On August 4, Shandong Tai'an Feicheng 10MW compressed air energy storage power station successfully delivered power at one time, marking the smooth realization of grid connection of the first domestic compressed air energy storage commercial power station. The Feicheng 10 MW compressed air energy storage power station equipment was developed by the Chinese Academy of Sciences. Taking full advantage of the natural advantages of good airtightness and high stability of underground salt caverns in the bordering yard of Feicheng, Tai'an, the air is compressed into the salt cavern cavity when the grid load is low, and the exhaust gas is used to drive the generator to generate electricity when the grid load peaks, so as to realize auxiliary grid reduction. The smooth implementation of the project will play a demonstrative and leading role in enhancing system regulation capabilities, ensuring the safe and stable operation of the power grid, and improving new energy load support capabilities.

China 's First Regional Frequency Regulation Auxiliary Service Market Operates

With the approval of the Southern Regulatory Bureau of the National Energy Administration, the country's first regional ancillary service market with FR services as trading product-the Southern China Regional FR Auxiliary Service Market will be officially put into operation on July 1. Since it started in Guangdong in September 2018, the southern regional FR auxiliary service market has expanded to four provinces: Guangdong, Guangxi, Yunnan, and Hainan. The market has "distributed orders" (frequency regulation mileage instructions) more than 48 million times, and market compensation costs amounted to RMB2.82 billion, allowing more participants to earn the dividends of market-oriented reforms.

Industry insiders have vividly compared the southern regional FR auxiliary service market to an online car-hailing platform. Power dispatch agencies are similar to online car-hailing platform operators, which issue system adjustment requirements (frequency regulation mileage instructions) based on the real-time load, operating conditions, and frequency fluctuations of the power system, similar to the “order dispatching” of online car-hailing platforms; Each power generation unit is similar to a "driver" who grabs orders, and submits an adjustment application to the dispatching agency based on its own adjustment performance and market quotation; after the order is successfully grabbed (confirmed as the winning unit), it is responsible for the system frequency adjustment according to the frequency control instruction issued by the dispatching agency, and receives the order perform the tasks required by the order. "Drivers" who take orders quickly and run orders on time (fast adjustment rate) and good service attitude (accurate adjustment) can often receive more system orders (frequency regulation instructions) and get more "commissions" (compensation benefits for auxiliary services) ).

Through the market-oriented model of “delivering orders”, “grabbing orders”, “acquiring orders” and “settlement”, the four provinces of Guangdong, Guangxi, Yunnan, and Hainan competed in the frequency modulation service market in the southern region. Provide FR auxiliary services to bring substantial market compensation returns to participants. A thermal power plant in Guangdong Province that has been in operation for many years has greatly improved its output performance by installing energy storage devices. By participating in the competition of frequency regulation auxiliary services, the annual service revenue exceeds 30 million yuan, exceeding its power generation revenue.

CATL Released 58.2 billion Yuan for Fixed Increase Plan

On the evening of August 12, CATL issued a series of announcements including the "Preplan for Issuing Shares to Specific Objects". According to the announcement, CATL will determine the number of shares to be issued to specific targets based on the total amount of funds raised divided by the issue price, and at the same time, it will not exceed 10% of the company's total share capital before the issuance, that is, not more than 232,900,780 shares (including the amount), and The number of registrations approved by the China Securities Regulatory Commission shall prevail. The total amount of funds raised from the issuance of shares does not exceed RMB58.2 million (including the amount). After deducting the issuance expenses, it is planned to be used for all projects such as battery production, advanced technology research, development and application, and to supplement working capital.

This fundraising is used to expand the power and energy storage battery production capacity to 137GWh. It is expected that CATL's production capacity is expected to exceed 200/600GWh by the end of 2022, and promote the industry to accelerate into the "TWh" era. The supply chain of related lithium battery equipment and lithium battery materials is expected to benefit. In addition, CATL has increased investment in energy storage capacity and technology. As an industry leader, the company is expected to promote the development of the energy storage industry through innovation, and the progress has exceeded expectations.

National Development and Reform Commission Released Policy on Time-of-use Power Prices: Perfect Peak-valley Electricity Prices and Establish Peak Electricity Prices

On July 29, the NDRC issued the "Notice on Further Improving the Time-of-Use Electricity Price Mechanism", requesting to further improve the peak-valley electricity price mechanism, establish a peak electricity price mechanism, and improve the seasonal electricity price mechanism.

1. Improve the peak-valley price mechanism.

l Scientifically divide peak and valley periods. All localities should consider the local power supply-demand status, system power load characteristics, the proportion of new energy installed capacity, system adjustment capabilities, and other factors. Determine the period of tight system supply with high marginal power supply costs as peak hours, and guide users to save electricity, shift and avert peak hours. Determine the period when the system supply and demand are loose and the marginal power supply cost is low as the valley period to promote the consumption of new energy and guide users to adjust the load. Where the proportion of installed renewable energy power generation capacity is high, full consideration should be given to the fluctuation of new energy power generation output and the changing characteristics of the net load curve.

l Reasonably determine the peak-valley price. All localities should consider the local power system peak-valley ratio, the proportion of new energy installed capacity, system adjustment capacity, and other factors, and reasonably determine the peak-valley price gap. When the peak-valley ratio is expected to exceed 40% in the previous year or the current year, in principle, the electricity price difference should not be less than 4:1; and it should not be less than 3:1 in other places.

2. Establish a peak electricity price mechanism.

l All localities should implement a peak electricity price mechanism based on actual peak and valley electricity prices conditions. The peak period should be reasonably determined according to when the highest load of the local power system is 95% or more of the electricity load in the previous two years and should be flexibly adjusted in consideration of the power supply and demand of the year, weather changes, and other factors; the peak power price rises on the basis of the peak power price in principle not less than 20%. Where cogeneration units and renewable energy have a large proportion of installed capacity, and where the contradiction between phased oversupply and demand in the power system is prominent, a deep valley electricity price mechanism can be established concerning the peak electricity price mechanism. Strengthen the coordination of peak-valley electricity price mechanism and power management policies, and fully tap the demand side adjustment capabilities.

3. Improve the seasonal electricity price mechanism.

l Where there are obvious seasonal differences in daily power load or power supply and demand, it is necessary to further establish and improve the seasonal power price mechanism, divide the peak and valley periods by seasons, and set the seasonal peak and valley price difference reasonably; where the proportion of renewable energy such as hydropower is significant. It is necessary to comprehensively consider the complementary factors of wind and water, and further establish and improve the high and low electricity price mechanism. The high and low periods should be reasonably divided according to the characteristics of water and wind and solar output over the years, and the floating rate of electricity price should be set reasonably according to the supply and demand of the system. Encourage the northern regions to study and formulate seasonal electricity heating price policies, and promote the further reduction of clean heating electricity costs by appropriately extending the trough period and reducing the valley section of the electricity price, and effectively guaranteeing residents' demand for clean heating in winter.

Policy interpretation: Guidance comprehensively promote the development of energy storage under the ‘dual carbon’ goal

Driven by the national strategic goals of carbon peaking and carbon neutrality, energy storage, as an important technology and basic equipment supporting the new power systems, has become an inevitable trend for its large-scale development. Since April 21, 2021, the National Development and Reform Commission and the National Energy Administration have issued the ‘Guidance on Accelerating the Development of New Energy Storage (Draft for Solicitation of Comments)’(referred to as the ‘Guidance’), which has given rise to the energy storage industry and even the energy industry. The industry has given a high degree of recognition to the release of the Guidance and positive feedback. On July 23, the National Development and Reform Commission and the National Energy Administration formally issued the "Guidance" after fully soliciting suggestions from all walks of life.

China Energy Storage Alliance (CNESA) combines the research and understanding of industries and policies to briefly interpret and analyze the content of the guidelines, policies and industrial impacts:

Comparison of the ‘Guidance’ draft and official documents

Compared with the draft, the official document has not changed much, emphasizing strict adherence to the bottom line of energy storage safety, and integrating the advantages of the upstream and downstream of the industry chain through the method of "revealing the list and taking command" to promote the integrated development of industry, university, research and application, and concentrate efforts to tackle key problems in the large-scale development of the industry, promoting the diversified development of energy storage, and ensuring that energy storage becomes a strong support for the realization of the ‘dual carbon’ goal. In addition, in the improvement of the ‘new energy + energy storage’ project , adding a ‘sharing model’ has become one of the ways to implement new energy power generation projects for new energy storage, and it is clear that the ‘sharing model’ is to optimize the coordinated development of regional renewable energy and energy storage , also it is an effective way to promote the formation of a variety of energy storage business models.

The practical significance of the ‘Guidance’ to the development of the energy storage industry

1. Clarify the goal of 30GW of energy storage, and boost to achieve leapfrog development

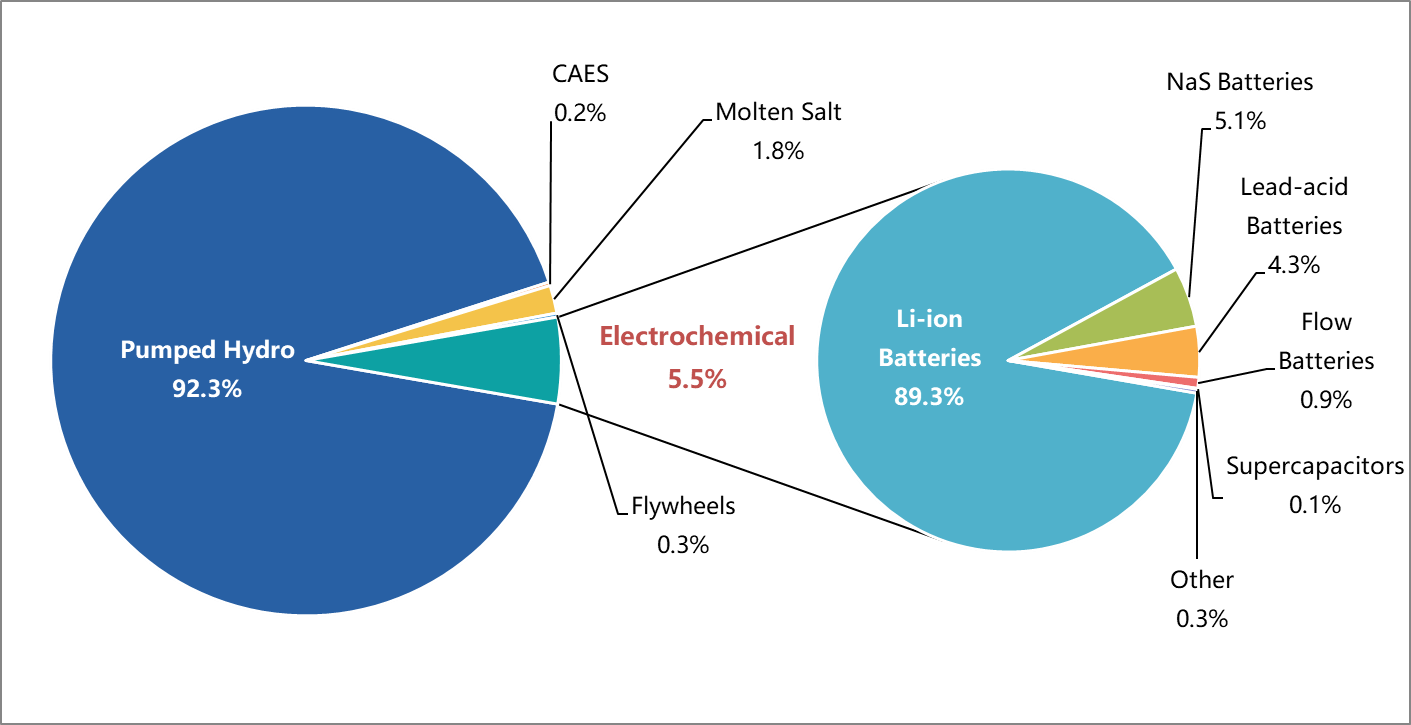

According to the statistics of the database from China Energy Storage Alliance , the cumulative installed capacity of new electric energy storage (including electrochemical energy storage, compressed air, flywheel, super capacitor, etc.) that has been put into operation by the end of 2020 has reached 3.28GW, from 3.28GW at the end of 2020 to With 30GW in 2025, the scale of the new energy storage market will expand to 10 times the current level in the next five years, with an average annual compound growth rate of more than 55%. This total scale and growth rate, and the clarification of my country's new energy storage installed capacity targets will release positive policy signals for society and capital, guide social capital to flow into technology and industries, and boost the rapid arrival of the trillion-dollar energy storage market.

2. Emphasize planning guidance and deepen the layout of energy storage in various application fields

At present, energy storage has entered a stage of rapid development, and it is urgent for the country to coordinate all parties to issue a special plan for it. Through strengthening management and guidance, it can effectively standardize industry management, optimize industrial layout, improve the efficiency of energy storage systems, and avoid disorderly development of the industry.

In the ‘Guidance on New Energy Storage’, energy storage on the power side emphasizes the layout of system-friendly new energy power station projects, the planning and construction of large-scale clean energy bases for cross-regional transmission, and the exploration and utilization of existing plant sites and transmission and transformation facilities for decommissioned thermal power units, or wind and solar storage facilities. These tasks on the one hand meet the current demand for energy storage in the development of renewable energy, and at the same time, they are in line with the previously issued ‘Guidance on Promoting the Integration of Power Sources the Development of Multi-energy Complementarity’ and ‘Notice: Regarding the Development of Wind Power and Photovoltaic Power Generation in 2021’ . It can be said that the implementation is supported and the policies are guaranteed.

Grid side energy storage emphasizes the role of new energy storage on the flexible adjustment capability and safety and stability of the grid, improving the power supply capacity of the grid, emphasizing the emergency power supply guarantee capability of the grid, and delaying the demand for energy storage in the upgrading and transformation of power transmission and transformation. It can be said that the grid-side energy storage that has been suspended since 2019 has re-pressed the start button. At the same time, with the industry’s new understanding of grid-side energy storage and the entry of various social entities, we believe that under the guidance of policies, the grid-side energy storage Energy storage will be rejuvenated.

User side energy storage has always been the most viable application field of the energy storage industry. With the development of new infrastructure and new business formats, user-side energy storage has increasingly shown a development trend of ‘energy storage’ +. With the continuous development of the electricity market deepening, this field will be the main force in energy storage business model innovation, which will bring vitality and surprises to the development of the industry.

3. Improve the new energy storage price mechanism and promote the establishment of energy storage business models

In the "Guidance", for the first time, the establishment of a grid-side independent energy storage power station capacity price mechanism was proposed, and the study and exploration of the cost and benefit of grid alternative energy storage facilities into the recovery of transmission and distribution prices, improved the peak and valley price policy, and created greater development for the user-side energy storage space. Based on the ‘Opinions on Further Improving the Price Formation Mechanism for Pumped Storage’ and the ‘Plan on Deepening the Reform of the Price Mechanism during the 14th Five-Year’ period, the country clearly proposes the establishment of a new type of energy storage price mechanism and a new type of storage price mechanism. Energy should be formed in the form of market competition, and energy storage facilities that play the role of grid substitution will be recovered through transmission and distribution prices. New energy storage can participate in the medium and long-term, spot and ancillary service markets to obtain benefits.

4. Aiming at the points of new allocation for energy storage, and specifying the focus of subsequent policies

At present, more than 20 provinces and cities in China have issued policies for the deployment of new energy storage. After energy storage is configured, how to dispatch and operate energy storage, how to participate in the market, and how to channel costs have become the primary issues which plague new energy companies and investors. In response to the current issues in the allocation of energy storage in various provinces, the document also further clarifies the coordinated development of energy storage and new energy, through competitive configuration, project approval (filing), grid connection timing, system scheduling and operation arrangements, and ensuring utilization hours , power auxiliary service compensation and assessment, etc. are given appropriate inclination, which points out the direction for the rationalization of new energy allocation of energy storage to achieve rational cost relief. In the transitional stage of the power market reform, it is possible to further explore the feasibility of allocation of energy storage in increasing the weight of ‘green power transactions’.

Based on the above analysis, as the first comprehensive policy document for the energy storage industry during the ‘14th Five-Year Plan’ period, the ‘Guidance’ provided reassurance for the development of the industry. In the context of the ‘dual-carbon’ goal and energy transition, the energy storage industry’s leapfrog development is the general trend and demand. The follow-up actions will inevitably introduce a series of policies for the development of energy storage to eliminate industrial development. Faced with ‘obstacles’ one by one. At the local level, with the improvement of policies and market mechanisms, new business models will emerge. We firmly believe that China will become the world’s largest energy storage market. On this huge and diverse fertile soil, the energy storage technology from China will be fully developed and verified, and will lead the development of the global energy storage industry! After all the exploration and perseverance, China's energy storage industry will surely gain steam!

2020 Energy Storage Industry Summary: A New Stage in Large-scale Development

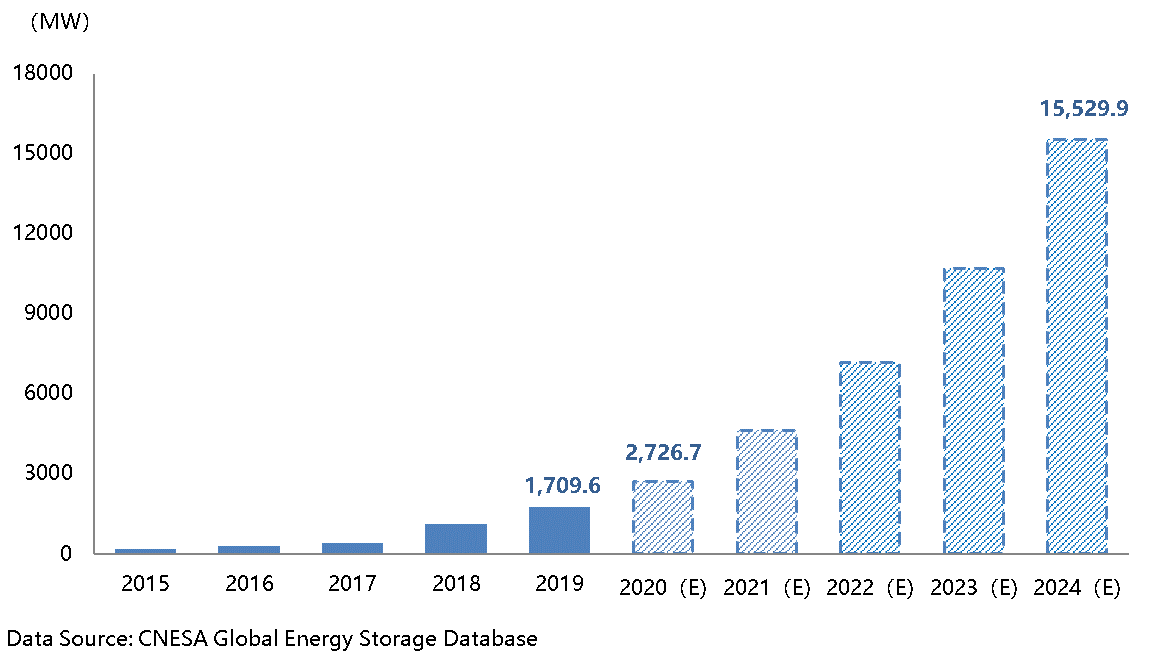

Despite the effect of COVID-19 on the energy storage industry in 2020, internal industry drivers, external policies, carbon neutralization goals, and other positive factors helped maintain rapid, large-scale energy storage growth during the past year. According to statistics from the CNESA global energy storage project database, by the end of 2020, total installed energy storage project capacity in China (including physical energy storage, electrochemical energy storage, and molten salt heat storage projects) reached 33.4 GW, with 2.7GW of this comprising newly operational capacity. Newly operational electrochemical energy storage capacity also surpassed the GW level, totaling 1083.3MW/2706.1MWh (final statistics to be released in CNESA’s Energy Storage Industry White Paper 2021 in April 2021). In 2020, the year-on-year growth rate of energy storage projects was 136%, and electrochemical energy storage system costs reached a new milestone of 1500 RMB/kWh. Just as planned in the Guiding Opinions on Promoting Energy Storage Technology and Industry Development, energy storage has now stepped out of the stage of early commercialization and entered a new stage of large-scale development.

Energy storage first passed through a technical verification phase during the 12th Five-year Plan period, followed by a second phase of project demonstrations and promotion during the 13th Five-year Plan period. These phases have laid a solid foundation for the development of technologies and applications for large-scale development. In response to carbon neutralization goals, initial development plans for the energy storage industry have been set, while the strategic position of energy storage in the reformation of China’s energy structure will be further clarified during the 14th Five-year Plan period. The national government is also currently coordinating the development needs for a variety of application fields. We look forward to seeing national and local step-by-step approaches to resolving the development bottlenecks that have plagued the energy storage industry, and the creation of refined implementation plans which will help transform energy storage into a new sector for economic growth. During the 14th Five-year Plan period, energy storage technology will see further breakthroughs in performance improvement and cost reduction. With the establishment and improvement of policies and market mechanisms, the industry will achieve rapid growth, and China will have the potential to become the largest market for energy storage in the world.

Throughout 2020, energy storage industry development in China displayed five major characteristics:

1. New Integration Trends Appeared

The integration of renewable energy with energy storage became a general trend in 2020. With increased renewable energy generation creating pressure on the power grid, local governments and power grid enterprises in 20 provinces put forward “centralized renewable energy + energy storage” development incentive policies. The policies signify that a consensus has been reached on the importance of energy storage technology to the large-scale application of renewable energy. In order for this development to continue, it will be important to create a rational plan for the deployment of energy storage, ensure the quality of project applications, and to rely on market mechanisms to determine costs and compensation. Profitability is the key to sustainable development.

"Unified" energy projects saw large-scale demonstration and promotion. The “Guiding Opinions on ‘Unified’ Energy Projects” issued by the National Development and Reform Commission and the National Energy Administration states a goal of increasing energy storage at the power side and load side to achieve a flexible and robust grid system. Since the release of the policy, numerous state-owned enterprises and provincial/municipal governments have signed "unified" demonstration project agreements. The planning and implementation of these projects will help to explore development paths and business models for energy storage under diverse scenarios and local conditions.

The value of energy storage in “cross-domain” applications has gradually emerged. The role of energy storage in the safe and stable operation of the power system is becoming increasingly prominent. Energy storage has also begun to see new applications including generation-side black start services and emergency reserve capacity for critical power users. As the construction of new infrastructure such as 5G cell towers, data centers, and EV charging stations accelerates, many regions have used price policies and financial support policies to support the construction of "integrated energy stations", which has helped to extend the “cross-domain” applications of behind-the-meter energy storage.

2. New Rules Gradually Removed Obstacles for Energy Storage to Participate in the Market

In 2020, regional electricity market rules helped establish energy storage’s identity in the ancillary services market, swept away initial obstacles to participation in market transactions, defined basic requirements for third-parties and consumer-side resources to participate in ancillary services, and defined the basic conditions for ancillary services costs to be gradually transmitted to the power consumer. At the same time, under the existing cost-sharing mechanism, energy storage entering the market has also brought risks to the use of ancillary services funds, and local policies have been explored to combat these challenges. For example, market rules and compensation standards have been frequently adjusted in Guangdong, western Inner Mongolia, Qinghai, Shanxi, Hunan and other regional markets. As a result, it is necessary to reasonably plan how projects enter the market while ensuring energy storage can also compete fairly within the market. With the large-scale penetration of renewable energy in the grid, the idea of determining peak and off-peak electricity prices according to net load has become popular. Continued regional adjustments to the price difference between peak and off-peak power have improved the economy of behind-the-meter energy storage, and the charging and discharging strategy of energy storage projects continues to be adjusted accordingly.

3. New Models Have Appeared, Led by "Sharing" and "Leasing"

In the past, energy storage projects widely relied on an energy management contract model. In recent years, with the introduction of relevant supporting policies and greater penetration of specialized energy storage applications, new models have begun to emerge. One such model is the shared energy storage model first launched by Qinghai Province, which has helped to increase the implementation of independent energy storage stations. Another such model is the leasing model for front-of-the-meter energy storage projects adopted by Hunan province in 2018, and the subsequent 2020 upgraded version of the leasing model which applied to energy storage paired with renewable generation and designed to split investment risks between each entity. An additional agent operator model has also emerged. This model allows third-party companies to integrate distributed energy storage systems and EV charging stations through a centralized control station to participate in grid services. The agent operator model is in part a product of the pursuit of value stacking of energy storage applications, and at the same time opens the links between power supply, power grid, and the consumer to realize the value of connecting energy storage. The continued exploration and implementation of new models will greatly promote the value of energy storage applications and the profitability of energy storage projects.

4. Continued Breakthroughs in Technology and Continued Decline in Costs

Breakthroughs have been made in a variety of energy storage technologies. Lithium-ion battery development trends continued toward greater capacities and longer lifespans. CATL developed new LiFePO batteries which offer ultra long life capabilities, while BYD launched "blade" batteries to further improve battery cell capacities. Other energy storage technologies such as vanadium flow batteries and compressed air energy storage saw new breakthroughs in long-term energy storage capabilities. These include the vanadium flow battery stack developed by the Dalian Institute of Chemical Physics, which adopts a weldable porous ion-conductive membrane, and the successfully completed integration test of the first 100MW CAES expander by the Chinese Academy of Sciences Institute of Engineering Thermophysics. Industry attention was also devoted to the effectiveness of applications and the safety of energy storage systems, and lithium-ion battery energy storage systems saw new developments toward higher voltages.

Energy storage system costs continued to decline. Take lithium-ion battery energy storage systems as an example: as battery production scales and manufacturing processes continue to improve and energy storage systems become more highly integrated, system costs have fallen by about 75% since 2012, nearing ever closer to solar/wind parity. By 2020, the costs of energy storage systems fell to 1500 RMB/KWh, bringing storage systems closer to economic feasibility.

5. New Forces Emerged, and Market Players Increase their Efforts to Participate

First, the capital market continued to increase investment in the energy storage industry. Many financial institutions invested in energy storage companies. Examples include Hillhouse Capital's 10.6 billion RMB investment in CATL, and the launch of IPOs by numerous energy storage companies such as Pylontech and Tianneng to raise funds to expand business. Second, new forces have sprung up, accelerating the deployment of energy storage. Traditional energy storage technology and system integrators such as CATL, Sungrow, BYD, and Narada continued to increase investments in the energy storage, while Tianjin Lishen signed an equity transfer agreement with Chengtong. At the same time, new forces in the domestic energy storage market continued to emerge, including Huawei, Envision, and Mingyang Smart Energy. In addition, solar PV companies such as Longi, Tongwei, and TrinaSolar began focus more attention on energy storage. Third, energy storage companies saw deeper integration with other industries. For example, CATL invested in a power engineering design service company, and established cooperation with the State Grid Integrated Energy Services Company. BYD partnered with Canadian Solar, Goldwind, China Resources, Chint and other domestic and international energy developers to expand the international reach of their energy storage business. The past year also saw many mineral, energy, and power companies exploring new opportunities in energy storage.

2020 was the final year of China's 13th Five-year Plan. Over the past five years, a solid foundation has been laid for energy storage in both technologies and applications. The 14th Five-year Plan is an important new window for the development of the energy storage industry, in which energy storage will become a key supporting technology for renewable energy and China’s goals of peak carbon by 2030 and carbon neutralization by 2060. As we face this new period, the question remains as to how energy storage colleagues will seize new opportunities, face changing markets, promote commercial development of energy storage, and establish a leading position in the international market.

Author: Shi Yubo Executive Vice Chairman, China Energy Research Society; Former Deputy Director, National Energy Administration

0.1 RMB per kWh: Qinghai Enacts First Renewable Energy & Energy Storage Subsidy

Recently, the Qinghai provincial Development and Reform Commission, Department of Science and Technology, Department of Industry and Information Technology, and Energy Administration jointly issued the "Notice on the Distribution of Several Measures to Support the Development of the Energy Storage Industry (Trial)" (hereinafter referred to as the "Notice"). For “renewables + energy storage” and "hydropower + renewables + energy storage" projects which produce and store electricity sold to the provincial grid, an operating subsidy of 0.10 RMB per kilowatt hour will be provided. In addition, Qinghai’s Industry and Information Technology Department has announced that for projects with 60% or more of their batteries manufactured in Qinghai, an additional 0.05 RMB per kilowatt hour subsidy will be provided.

According to reports, the "Notice" subsidies will be available for electrochemical energy storage projects developed in 2021 and 2022, and will be settled monthly by the grid company according to the amount of electricity provided. The subsidy funds will be considered a part of the Qinghai grid’s second supervision cycle T&D price reduction reserve funds. The subsidy period is tentatively set from January 1, 2021 to December 31, 2022.

According to an expert at Kaiyuan Securities, Qinghai has always been a leading region for domestic energy storage pilot projects. The introduction of the new energy storage subsidy policy will provide valuable learning experience for other provinces who are likely to follow suit.

Alleviating the Challenge of High Cost Renewables+Storage

Since 2020, the national government has repeatedly expressed support for the development of energy storage, and many provincial governments have issued supporting documents for energy storage at the power generation side. Inner Mongolia, Xinjiang, Liaoning, Hubei, Jiangxi, Shandong, and other regions have recommended or encouraged newly constructed wind and solar projects to deploy energy storage systems. Yet industry disputes over renewables and energy storage have caused continuous challenges. One focus of controversy is who should bear the cost for energy storage. In the absence of both subsidies and a reasonable profit model, can renewables+ storage continue to develop? The Qinghai energy storage subsidy policy will provide some alleviation to the cost challenge of deploying storage with renewables.

Li Zhen, deputy secretary-general of the China Energy Storage Alliance, believes that the release of Qinghai’s energy storage subsidy policy is good for the industry. The policy makes clear that energy storage is prioritized to ensure a certain number of consumption hours, and provides clear standards for subsidy implementation. At the current transition stage in which a mature spot market has yet to be established, the subsidy policy provides reasonable compensation for energy storage services, provides an innovative mechanism for the co-development of energy storage and renewable energy, and provides a model which may inspire related policies in other regions of the country.

Huang Bibin, director of the State Grid Energy Research Institute's New Energy and Statistics Institute, stated that an increasing number of provinces are considering the system regulation challenges of connecting large-scale renewable energy to the grid, and have begun to require renewable energy projects to be equipped with energy storage in order to meet grid-connection requirements and improve the regulation capability of the entire power system. This may become a trend or transition method under the current power market conditions, in which much remains to be improved. Although these deployments have increased the cost of renewable energy for investors, they have also supported energy storage industry development.

Peng Peng, secretary general of the China New Energy Power Investment and Financing Alliance, told reporters that in the past, provincial policies requiring energy storage allocation with renewable generation did not provide any subsidies for energy storage, and that Qinghai’s policy is the first to do so. This is a big step forward for the industry.

However, one anonymous expert from the Energy Research Institute at the National Development and Reform Commission believes that the subsidy policy issued by Qinghai can only partially solve the problem of excessive energy storage allocation costs, and cannot completely resolve all disputes over renewable energy and energy storage allocation. Additional points of contention when pairing renewable energy and energy storage include the proportion of energy storage capacity which should be required for each system, and the manner in which energy storage should be deployed.

Lack of Assessment Standards for Energy Storage Systems

According to data from the National Energy Administration, during the first three quarters of 2020, Qinghai’s solar curtailment was 940 million kWh, a rate of 7.0%, and a year-on-year increase of 1.2%. The rise of the curtailment rate makes the need for energy storage increasingly urgent. The release of Qinghai’s new subsidy policy will help to increase industry willingness to deploy energy storage.

While the current version of the policy makes clear provisions on subsidies, it does not put forward specific indicator requirements for the energy storage system. Li Zhen told reporters that energy storage is an emerging technology, and related standards are gradually being established. At present, standards have been released for the construction, grid connection, and testing of energy storage stations. Regions may set corresponding entry thresholds in accordance with national standards to ensure the construction quality of the energy storage system. In addition, because Qinghai’s policy will subsidize energy storage based on the amount of electricity generated rather than subsidizing initial investment, there is decreased risk of fraud related to deployment of substandard or inadequate energy storage systems.

According to Li Zhen, "If we calculate according to the requirements of the “Notice,” which ensures that energy storage facilities are utilized for no less than 540 hours, then an energy storage system discharging for 2 hours a day will see utilization of 270 days or more. As the ancillary services market and spot market develop and improve, energy storage may participate in primary and secondary frequency regulation. With a certain amount of profits guaranteed, energy storage application scenarios will become more varied, and investment recovery and project profitability will become more feasible. As long as there are reasonable market applications, we can avoid the possibility of bad market entities driving out good ones, and more investment will be driven into the market to build more high-quality energy storage projects."

Peng Peng believes that market maturity cannot happen overnight. In the early stages in which data is lacking and experience is limited, only a simple management model can be used for an initial batch of projects, followed by a gradual refining of management. Therefore, for the time being, there are only subsidies, without standards and management regulations. Although some companies may adopt lower-priced energy storage equipment out of cost considerations, the possibility of compensation being awarded to substandard projects is unlikely under the current diversified regulatory methods.

Huang Bibin stated that as a "Notice", it is not necessary to clarify all contents. In the future, as more projects are advances, policies on construction quality or grid-connected standards may be issued, as well as detailed implementation rules for subsidies.

Policy Implementation Requires Refinement

As the first domestic subsidy policy addressing energy storage and renewable generation pairing, many difficulties may still arise in the specific implementation process.

One industry expert interviewed agrees that to receive the subsidy, electricity sold to the grid must be electricity that is within the province. But determining what electricity is considered “provincial” is a problem. As the anonymous expert stated, “Is it possible to consider all power which is not transmitted by UHV lines as part of ‘provincial’ power? The policy requires further refinement in order to answer this question."

In addition, according to the "Notice", power dispatched by electrochemical technologies in “renewables+storage” and “hydropower+storage” projects will no longer participate in Qinghai's annual direct power trading market, but will instead have payment settled through Qinghai’s renewable energy settlement base price. According to the anonymous expert above, "It is not explained how the base price is determined. I personally assume that it will be the average settlement price for renewable energy. However, whether this average price will be based on "wind+solar," "wind+solar+hydropower," or just simply ‘solar’ still needs to be clarified. "

Energy storage is still in the early stages of development. The main factor restricting the deployment of energy storage paired with renewable generation is that the cost of energy storage is not transmitted through a reasonable market mechanism, and that the full benefits of energy storage cannot be fully realized under the current structure. Although the "Notice" provides clear utilization hours and subsidy criteria for energy storage, Li Zhen believes that subsequent implementation rules are needed to ensure successful policies and guarantee the benefits of energy storage. For example, how should energy storage utilization hours be measured? How should the income which energy storage generates be settled?

"In addition, Qinghai is the first province to construct independent energy storage stations which participate in peak shaving. This new policy does not specify charging and discharging prices for these independent energy storage stations, nor does it specify their transaction settlement mechanism. These issues need to be further refined." Li Zhen said. "Finally, over time, we also need to determine how many flexible regulation resources Qinghai needs, and how many energy storage stations need to be deployed. We also must work to further understand and create a plan for how the power grid can ensure that energy storage utilization reaches 540 hours. The clearer the policy, the more beneficial it will be to stabilize investment and create a good business environment."

Author: Han Yifei, China Energy News

Energy Storage and Renewable Energy Co-development Trends and Application Models

In recent years, as installed capacities have expanded and technologies have advanced, the cost of renewable energy power generation has dropped significantly, gradually approaching that of fossil energy and in some cases even lower than that of fossil energy. The pairing of “renewable energy + energy storage” has gradually become the consensus for future renewable energy development.

In the past two years, many provinces, cities, and regions in China have issued ancillary services construction plans and operations regulations, such as updates to the grid regulations in northwest China, updates to grid regulations and ancillary services market regulations in northeast China, regulations for energy storage engaged in peak shaving in Shanxi, rules for third-party independent participation in the north China peak shaving ancillary services trial market, updates to grid regulations in southern China, and other regulatory updates. These rules have helped to promote the healthy and orderly development of the power ancillary service market, and have provided a platform for new market players and new technologies such as energy storage to participate in the power market. For example, Zhejiang has carried out transactions for ancillary services such as frequency regulation, voltage regulation, backup, and black start, explored a joint clearing model for ancillary services and the spot market, and optimized the marginal clearing of electricity and ancillary services.

In addition, over the past two years, more than ten provinces including Inner Mongolia, Hubei, and Henan have issued policies requiring new renewable energy projects to be equipped with 5%-20% energy storage systems to promote renewable energy + energy storage applications.

Renewable Energy + Energy Storage Application Business Models

Centralized wind/solar stations + storage application models typically engage in services such as peak shaving, capacity firming, grid support, and output smoothing. Current profit points include load shifting during limited power periods, priority dispatching, and reduction of thermal power spinning reserves. Potential profit points include revenue from solar-storage and wind-storage and from participation in frequency regulation and ancillary services. The advantages of these application models are that they can limit the risk of generators being penalized. However, the true value of lowering such risks is difficult to assess, and there is no compensation mechanism to measure the value created by energy storage. Economical projects are also difficult to guarantee. Additional challenges include a lack of rational investment undertaken by the power generation side, a lack of supporting policies, a lack of a market mechanism, and a lack of large-scale energy storage planning.

Xinjiang is one example. On May 26, 2020, the Xinjiang Development and Reform Commission issued the "Interim Regulations for Generation-side Energy Storage Management in the Xinjiang Power Grid," encouraging power generation companies, power sales companies, power consumers, and independent ancillary services providers to invest in the construction of energy storage facilities with a required charging power of 5000kw or more and continuous charging time of 2 hours or more. The interim regulations provide four basic principles or application models, namely, market bidding, inter-plant transactions, bilateral negotiations, and grid dispatch. Of these, the main operations rules which are used include market bidding by wind farms/solar PV as well as bilateral negotiations between power generation companies and energy storage. The regulations help to encourage the power grid to increase basic dispatching time by 100 hours annually.

These wind-storage and solar-storage stations enjoy two kinds of profit models. The first is the self-use of energy storage capacity at the wind or solar station where it is located, dispatching energy as if it were generated by the plant, and generating revenue according to the generator’s contracted price. The other type of profit model is generated when the energy storage facility enters a charging state according to the instruction of the power dispatch agency, and receiving compensation for the amount of power charged. Standard compensation for this model is 0.55 yuan/kWh.

In addition to the front-of-meter energy storage in Xinjiang, the industry has also taken note of the “shared energy storage” commercial operations model in Qinghai. This model allows renewable energy plants and energy storage enterprises to sign a transaction contract specifying time, quantity, and price of energy being traded, and cooperating with the power grid to allow dispatch of energy storage.

Rather than limiting energy storage applications to the generators at which they are co-located, a more flexible business model can be created which forms independent energy storage system operators. These specialized companies would engage in the selection, financing, design, construction, operation, and maintenance of energy storage power stations. In actual operation, energy storage operators would need to cooperate with power generation enterprises to form "virtual" connections, that is, energy storage systems would not need to be physically connected with generators, but could form a unified body of power generation enterprises at the grid-side so that generators and energy storage systems can provide high quality ancillary services. A win-win for energy storage operators and power generation enterprises can be achieved by sharing the compensation received for providing ancillary services.

Three models can be derived from this: In the first, a single power generation company and a single energy storage operator cooperate with a clear relationship and direct cost settlement. In the second model, one power generation company cooperates with multiple energy storage operators. In this model, power generation companies can make full use of the advantages of energy storage technology, and even use the variety of energy storage resources at their disposal to meet the demands of different ancillary services, thereby maximizing the quality of ancillary services provided. However, this type of cooperation model is technically more complicated, creating challenges for the operation and management of power generation. In the third model, multiple power generation companies cooperate with one energy storage operation company. The foundation of this business model is that the energy storage operator has built a larger capacity and module-divided energy storage station, and the energy storage operator may choose its best quality partner. However, this type of model presents a certain degree of complexity in business operations.

New Energy Storage Policies and Trends in China

Energy storage development in China is seeing new trends emerge.

First, energy storage technology is a multi-disciplinary, multi-scale integration of science and technology. Chemical and physical energy storage technologies involve electric power, machinery, control and other aspects. Energy storage materials, units, systems and other components require multi-disciplinary cross-integration. This cross-integration will become a major trend as new technologies are developed and existing technologies improve.

Second, there are currently a variety of energy storage technologies, which may become centralized on a handful of mainstream technologies in the future. At the same time, new technologies will continue to emerge. Whichever energy storage technology will dominate the market will be a matter of the market “voting with its feet.”

Third, the price of energy storage is rapidly falling. Only under the precondition that both renewable energy and energy storage prices continue to fall can renewable energy + energy storage become an established business model.

In the future, energy storage and renewable energy will see integrated development. Renewable energy development in China will pass through three stages, namely, the subsidy support stage, the renewable energy parity stage, and the renewables + storage parity stage. Only when the renewables + storage price (parity) and performance (dispatchability) become comparable to fossil energy will the era of mainstream renewable energy truly arrive.

Energy storage itself will also pass through four stages of development: a technical verification stage, an applications demonstration stage, an initial commercialization stage, and a large-scale development stage. Energy storage in China still faces some major challenges, such as safety concerns, a lack of clarity on what entity should be responsible for energy storage management, a lack of a reasonable price mechanism that can properly compensate storage’s value, an incomplete support mechanism for participating in the energy market, and other challenges.

To meet these challenges, we must first clarify what entity will be responsible for ensuring the safety of energy storage systems, and what entity will be responsible for overall management of energy storage projects. Comprehensive safety evaluations of energy storage systems should be conducted, identifying safety hazards at each segment of the energy storage system, and determining proper management methods for minimizing such hazards. In addition, we must also make use of project experience and our knowledge of current market development to improve standards and regulations for energy storage, and raise the threshold of entry for energy storage products in the market.

Second, we must clarify the identity of energy storage as a market entity. This includes defining the procedures for establishing energy storage projects, including fire safety approval, environmental assessment, land approval, facility approval, civil air defense approval, and other procedures. Grid companies must also clarify the procedures for grid connection of energy storage across various storage applications.

Third, a reasonable price mechanism must be defined. The value of the public good brought by energy storage is far greater than its cost. But if only a single market entity is responsible for the cost of energy storage, benefits are likely to be less than the total cost of investment. Therefore, we must look at the cost and value of energy storage from an overall perspective, making decisions at the national level and based on the principle that the beneficiary should be the one to pay for services. These actions will help to establish a reasonable market-oriented price mechanism shared by generators, the grid, and consumers.

Facing the challenged of energy storage commercialization across many fields, we must continue to accelerate the power marketization process, use market-based means to solve challenges in energy storage system applications, and rationalize market rules to adapt to new technologies such as energy storage. The ancillary services market and demand-side management, particularly the long-term demand response mechanism, are still waiting to be fully established in order to increase the value of energy storage applications across various fields. In the initial stages of marketization, it is also necessary to provide financial assistance to energy storage to support the social benefit it brings. We have three primary suggestions for the development of energy storage:

At the current stage, we must be engaged in forward-thinking planning and research to avoid ineffective allocation of resources. We must make clear the threshold of entry for energy storage in the market to ensure only high-quality energy storage applications are developed. We must also implement policies for paired energy storage applications which will support co-development of storage with renewable energy generation.

In the short term, with the power market and price mechanism still unable to reflect the value of paired energy storage systems, we must promote pumped hydro storage polices and introduce transitional polices which will support renewable energy and energy storage co-development. We suggest that an energy storage quota mechanism should be explored, and the importance of “green power” should be emphasized. China's green certificate trading and renewable energy quota mechanism should be used as a reference.

Finally, in the medium and long term, the price of renewable energy power generation and the cost of energy storage must be paid by its beneficiaries. Price compensation is also necessary to promote the co-development of renewable energy and energy storage. We suggest the establishment of a long-term market-oriented mechanism and an energy storage price mechanism which considers the holistic perspective to properly assign the payment for “green value” to those which benefit most from it.

Author: Chen Haisheng, Chairman, China Energy Storage Alliance

2020 China Energy Storage Policy Review: Entering a New Stage of Development in the 14th Five-year Plan Period

Under the direction of the national “Guiding Opinions on Promoting Energy Storage Technology and Industry Development” policy, the development of energy storage in China over the past five years has entered the fast track. A number of different technology and application pilot demonstration projects have been launched, many key technical components have reached an advanced level of maturity, numerous key technical norms and standards have formed, and internationally competitive market players have entered the playing field. While it is true that the development of China's energy storage industry has moved from a technical verification stage to a new stage of early commercialization, the industry still faces many challenges which hinder development, and true "industrialization" has not yet materialized. As we enter the 14th Five-year Plan period, we must consider the needs of energy storage in the broader development of the national economy, increase the strategic position of energy storage in the adjustment of the energy structure, and make known the important role of energy storage in the social and economic development of China. While looking back on 2020, we also looking forward to the development of energy storage industrialization during the 14th Five-year Plan, as policy and market mechanisms become the key to promote the full commercialization and large-scale application of energy storage.

Build a solid foundation for the training of talents and increase the strategic importance of energy storage

In 2020, under the direction of the National Development and Reform Commission to promote energy storage and lay a solid foundation for industrial development, the Ministry of Education, the National Development and Reform Commission, and the Ministry of Finance jointly issued the “Action Plan for Energy Storage Technology Discipline Development (2020-2024),” proposing to create a number of undergraduate majors, secondary disciplines, and cross-disciplines specializing in energy storage technology over the next five years. Xi'an Jiaotong University, North China Electric Power University, and other colleges and universities have already added such energy storage disciplines. The “Suggestions on Accelerating the Reform and Development of Postgraduate Education in the New Era” also included the construction of an innovative platform for the integration of energy storage technology, industry, and education, and implements a special project for independent training of talents in core technical areas. The construction of a discipline system and the training of professionals through these policies will help to build a solid industrial foundation for energy storage.

Industry development guidance and pursuit of optimal energy prices

In July 2020, the National Energy Administration issued the “Notice on Organization and Application of Scientific and Technological Innovation (Energy Storage) Pilot Demonstration Projects.” The issuance marked the conclusion of a years-long solicitation of national energy storage demonstration projects with the shortlisting of eight large-scale energy storage projects in a range of applications. The demonstration projects will help to promote the introduction of new policies and market mechanisms through analysis and synthesis of successful experiences and current challenges relating to a diverse range of energy storage projects.

The National Development and Reform Commission and the National Energy Administration proposed a "two integrations" energy development strategy in the “Guiding Opinions on the Development of ‘Integrated Wind, Solar, Hydro and Thermal Storage’ and ‘Integrated Source, Network, and Load’ (Draft for Comment).” The proposal combines the advantages of different energy technologies with the rapid and flexible adjustment capabilities of energy storage. However, the pursuit of low energy costs through the "two integrations" strategy is not realistic in the short term. We must also consider the value and cost of the societal benefits of the green development which these projects bring. Promoting the construction of an intelligent, efficient, and green energy system requires the entire nation to accept and bear these comprehensive costs and set aside the single pursuit of only the absolute lowest energy costs.

Continued electricity market reforms create an open and fair environment

As electricity market reforms continue, market rules gradually tilt to new market players such as energy storage. The “Basic Rules of Medium-and Long-term Electric Power Trading” defines the identity of energy storage enterprises participating in market transactions. Jiangsu, Jiangxi, Shanxi, Qinghai, and other regions have released construction plans for electric power spot markets and proposed long-term development directions for ancillary services markets. Among these proposals, "establishing a market mechanism for ancillary service costs shared by users and power generators" has become the key for promoting the commercial application of energy storage in the future. The “Notice on the Signing of Medium-and Long-term Electric Power Contracts in 2021” proposes to promote medium-and long-term transactions with load curves on both the generator and user side. Because it is difficult to predict market supply and demand in the short term, it is still necessary to refer to the existing catalogue electricity price or guiding electricity price to determine the peak and off-peak price difference. Although China has carried out medium-and long-term trading for many years, and has also put forward the idea of transitioning to a new price model, there are still some regions where the price formation mechanism does not match the actual power supply and demand. The peak and off-peak price gap has also been reduced through medium-and long-term transactions, which also reflects the passivity of the market mechanism. In the future, the trend of widening the peak and off-peak price gap will continue according to power supply and demand. Behind-the-meter energy storage arbitrage business models will still have guaranteed value, though the ability of energy storage to participate in spot market bidding must also gradually improve.

Under the guidance of the “Work Plan for Improving the Power Ancillary Services Compensation (Market) Mechanism,” ancillary services markets have been constructed in multiple regions in recent years, and energy storage has also been commercialized in Guangdong, West Inner Mongolia, Shanxi, North China, and other regions. However, the high compensation brought by the provision of high-performance energy storage services also creates risks for market capital use, and the continued adjustment of policies has also impacted investment in energy storage projects. In 2019, adjustments were made to the compensation calculation in West Inner Mongolia and North China. In 2020, Guangdong also made an adjustment to its settlement process, while West Inner Mongolia once again adjusted its compensation calculation method. Shanxi, Qinghai, Hunan, and other regions have also made downward adjustments to the peak regulation compensation standards for energy storage participating in ancillary services. Policies have changed frequently in less than a year. This lack of a long-term market mechanism has become a prominent problem restricting the commercial development of energy storage.

Despite this, ancillary service market rules solve the basic identity problem of energy storage participating in the market. Energy storage receives a market subject status equal to that of power generation enterprises, power sales enterprises, and power users, and third parties are permitted to offer their services to the market. Independent energy storage providers in Fujian, Jiangsu, Shanxi and other regions are permitted to apply for power generation business licenses, and are permitted to participate in ancillary services provision.

Renewable energy + energy storage becomes a leading trend, but commercial development still faces difficulties

As large-scale renewable energy continues to expand, the pressure and responsibility to supply guaranteed power generation becomes more intense. In 2020, numerous local governments and power grid departments once again put forward a demand for renewable energy projects to be equipped with energy storage systems matching 5% to 20% of renewable energy generation capacity. Energy storage has also become a precondition for priority grid connection and priority consumption. However, under existing system costs and without a mechanism in place for assigning cost coverage responsibility, the development of integrated renewables and storage cannot be achieved overnight. Relying solely on the principle that "charge and discharge electricity prices and settlement shall be determined in accordance with relevant national regulations" cannot solve commercial development challenges, but instead shows that policy is oriented towards transferring responsibility. During the process of charge and discharge, energy storage switches identity from that of a user to that of a power generator. Peak-shaving compensation and feed-in charges cannot be paid repeatedly, while independent energy storage projects are also faced with the risk of double charges. In addition, policy must also gradually raise the threshold of entry for projects in the market to avoid the possibility of safety accidents inhibiting industry development.

It is not necessary to use market mechanisms and policy compensation to give specific support to energy storage. Instead, energy storage should be allowed a fair and open market in which it is allowed to compete with other market entities. A sound market environment is the core for comprehensive commercial development of energy storage.

Electricity prices are optimized and adjusted, and behind-the-meter energy storage prices becomes more reasonable

A new round of transmission and distribution electricity price and retail electricity price adjustments resulted in numerous regions reducing consumer electricity prices, adjusting peak and off-peak price differences, and adjusting the peak and off-peak price implementation period. With the large-scale deployment of renewable energy, the original mode of determining peak and off-peak electricity prices according to consumer electricity consumption habits has changed, and net load has become the basis for peak and off-peak price adjustment. In 2020, Jiangsu, Zhejiang and other regions further reduced the off-peak electricity price and widened the peak and off-peak price gap. Regions such as Hubei not only widened the peak and off-peak period, but also added a super peak electricity price and adjusted their peak and off-peak price differences. Shandong, Gansu and other regions implemented complete price adjustments for all TOU periods. While the widening of the peak and off-peak price difference is beneficial to behind-the-meter energy storage applications, energy storage charge and discharge strategies must also be adjusted to adapt to the changes to the peak and off-peak period.

At the same time, Beijing’s Chaoyang District continued to provide 20% initial investment subsidies for energy storage projects after energy storage was incorporated into the special funds for energy conservation and emission reduction in 2019. After Hefei, Suzhou, and other regions granted subsidies for distributed solar+storage and energy storage systems, Xi'an and Shaanxi begin providing 1 RMB/kWh charging subsidies for energy storage in solar+storage systems. Energy storage technologies are also needed in new applications such as 5G base stations, data centers, and EV support facilities. Consumers in these industries will rely on energy storage to help solve distribution capacity problems, provide emergency power backup, and reduce electricity expenditures. Related energy storage applications can also receive regional subsidies in Guangdong, Kunming, Hefei and other regions. With the increasingly widespread use of EVs, further integration of solar+storage+charging can also be expected.

Demand response and consumer peak shaving overlap, and adjustment resources require increased efficiency

The peak-shaving market is expected to connect with the spot market mechanism, using market-oriented price mechanisms to mobilize resources to respond to the demands of the power system. However, to mobilize behind-the-meter adjustment resources, power operations regulators in Shanghai, Jiangsu, Guangdong, Zhejiang, Shandong, and Henan launched the construction of a demand response mechanism based on the 2013 demand response trial program. Compensation comes from surplus capital pools such as super peak electricity prices and renewable energy transactions. In addition, energy regulatory departments in North China, Jiangsu, and Shanxi opened the door for third-party entities and consumer resources to participate in peak-shaving ancillary services, though peak-shaving compensation in some regions is still provided by power generation enterprises. In areas in which ancillary services costs are not transmitted to the consumer, there are policy change risks for non-generation entities which earn profits from ancillary services.

Due to the high overlap between demand response execution time and peak and off-peak electricity prices, there is still room for flexible design of the baseline, so the profits for energy storage participating in demand response are relatively limited. The existing peak shaving and demand response mechanism design provides energy storage charging and discharging compensation which can increase energy storage revenue. However, under the existing peak and off-peak price mechanism, independent energy storage charging and discharging for peak shaving is already in place. If peak shaving and demand response implementation are consistent with the implementation of peak and off-peak price periods, there will be some overlap in compensation. In addition, although peak shaving and demand response are directed by different departments, the response mechanism is basically the same, and there is still the problem of compensation payments duplicating. In some regions, peak shaving is frequently dispatched, with cumulative days equaling as much as half a year. A resource response that was originally a short-term emergency service has become a continuous demand. Rather than continue this practice, it would be better to flexibly change the peak and off-peak pricing period and prices, and allow users to cover the cost of energy storage. Therefore, it is necessary to integrate the process of spot market construction to effectively link consumer peak shaving, demand response, and market-based pricing mechanisms to avoid overlapping use of resources and invalid payment of funds. The baseline and response mechanism should be adjusted reasonably to support the energy storage technology as it provides services to the power system.

The power grid supports the development of energy storage and promotes its role in the energy system

In 2019, the national government made it clear that “costs unrelated to the power transmission and distribution business of grid companies,” including the cost of energy storage facilities, should not be included in transmission and distribution prices. China’s major grid companies followed by stating they would not carry out grid-side electrochemical storage investment, leasing, or contract energy management, nor would they construct new pumped hydro storage projects. Currently, due to the inability to match regulatory capabilities with the demand for grid investment in energy storage projects, it is reasonable to prohibit grid investment in energy storage projects under the principle of ensuring market fairness. However, this does not mean that the regulatory mechanism is not evolving. In 2020, the method by which the power grids promoted energy storage development changed. In the “Key Work Arrangements for Reform in 2020” and the “Opinions of State Grid Co., Ltd. on Comprehensively Deepening Reform and Striving for Breakthroughs,” the power grid expressed its intention to implement a new business plan for energy storage and cultivate new momentum for growth based on strategic emerging industries such as energy storage. The “Key Points for Professional Work on Smart Power Utilization in 2020" also suggested strengthening customer-side energy storage application research and gradually clarifying system access requirements. In addition, the “Energy Law of the People's Republic of China (draft for comment)” encouraged the development of smart grid and energy storage technology. The National Energy Administration's response to Recommendation No. 9178 of the Third Session of the Thirteenth National People's Congress stated that for some energy storage projects deployed to defer investment in new transmission lines and substation equipment, consideration will be given to include their construction and operations costs into T&D service costs. The response also suggested that continued research would seek to create an effective model for covering the costs of energy storage in order to support the orderly development of grid-side storage.

Implementing large-scale commercial development of energy storage in China will require significant effort from power grid enterprises to promote grid connection, dispatching, and trading mechanisms, and also share the responsibility of the regulatory authority for energy storage safety risks to ensure the high-quality application of energy storage.

How Can Energy Storage Overcome Obstacles to Participation in the Ancillary Services Market?

In November 2020, the Central China Energy Regulatory Bureau released the “Jiangxi Province Power Ancillary Services Market Operations Regulations (Trial)” (referred to as the “regulations” below). In comparison to the earlier draft release, the trial regulations have added content which encourages independent energy storage systems to participate in the peak shaving ancillary services market.

Since the National Energy Administration’s 2017 publication of the “Improving Power Ancillary Services Compensation (Market) Mechanism Workplan,” multiple regions have followed with market operations regulations for ancillary services, providing support for energy storage technology applications. Considering these developments, what is the current status of the ancillary services market in China? What challenges remain to be resolved?

Independent Energy Storage Has Advantages

Industry experts believe that although the release of the Jiangxi regulations provides clarification of energy storage’s identity, the compensation mechanism and subsidies for energy storage provided in the regulations are not enough to cover the investment costs for storage. Market regulations help clear obstacles related to energy storage’s identity, but do not provide simple price compensation.

“Independent energy storage stations are an emerging trend. When energy storage is tied to other systems, it must share its earnings with those other systems,” China Energy Storage Alliance senior policy research manager Wang Si told reporters.

Wang Si believes that independent energy storage possesses two advantages. First, companies which invest and operate independent energy storage systems may operate projects on their own, collecting earnings for themselves with a greater degree of flexibility. Second, independent energy storage systems are better able to aggregate, creating greater value through energy storage sharing. This changes the conventional business model of providing service for just one user, allowing an energy storage system to instead provide service for multiple generation companies, users, and even the entire power system. “Therefore, it is necessary to not only design such systems, but also allow them to participate in the ancillary services market. This will increase the overall effectiveness of the systems,” said Wang Si.

According to Wang Haohuai, director of the China Southern Grid Power Dispatch Center, “with energy storage’s identity in the market defined, operator autonomy is increased. Otherwise, operations and settlement are limited by the entity to which the storage system is tied to, which will affect enthusiasm for investment.” As Wang Haohuai also stated, energy storage follows market service regulations. Implementation of a pay-for-performance mechanism should also be guided by a top-to-bottom evaluation or market mechanism. “For example, once large-scale renewable energy penetrates the grid, exactly how much peak shaving and frequency regulation resources are needed, and how fast, accurate, and stable must they be? Only when operations, market, and settlement provisions have established relevant indicators will energy storage be able to achieve a sufficiently fast regulatory speed and earn a higher level of compensation.”

The Energy Storage Cost Mechanism Continues to Face Challenges

Energy storage has yet to reach a fully commercial stage, making marketization of ancillary services a challenge to commercial operations of energy storage.

According to Wang Si, the key to solving the problem of ancillary services commercialization lies in the power market. Current market regulations and related policies do not support market entry of energy storage. This is especially true of ancillary services market and spot market regulations, which cannot support the full participation of storage in the market, nor allow it to receive full benefits. “Following power market reforms, barriers to energy storage’s participation in the market were removed, and new doors were opened for energy storage to earn profits. We predict that energy storage costs will continue to decline, particularly since the large-scale effect of energy storage in the power system has yet to be reflected.”

Wang Si went on to state that energy storage’s costs should not be incorporated in power costs, “in the current renewable energy quota system, it is the consumers who are made to bear the duty of using green electricity, and the corresponding costs are reflected in financial products such as green certificates. In the future, power generators will gradually transmit the cost to the consumer side, and receive payment from the beneficiary. To support the development of renewable energy and energy storage, corresponding policy support is needed to generate economies of scale, further reduce costs, and enhance competitiveness."

According to Wang Haohuai, the power market system is currently under construction, and the commercial value assessment of energy storage is undergoing major policy changes, creating both risks and opportunities. For example, in addition to the challenges of the “pay-for-performance” mechanism, there are also issues such as the inability to transfer energy storage costs to the consumer, preventing the beneficiary from being the one who pays. “Combined energy storage and renewable energy costs are still high at the current stage. In order to promote green energy consumption, consumers must take on the costs of green energy development.”

Policy Changes Bring Investment Risks

Ancillary services include frequency regulation, peak shaving, operating reserves, voltage control, blackstart, and other services. Among these, peak shaving is a unique service in China. Peak shaving is the practice of short-term regulation of power to match output generation with changing load, balancing power and encouraging greater consumption of renewable power. “Whether peak shaving and spot markets will be integrated in the future or will function in parallel is a matter of discussion among experts,” said Wang Haohuai.

Electricity market rules have not yet formed a long-term mechanism. Marketization is still at a transitional stage, which puts projects with a long investment payback period at risk when regulatory changes occur. “Everyone invests in energy storage projects under the current regulatory system, so they also face greater risks from policy changes,” said Wang Si.

Wang Si pointed out that the release of ancillary services market operations regulations across many regions has given energy storage an opportunity to expand profit margins to a certain extent, but that the vast majority of policies and regulations cannot offer compensation which fully covers investment costs.