy storage. Additionally Premier Li called for increasing China’s global competitiveness in the energy technology sphere, calling for breakthroughs in microgrid technology and the construction of the “Internet+” Smart Energy, promoting grid system adjustability, increasing renewables consumption, and developing state-of the art high-efficiency energy technology. He also voiced the need for reforms in state-run energy enterprises, and increasing support for privately-run energy companies entering the industry.

7) NEA Project Guidelines Include Energy Storage

On November 22, 2016, the NEA published the “National Electricity Project Demonstration Management Guidelines” 《国家电力示范项目管理办法》clarifying the application procedures for demonstration project assessment and approval. Among these guidelines, the document also states that energy storage projects fall under this jurisdiction. The release of the document marks a big step for energy storage, showing official, legal recognition by the National Energy Administration, thereby laying the groundwork for future storage projects, policies, and wide-scale implementation.

8) Battery Companies Massively Invested in Storage Projects

As more and more consumers move to purchase electric vehicles, supply has struggled to meet demand. As such, in 2016 companies like BYD, Lishen, China Aviation Lithium Battery Co., Guoxuan, and Optimum Nano released investment expansion plans. Additionally, lead-battery producers like Mengshine, Shuangdeng, and Narada invested heavily in constructing Li-ion battery production centers. On November 22, the Chinese Ministry of Information and Technology published a draft proposal on electric vehicle industry standards 《汽车动力电池行业规范条件(2017年)》 stipulating future Li-ion factories must have annual production capacities of 200 MWh. The figure, however, was later updated to 8000 MWh, a move which will likely further increase investments.

9) New Specialized Storage Companies Emerged

Several specialized storage companies were founded in 2016 deploying large scale storage production capacity totaling over 100 MWh. New companies largely originated in one of two ways: either 1) battery manufacturers and PCS companies combining with system integrators, or 2) PV manufacturers moving into storage applications. In the first category, examples include Sungrow’s collaboration with Samsung SDI, Clou Electronics with LG Chem, and Eve Battery with Alpha ESS. The second category of PV manufacturers expanding to storage operations includes GCL Technology Integration Co. who recently founded GCL Integrated Storage announcing a 500 MWh annual capacity production center in Suzhou, along with Trina Solar announcing Trina Storage.

10) Electricity System Reforms Continue to Roll Out

Following the 2015 release of Document No. 9 (9号文) additional provincial, city, and regional-level reforms have begun to take shape introducing electricity retail reform pilots. So far, the NDRC has already reviewed plans comprehensive reform trials for 18 provinces and autonomous regions including Yunnan, Guizhou, Shanxi, Guangxi, Hainan, Gansu, Beijing, Hubei, Sichuan, Liaoning, Shaanxi, Anhui, Henan, Xinjiang, Shandong, Ningxia, Shanghai, and Inner Mongolia. The following 8 provinces and regions have also already launched retail reform pilots: Guangdong, Chongqing, Xinjiang Production and Construction Corps, Heilongjiang, Fujian, Hebei, Zhejiang, and Jilin. Additionally over 1,000 new electricity retail companies have been registered across the country.

CNESA Storage Market Analysis Q3 2016

Leading up to Q3 2016, China has accumulated a total of 170.6 MW of operating energy storage, this figure represents a 34% increase compared to the same period last year.

In Q3 of 2016, 14 new projects were announced including projects in the planning stage, projects under construction, and newly operation projects totaling 587.0 MW in scale, representing a 586% increase compared to Q3 of 2015, and a 50% increase compared to Q2 of this year. These new storage systems are part of projects geared at renewable energy grid integration along with distributed electricity generation and microgrids.

Q3 also saw 3 projects beginning operations totaling 1.5 MW in scale, a 50% increase compared to the same period last year, and an 87% increase compared to Q2 of 2015. These projects primarily focus on distributed generation and microgrids.

Bulk of New Projects Concentrated in China's Northwest

Gansu Province:

Guazhou County, Jiuquan City: Shidai Jiahua Co. has announcement plans for a 400 MW*4h super capacitor storage station as part of a wind curtailment microgrid project demonstration. Investments totaling US$860 million with an expected payback of 16-18 years.

Inner Mongolia

Xilin Gol: Plans announced for a 160 MW microgrid and renewable grid integration project demonstration as part of local government plans to explore setting up independent electricity retailers.

Jiangsu Province

Xuzhou Economic Development Zone: A 1.5MW/12MWh project under China Silicon Industries, Narada Power, Sungrow, GCL Power began operations.

Wuxi City Xingzhou Industrial Park: A Narada Power backed 15 MW/120 MWh project, with plans to increase capacity.

Huai’an City: Huai’an Electricity Supply Co., Nanrui Huaisheng Cable Co., Sunwoda jointly collaborated on a 500kW/1000kWh project.

Tibet

Shuanghu County: A new storage project owned by Northwest Engineering Corporation began operations. Storage by Samsung SDI- Sungrow (7 MW/ 13.6 MWh) Clou Electronics (3 MW/10.08 MWh).

Power Reforms Take Shape on a Regional Level

Several rounds of regional-level reforms

| Electricity trading centers established | Guangxi Province Guangdong Province Beijing Hebei Province Kunming Chongqing |

| Reform plans approved by NEA | Fujian Province Beijing (submitted only) Hainan Province Shandong Province |

| Comprehensive reform trials approved by NEA |

Yunnan Province Guizhou Province Shanxi Province Guangxi Province |

| Electricity Retail Reforms approved by NEA |

Guangdong Province Chongqing Xinjiang |

| Power Trading/Power Market under construction |

Chongqing Tianjin Tang Grid Jing-Jin-Ji Grid (regional grid connecting Beijing, Hebei Province, and Tianjin) |

Storage Appears in Q3 Renewables Sector plans

Large scale wind/solar

Xinjiang recently published a policy document “Opinions on Increasing Expansion of Renewables Consumption Sustainable Development” accelerating plans for wind and solar + storage project construction and demonstrations.

Thermal Storage

National Energy Administration issued “Notification on Construction of Solar Thermal Generation Project Demonstrations” confirming 20 new solar thermal pilot projects, totaling 1349 MW. Projects will be distributed across Qinghai Province, Gansu Province, Hebei Province, Inner Mongolia Autonomous Region, and Xinjiang Autonomous Region. Construction on approved projects is required to be completed by the end of 2018.

Q3 Industry News

Production Plans

- Chinese PV/inverter manufacturer now storage manufacturer, Sungrow, has formally began joint operations with Samsung SDI. By the end of this year production capacity will reach 100 MWh, with 500 MWh expected by next year

- GCL Integrators: plans to invest USD13 million in a 500 MWh annual capacity battery manufacturing facility.

Investments

- Gree Electronics: purchased of Zhuhai Yinlong Co. (珠海银隆) for US$1.8 billion

- Shanghai Power: over the next five years will execute the “10,000 Storage Stations” project. The company has annoucned plans to invest US$870 million within the next 3 years to construct 100-200 storage projects in Wuxi, Jiangsu Province. Within the next 5 years Shanghai Power plans to invest a total US$4.3 billion planning over 1000 storage projects in Hubei province.

Electric Vehicles

Planning Documents

Beijing: According to the “Beijing City 13th Five Year Period Plan for Strengthening National Science and Technology Innovation,” by 2020, Beijing will become China’s leading alternate energy vehicle R&D center. The entire city aims to produce 500,000 electric vehicles by 2020.

EV Battery/ EV Manufacturing

Shaanxi Optimum Nano: the first of a three stage electric vehicle battery manufacturing project went into operations in Weinan City, Shannxi Province (10 GW production capacity, total investment US$720 million)

Guoxuan High-Tech & Kang Sheng Co. in Luzhou, Sichuan Province will invest US$430 million to build a 1000MAh production capacity production center.

BYD: in Xining, Qinghai Province invested US$580 million for a 10 GWh Li-ion battery production project. In the next three years, BYD also plans to expand operations to a US-based EV factory operations, increasing production capacity from 300 buses/year to 1000 buses, trucks, and other specialized vehicles.

A Conversation with CNESA's Tina Zhang

Potentials for Energy Storage in China's Ancillary Services

An interview with Tina Zhang, China Energy Research Society Energy Storage Committee Secretary General, China Energy Storage Alliance Secretary General

Interviewed by Qiuling Xu, China Electric Times

Introduction: Solar and wind powered energy are developing at high speed, yet at the same time are faced with a series of challenges regarding energy waste. Through ten years of development, energy storage has already been acknowledged as the crucial technological solution to this problem. The following is an interview with CNESA Secretary General, Tina Zhang, regarding energy storage’s promise in providing ancillary services.

Cost is Key for Energy Storage’s Participation in Load Shifting/Frequency Modulation Services

Xu: In regards to the changing energy landscapes in China where wind and solar resources are quickly being integrated into the grid, what challenges does this pose for China’s ancillary services?

Zhang: Essentially, the problem is like this: the difference in demand between peak- and off-peak electricity is growing and the system’s load shifting capacity can’t keep up. Powering up and powering down large-scale thermal power equipment results is highly inefficient, causes equipment wear and tear, wastes coal, and is neither safe nor economic. Pumped hydro storage capacity is also insufficient. Demand-side management that staggers electricity users to mitigate peak load stress is also not accomplishing enough. In the future, highly efficient, smart grids need large sources of distributed capacity and renewable energy to enter the grid. Additionally, the grid’s ability to accept renewable sources in large part depends on the structure and composition of the electrical power systems, especially the ability to shift peak loads.

Xu: So the industry is following more and more closely the potential value of using energy storage in providing ancillary services?

Zhang: Yes. We will see, adding so much increased capacity in renewables brings about short and long-term problems for the electricity industry. At present, we’re seeing high rates of curtailed wind and solar. In the future, high rates of grid integrated renewables poses challenges for grid regulation. With regard to China’s current main power sources, thermal power is not only the country’s principal electricity generation source, but also undertakes most of current ancillary service operations. Pumped hydro storage and natural gas, by contrast, are used much less. In addition, during winter months, thermal power must also provide heating; you could say that thermal power’s multifaceted role makes it difficult to exhibit its function in providing ancillary services. In light of these two circumstances, this gives storage a certain opportunity. Using energy storage to provide ancillary services will increase grid flexibility, as well as encourage renewables consumption.

Xu: Since resources to provide ancillary services in China are limited, the idea that storage can participate in this market is becoming a hot topic. Starting with the 2011 Zhangbei solar+storage transmission integration project, the performance and effectiveness storage stations providing ancillary services for large scale renewables projects are being validated. However, the fact remains that costs are still an issue. Do you see this as a challenge?

Zhang: It is. Cost is certainly an important factor when considering whether or not storage can be used to provide ancillary services. With regard to mainstream storage technology costs, we’ve discovered that through 2015 to the beginning of 2016 storage investment costs have come down significantly when compared to 2014. Take the lithium iron phosphate battery as an example: system costs have already dropped to USD$300/kWh, which we predict will drop 50% by 2020, reaching as low as USD$150/kWh. By 2020, we also expect other storage technology costs to drop significantly, among them lead batteries to drop 48%, vanadium-flow batteries by 23%, and supercritical compressed air storage to drop by 44%.

You could say, the decreasing costs also will help storage participate in “peak shaving valley filling” applications, further assisting an increase in renewables consumption. Energy storage systems can realize a multitude of applications and bring about economic gains and increase efficiency. Thus whether or not the investment costs of storage are economically feasible depends on if storage stations obtain the rights to participate in ancillary services. This will be the driving force behind realizing the benefits and value of storage and promoting future adoption of energy storage technology.

The Urgent Need for a Feasible Profit Model

Xu: How would you say China has made headway in promoting the use of energy storage to provide ancillary services?

Zhang: In June of this year, China’s National Energy Administration formally released “Notification for the Trial Demonstration Promoting Storage in China’s North Compensation (Market) Mechanism” which for many was a burst of fresh air, blowing open the door to allow storage to participate in ancillary services markets. Everyone in the industry was full of confidence. According to our forecasts, under “business-as-usual” conditions, Chinese storage capacity will reach up to 14.5 GW (these data include thermal storage, but not pumped hydro). In an ideal scenario, we could see capacity reaching up to 24.2 GW. Favorable policy and market requirements are the two forces that would set the foundation to encourage storage applications. At present, projects like Dalian’s national level chemical storage demonstration and the Erlianhaote microgrid network project are either in planning or are actively being deployed. Some new models for storage stations providing ancillary services are also under investigation.

Xu: So these new models you just mentioned, investigations into such models have produced what kind of results?

Zhang: Most recently at the “Seminar on the Role of Large-Scale Storage in New Energy Generation,” industry leaders unanimously agreed, the biggest challenge facing the storage at the moment is lack of a viable profit model. In theory, storage can improve the quality of power generated by wind, alleviate stress on the grid, participate in power electricity markets, and provide ancillary services, all of these applications. But owing to the fact that storage lacks a clear mechanism to participate in these markets, and lacks a method to calculate costs and generate profits, it’s really hard to properly consider storage’s value. In addition, at the present stage, storage is mainly deployed at wind and solar stations, effectively binding storage with wind/solar operations. The grid has no way to optimize the dispatch of storage resources, making storage’s function less than anticipated. We need to separate storage from wind/solar stations to properly calculate its profitability. As a result, all this brings about a lot of difficulty in setting up a payment mechanism.

Xu: And there’s no policy addressing this?

Zhang: The industry is actively working on this. For example, the domestic company, Quanwei, has been suggesting the concept of constructing stand-alone battery storage stations at centralized wind/solar sites. They hope that such a setup would allow the stations to coordinate wind/solar storage in addition to separated, stand-alone storage operations. This kind of stand-alone storage could be directly dispatched by the grid to provide many types of services including ancillary services, backup capacity, and power output smoothing, much similar to small-scale pumped hydro stations. In Quanwei’s stand-alone storage concept, the storage station’s adjustable capacity is relatively easy to calculate, this definitely simplifies many of the problems faced by energy storage station. Separating storage from generation equipment makes things clearer from an investments point of view as well, making it simpler to make economic assessments. At the same time, it makes it easier to illuminate the intrinsic value of storage technology, itself, making storage technology a stronger target for policy and subsidies.

This interview has been translated from the original Chinese, available here.

Nine Updates on China’s 2016 Energy Storage Industry

In the first half of this year we observed some positive signs: China’s increasing electricity system reforms, the rise of the “energy internet,” and growing activity in frequency regulation and peak-load shifting in China’s North. We also saw some less positive developments such as increases in wind and solar curtailments. Good and bad alike, all of these developments underline the importance of energy storage in a wide array of fields, from renewable energy, distributed generation and microgrids, as well as in setting electricity prices. From the beginning of 2016 to present, China’s energy storage industry took steps forward in project planning, policy support, and increasing product capacity.

Here are nine highlights:

1) Large-Scale Storage Projects Increased

According to CNESA’s project database, storage project installations continued to increase. In the first half of 2016, newly operating projects totaled 28.5 MW, principally focused on renewable energy grid integration in Northwestern China. The nine newly operating projects include Golmud (Tibet) City Solar Storage Station and Kelu Electronics Solar Storage in Yumen, Gansu province.

In addition to the projects in operation, in the first half of 2016, China also announced storage project construction plans adding up to over 400 MW in scale (CNESA project database). System integrator companies Samsung SDI-Sungrow, Dalian Rongke, Narada Battery, were the main enterprises involved. Technologies involved include Li-ion, flow, and lead storage batteries. Principal applications include ancillary services, large scale renewable energy grid integration, and distributed energy and microgrids. CNESA forecasts that these projects will gain momentum in the upcoming years.

2) New Energy Policies Emphasized Energy Storage

As China enters its 13th Five Year Planning Period in the midst of the energy revolution, the State Council, National Development and Resource Council (NDRC), and National Energy Administration (NEA) have all geared policy efforts towards adjusting China’s energy systems, innovation of new technology, manufacturing equipment, constructing smart grids, and developing renewable energy. CNESA predicts future policies will be focus on the energy internet, ancillary services, and microgrids, all increasing applications for energy storage technology.

Energy storage was mentioned in numerous policy documents including, “Innovation in the Energy Storage Technology Revolution: New Action Plan (2016-2030),” “Outline for the Strategy of Driving National Innovation,” and “Made in China 2025—Plan for Installation of Power Equipment.” Such policy documents clearly outlined roadmaps for development and innovation in the energy storage, project demonstrations, and how to tackle key problems in the industry.

The importance and application value of energy storage technology also appeared in the policy document “Guiding Opinions on Implementing the ‘Internet+’ Smart Energy Development.” Energy storage is related to internet, electricity storage, heat storage, hydrogen cells, and gas storage. Through different forms of storage, electric power, heat, traffic, and oil and gas applications all interconnect.

3) Power System Reforms Granted More Marketing Opportunities for Energy Storage

New rounds of electricity system reforms aim at transmission & distribution price reforms, the creation of an electricity market, sell-side reforms, and launching demand response. Increasing the degree of electricity marketization will allow the latent market potential of energy storage to open up, expanding storage business models, and bring about a turning point in the industry. As electricity retailers throughout China are established, the reforms will go into effect, introducing a flexible and diverse pricing system, thus creating spaces for the use of user-sited energy storage.

Distributed storage set-ups for industrial users were also a hot topic. At present, companies like BYD, Zhonhen, and GSL System Integration Technology Co. have already began targeting industrial parks for planning large scale distributed energy storage systems. Optimizing differences in peak and off-peak electricity prices is the primary goal, along with balancing PV use levels, participating in demand response, delaying upgrades to electricity system infrastructure, and providing in ancillary services. Given current peak and off-peak price conditions, increasing off-peak consumption and decreasing peak consumption in industrial areas can result in investment returns of five years.

4) Energy Storage Can Play a Chief Role in Providing Ancillary Services in Northern China

In June of 2016, the NEA formally issued a policy in favor of electricity systems peak-load shifting and frequency regulation titled, “Notification on Promoting Energy Storage in China’s Northern Regions Ancillary Services Compensating (Market) Mechanisms Trial Project.” This is the final release of the document after the NEA solicited opinions in May earlier this year.

The first part of this document discusses how to formulate substantive policies supporting the energy storage industry, how to employ energy storage in ancillary services cost sharing mechanisms, and how to demonstrate electricity storage technology’s superiority in peak-load shifting and frequency modulation. First of all, the document states that policy must first clearly give stand-alone energy storage an important position in electricity markets. Energy storage also needs a recognized identity similar to that of ancillary services, generator storage, retailers, and electricity users. Next, policy must encourage energy storage diversification by encouraging investment diversification. Policy should also support both concentrated energy storage in renewable energy generation and distributed energy storage facilities in smaller districts, buildings, industries, as well as user-sited distributed storage facilities. Storage’s use in peak balancing, and fast response, will encourage the recognition of its value. Additionally, the document states policy must promote not only power plants, but also user-sited storage facilities to participate in peak-load shifting ancillary services together with grid companies.

5) Rapid Investments in Battery Companies are Driving Energy Storage

The rising popularity of electric cars is driving domestic demand for batteries to the point where supply doesn't meet demand. In the first half of 2016, companies like BYD, Lishen, and China Aviation Lithium Battery Co., Hefei Guoxuan High-Tech Power Energy Co., and Optimum Nano, drove the domestic battery industry forward introducing several rounds of investment plans. Lead battery manufacturers such as Menshine, Shuangdeng, and Narada Power represent enterprises also vigorously investing in Li-ion battery systems.

According to CNESA’s statistics, in the first half of 2016, domestic enterprises already announced an increase of 120 GWh in newly added production capacity for power Li-ion batteries. If operations begin smoothly, by 2018, the domestic market can potentially be faced with the pressures of a supply exceeds demand scenario. In addition to current applications in electric cars, electric bikes, and the electric tools markets, battery storage will become a key industry for battery manufacturers and focus point in future markets.

6) New, Specialized Energy Storage Companies Entered the Market

From 2015 to the first half of 2016, many new companies specializing in energy storage entered the market, with a combined planned storage capacity exceeding 100 MWh. These new businesses largely aim at developing user storage products, providing energy storage systems solutions services. The newly founded companies comprise two main types:

A) Battery manufacturer and PCS companies launching partnerships with system integrators. Examples include:

a. Sungrow Power and Samsung SDI: The joint venture has already accrued more than $170 million USD in investments In July of 2016 the two officially launched energy storage equipment production. They expect an annual production capability of 2000 MWh in storage equipment.

b. Shenzhen Clou Electronics and LG Chem: The two have set up a new joint venture enterprise, Shenzhen Kele New Energy Technologies Ltd., at a registered cost $3.5 million USD. The planned yearly production capacity is set for over 400 MWh, with assembly lines set to begin operations starting in early 2017

c. EVE Lithium Batteries and Neovoltaic: EVE recently purchased a 12.5% share in Neovoltaic. Neovoltaic mostly focuses on PV storage, energy management services, and internet in the Australian and German markets. This move will help EVE expand its storage user base.

B) Traditional PV enterprises along with PV system integrators opening up storage-focused companies. Examples include:

a. Suzhou GCL Integrated Storage Technology Co.: This company, set up by GCL System Integration Technology, was founded with expected annual production of 500 MWh in battery capacity. At present, they have already developed and are taking orders for their first storage product, the E-KwBe NC-S Series. In the future the company will move toward distributed PV, industrial storage, and grid storage.

b. Trina Energy Storage: Trina Solar established Trina Storage Co. as a system integrator company to provide storage solutions for industrial users as well as public utility grid storage, residential storage, off-grid storage, communications systems, and vehicles.

7) Chinese Companies Target Foreign Residential Storage Markets

In recent years, the distributed residential storage market has developed in countries like Germany, Australia, the U.S., and Japan. Local governments overseas have drawn up storage installation subsidies, tax credits, and other demand response incentive mechanisms in order to expand the storage user base and bring about viable business models.

While companies like Tesla, Sonnenbatterie, and LG Chem, release residential storage products all over the word, Chinese storage technology companies are targeting the Australian and German residential storage markets. Since 2016, Shenzhen Clou Electronics, Neovoltaics, China Aviation Lithium Battery Co., GCL Integrated Storage, Pylontech, and Trina Storage, have all released products for residential PV + storage users with capacities ranging from 2.5 kWh to 7 kWh, mainly employing Li-ion battery technology complete with smart energy management systems solutions. Chinese storage enterprises, with technology and production capacity in Li-ion and lead-acid batteries, are looking to establish business partnerships with PV installers and storage system integrators in the Australian, German, and American residential storage markets.

8) Chinese Regional Governments Have Taken Measures to Support the Growing Domestic Storage Industry

As the storage market grows, local and regional governments have grasped the importance of the emerging energy storage industry. In 2016 the governments of Dalian City, Qinghai Province, and Bijie City have all initiated planning efforts for the storage industry, preparing for industrialization and constructing demonstration centers.

Dalian City (Liaoning Province)

In March of 2016, the Dalian City local government issued a policy document “Dalian City People’s Government Opinions on Advancing the Energy Storage Industry,” declaring the city a research and manufacturing center of vanadium-flow and Li-ion batteries. The policy outlines a supply chain involving local materials preparation and system integration, estimating that both the storage and related industries worth at nearly 50 billion CNY. In April of 2016, the NEA approved Dalian’s National Chemical Storage Peak Load-Shifting Station demonstration project, with a scale of 200 MW/800MWh. This signifies the first time that the NEA has approved a national scale chemical storage demonstration project and ensures enormous benefits for Dalian’s flow battery industry.

Qinghai Province