Divining China's Energy Future

Reading the “Internet+” Smart Energy Development Guidelines

On February 29th, 2016, the NDRC, NEA, and Ministry of Industry and Information Technology released Guiding Opinions on “Internet+” Smart Energy Development.

This policy document focuses on the Energy Internet, a concept which has engulfed Chinese energy and grid circles for more than a year.

With the release of this document, we have an official take on the future of China’s grid.

The Opinions established a definition for this Energy Internet concept: “a new industry development model based on a deeply integrated network of energy production, transmission, storage, consumption and markets. It is characterized by device intelligence, energy diversity, information symmetry, distributed generation and demand, a flat structure, and open exchange.”

Until now, energy storage in China has been perceived as a set of technologies or devices used in certain links in the grid. But the Opinions take a different approach, describing energy storage as a standalone link in the energy chain, alongside production, transmission, and consumption. This is the first time that national government bodies have recognized energy storage as a separate and critical part of the future energy system.

The Energy Internet covers power, heat, oil and gas, and transportation. By highlighting energy storage as an independent link in the energy chain, policymakers are laying a foundation for the beneficial use of energy storage across the board.

The Opinions take a broad look at energy storage, calling for the development of “high-capacity, low-cost, high-efficiency and long-lived energy storage products and systems in electricity, thermal, and clean fuel storage.” This inclusive approach places energy storage at the center of the interconnections between power, heat, transportation and gas networks.

Bulk Energy Storage and Renewables Integration

The Opinions argue “suitably-sized energy storage facilities should be located in energy production centers to optimize grid and energy system operation."

At present, energy storage facilities used for renewables integration are generation-side resources, co-located with particular power stations. The Opinions call on years of operational experience and institutional input to suggest that energy storage functions better as a shared resource located in areas with high energy production. This maximizes the value of expensive storage installations by serving multiple stations at once.

Better sited energy storage would also gain value by giving grid operators the ability to tap into other operational benefits of the technology.

Some experts estimate that energy storage installations equaling 5-10% of the generation capacity in a renewable energy producing region would be sufficient to address intermittency issues. With China’s 12th Five-Year Plan calling for 200 gigawatts of wind by 2020, the grid would benefit from an additional 10-20 gigawatts of energy storage – an enormous opportunity.

Distributed Energy Storage – the Future of the Industry

The Opinions also promote the deployment of “distributed energy resources in communities, rooftops, and homes through the use of grid-friendly, effective and distributed energy storage.”

Distributed energy storage has attracted a lot of attention for its flexibility, low capital requirements, and value to the consumer by supporting on-site solar generation, demand response, and bill management.

The Opinions also bring up networked management of energy storage devices, calling for energy storage device databases, remote operation and control of distributed storage devices, and energy storage cloud platforms. It encourages modular system design, standardization, networked control over second-life batteries, and support for unhindered and flexible energy exchange. The document also promotes energy storage as a provider of backup power, peak shaving, frequency regulation, and other services.

But because China’s residential electricity rates are so low, residential energy storage is not yet profitable. However, in some industrial parks and among some high-energy consuming businesses, users are beginning to consider solar-plus-storage as a way to reduce electricity bills.

While the present opportunities for energy storage are limited, China remains committed to revolutionizing its energy system. This means that demand response, time-of-use rates and demand charges are likely to grow. As these policies spread and mature, distributed energy storage may well become an attractive market.

The Opinions also mention electric vehicles: “Promote the use of used EV batteries in stationary energy storage. Build an operational EV cloud platform based on elements of the grid, energy storage and distributed energy consumption. Explore the use of electric vehicles in networked platforms to participate in direct energy trading, demand response, and other models.”

According to official targets, China aims to bring five million electric vehicles to the road by 2020. Electric vehicle charging can have a serious impact on the grid, and so having effective control over distributed EV batteries to provide peak shaving, frequency regulation, or engage in demand response could help maximize the value of electric vehicles.

According to the Opinions, the rollout of the Energy Internet model is set to take place in two phases. From 2016 to 2018, the government will support pilot demonstration projects of different types and scales. From 2019-2025, the emphasis will be on diversification and scaled-up development, and establishing the Energy Internet as a driver of GDP growth.

While its clear that China is a long way from achieving these goals, its telling that national decision-making bodies are endorsing such powerful language to describe their vision of the grid to come. What's most uncertain is how China's vested grid interests will adapt to -- or resist -- these changes.

A Look Ahead at 2016: A Message from CNESA Secretary-General Tina Zhang

2015 was a landmark year for energy storage in China.

Season's greetings from the China Energy Storage Alliance.

In March, the government announced long-awaited power sector reforms that promise new opportunities for energy storage in an increasingly market-based power system.

Policymakers prepared the country’s next Five-Year Plan, the policy lodestone which will guide China’s development through 2020. This carefully crafted document is the key to meeting China’s ambitious energy and environmental targets.

And in the Paris COP21 talks, China emerged as a world leader by arguing that clean energy can be a tool to simultaneously address climate change and meet development goals.

Looking ahead, all indicators point to continued strong growth in clean energy and a greater role for markets and innovation in China’s transition to a more sustainable economy.

Of course, this transition is already well underway. As of September, China has installed 38 gigawatts of grid-connected solar, and the country reached 100 gigawatts of wind capacity earlier this year.

Now it’s our turn.

Energy storage is going to be a big part of China’s energy revolution, and policymakers know it. Last month, China’s national governing body called for increased deployments of energy storage and smart grids, higher penetrations of distributed generation, a greater share of renewables in China’s energy mix, more efficient and low-carbon dispatch, and greater numbers of electric vehicles on the road.

For now, China’s energy storage market remains dominated by pumped hydro: only 106 megawatts of China’s 21.9 gigawatts of energy storage capacity come from battery storage, according to CNESA’s Energy Storage Project Database. Nevertheless, this number still puts China among the top five countries in terms of grid-connected battery capacity, and installations are rising fast. On average, China’s battery storage capacity has more than doubled each year since 2010.

But it’s not just batteries making the news. In October, China’s top energy ministry collected bids for concentrating solar power generation demonstration projects -- most of which included molten salt energy storage. Several more gigawatts of CSP projects are in the pipeline, suggesting that thermal energy storage in China is finally starting to turn the corner.

Where do we see the industry going in 2016 and beyond?

Microgrids and Distributed Generation

About half of China’s non-hydro energy storage capacity is paired with microgrids or distributed generation, and we foresee that these will remain strong growth areas in the coming year. Successful demonstration projects have proven that China’s islands and remote western regions are prime targets for energy storage deployments, while industrial parks, hospitals, data centers, and other urban buildings are now coming into the spotlight. And last July, the government announced a plan to promote renewable energy-based microgrids nationwide, a great sign for the development of solar-plus-storage in China.

Demand-side Management

There is enormous potential for energy storage in demand side management, thanks to policy commitments from the highest levels of government. Last year, Chairman Xi Jinping announced a campaign to promote efficient energy use in order to meet the country’s carbon emissions and air pollution targets. This drive – as well as our industry connections and technical knowledge – is why CNESA was selected by the Beijing municipal government to lead a demand response pilot program in Beijing. This past August, we helped reduce peak load by 70 megawatts just as demand was set to reach a new nationwide record.

Electric Vehicles

We’re also excited by the future of electric vehicle grid integration. It’s no secret that China’s EV market is booming; automakers sold over 130,000 plug-in electric vehicles in the first three quarters of 2015, double the number sold in the same period last year. This is a great step forward in the electrification of China’s transportation sector, but it also represents a huge challenge for Chinese grid operators – a challenge that energy storage and smart grid technology companies are well-positioned to solve.

While China's energy storage market is primed for growth, challenges still remain.

China is still an emerging market, with all the risks that can bring. Regulatory changes are forthcoming, but there is still a great deal of uncertainty and a lack of well-defined value streams. That’s why our team works hard to keep you informed via our monthly newsletter, annual white paper, and customized market and policy insights.

Strong partnerships are also a must, which is one reason we organize China’s premier energy storage conference each year. In June, we held our fourth annual Energy Storage China Conference and Expo, our largest to date with over 700 attendees and 60 presentations from top policymakers, industry leaders, and energy researchers. The event is a great opportunity to learn more about China’s energy storage ecosystem and to make lasting partnerships in the world’s largest emerging market. I invite you to join us for next year’s event, to be held May 10-12th in Beijing.

Since 2010, CNESA has brought you the latest developments and opportunities for partnerships in energy storage. In 2016, I hope you’ll join us as we lead the way towards building a cleaner, smarter and stronger world.

China's Grid and the Electric Car

Courtesy: BYD

Thanks to generous subsidies and incentive programs, electric vehicle sales in China are booming. Chinese EV drivers enjoy a number of perks, including tax incentives when purchasing a vehicle and exemptions from restrictions designed to reduce traffic congestion.

In part due to these measures, sales of plug-in electric vehicles have soared. In the first nine months of 2015, automakers sold 136,733 units – twice the amount sold in the same period last year, according to Wards Auto.

These policies are part of a drive to put 5 million new energy vehicles (NEVs) on Chinese roads by 2020. Although it’s unclear whether or not this target will be met, it is certain that the grid will be faced with new challenges and opportunities as more plug-in electric vehicles hit the road.

In particular, Chinese regulators will need to begin examining how electric vehicle demand response can help address grid instability and support China’s transition to a low-carbon power system.

Electric vehicles and demand response

As the transportation sector electrifies, electricity consumption patterns will change. In order to meet demand, utilities need capacity and incentive mechanisms to address potential spikes in consumption. A study commissioned by the Regulatory Assistance Project and the International Council for Clean Transportation compared the expected impact on peak load in various countries as the number of plug-in electric vehicles rises. The report found that China’s grid was particularly susceptible to disruption in cases of high EV penetration.

To avoid power shortages, Chinese regulators will need to adopt measures to minimize the impact of electric vehicle charging on the grid. Policymakers have several options on the demand side to do this.

Programmable charging

Programmed charging allows grid operators to control EV load. In this model, EVs receive signals from the grid to optimize efficiency and reduce grid impact, while also factoring in battery constraints and the user's charging requirements.

EV programmable charging can be regarded as a flexible demand response resource, providing a certain amount of peak shaving functionality. Via smart grid signals and time-of-use pricing incentives, EV owners can be encouraged to charge their vehicles when wholesale electricity prices are low. Entities like charging facility operators and vehicle companies can act as load aggregators, earning subsidies and lowering EV lifetime ownership costs via participation in such demand response programs.

Large scale implementation of programmable charging faces several problems: chargers and charging stations do not all support remotely programmed control, there are issues with ITC standards and data compatibility issues, and there is a lack of attractive pricing mechanisms and business models.

Vehicle-grid integration (V2G)

Vehicle-to-grid integration (V2G) takes the role of EVs a step further by using the vehicle battery to provide grid services, including peak shaving, frequency regulation, renewables smoothing, and non-power supporting functions. An NRDC study, Electric Vehicles, Demand Response and Renewable Energy – Jointly Advancing Low Carbon Development, estimated that vehicle-to-grid integration could yield billions of yuan in cost savings each year by using electric vehicles for flexible capacity.

But V2G, while technologically feasible, still requires a great deal of standardization and business model development. Most EVs and charging infrastructure do not support output to the grid, ancillary service markets are not open to such participants, and the extra wear and tear on vehicle batteries will be a disincentive unless proper compensation is provided to vehicle owners. These challenges are compounded in China due to a regulatory framework that makes market-driven demand response particularly challenging.

Demand Response with Chinese Characteristics

China’s current load management mechanisms are, to a large degree, vestiges of the planned economy era. Chinese grid operators typically rely on administrative rationing during electricity shortages, rather than market-based demand response.

Nonetheless, China is implementing a small number of demand response pilot programs, including one in Beijing, which are helping set the stage for policy reforms expected to be released soon. In March 2015, the government introduced power sector reforms addressing issues that will affect demand response: pricing reforms, ancillary services markets, and the opening up of wholesale electricity markets. Those reforms will be followed by more specific policy measures later this year.

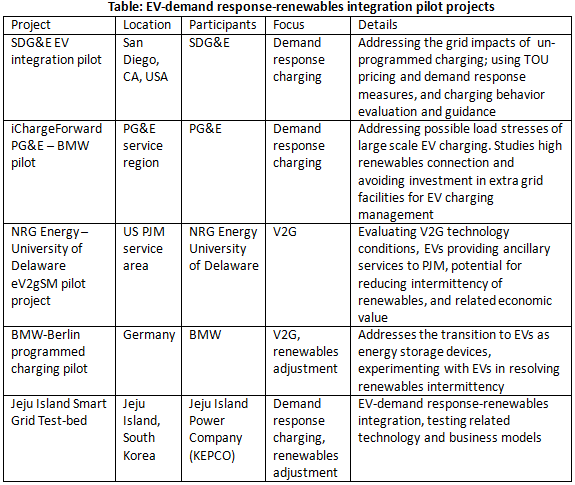

In the meantime, more demonstration projects integrating electric vehicles and grid operations are needed. Internationally, there are a number of demonstration projects which may serve as good models.

At the time of writing, we are unaware of any electric vehicle demand response programs in mainland China. But with record-breaking electric vehicle sales unlikely to slow down, we fully expect to see these programs coming soon.

Original article by Daixin Li, translation by Matt Stein, editing by Charlie Vest.

Archive

SUBSCRIBE

Sign up for our free monthly newsletter to stay informed about the Chinese energy storage market.

Quisque iaculis facilisis lacinia. Mauris euismod pellentesque tellus sit amet mollis.