China Announces Renewables Quota, But Is It Enough?

On March 3rd, the National Energy Administration released “Guiding Opinions on Establishing Renewable Energy Portfolio Standards,” which set renewable energy consumption targets for China. The country aims to rely on renewable energy for 15% of total primary energy consumption by 2020, and 20% by 2030. Non-hydro renewables should produce 9% of consumed electricity by 2020. The Opinions break down the non-hydro renewable electricity consumption requirements for each province and region, shown below.

| Region | Region | ||

|---|---|---|---|

| Beijing | 10% | Hubei | 7% |

| Tianjin | 10% | Hunan | 7% |

| Hebei | 10% | Guangdong | 7% |

| Shanxi | 10% | Guangxi | 5% |

| Inner Mongolia | 13% | Hainan | 10% |

| Liaoning | 13% | Chongqing | 5% |

| Jinan | 13% | Sichuan | 5% |

| Heilongjiang | 13% | Guizhou | 5% |

| Shanghai | 5% | Yunnan | 10% |

| Jiangsu | 7% | Tibet | 13% |

| Zhejiang | 7% | Shaanxi | 10% |

| Anhui | 7% | Gansu | 13% |

| Fujian | 7% | Qinghai | 10% |

| Jiangxi | 5% | Ningxia | 13% |

| Shandong | 10% | Xinjiang | 13% |

| Henan | 7% | Total | 9% |

Based on the government 2020 forecasts for power consumption and renewable energy capacity, we made a few simple calculations.

| 2020 Installed Capacity | 2020 Annual Use-Hours | 2020 Generation | |

|---|---|---|---|

| Wind | 250 GW | 1728 hours | 432 TWh |

| Solar PV | 160 GW | 1133 hours | 181.3 TWh |

Sources: Renewable Energy Development 13th Five Year Plan (Draft Version); 2015 wind and solar generation statistics, NEA

Graph assumes 2020 generation patterns are similar to 2015. 2020 annual generation=Installed capacity*utilization hours. Annual use-hours (利用小时) is derived by dividing total generated electricity over the course of one year (GWh) by the total capacity of the generation fleet (GW).

Assuming that the overall capacity factors for wind and solar in China don’t change from 2015 levels (I’ll get to that in a moment), wind and solar together are expected to produce 613 TWh annually in 2020. The National Development and Reform Commission anticipates that the entire country will consume 7390 TWh in 2020, meaning that solar and wind generation would comprise about 8% of the total. Once you factor in biomass and other non-hydro renewables, you can just about expect to meet the Opinions’ target of 9% renewable electricity production nationwide by 2020.

Is it Ambitious Enough?

While the target earns marks for realism, it struggles to make the grade in terms of ambition. We based our above calculation on wind and solar consumption for 2015. Thing is, wind and solar consumption was disastrous last year. Average solar and wind curtailment reached 10%, with some regions experiencing curtailment rates exceeding 30%.

Additionally, experts are mixed in their assessment of the strength of the new policy. Back in 2012, aware that existing mechanisms wouldn’t be enough to drive renewable energy consumption, the NEA drafted policies establishing renewable energy consumption targets, called the “Renewable Energy Quota Management Method.” The policies included robust assessment and enforcement mechanisms, but due to conflicts of interest, the policies never went into effect.

The newly-announced energy consumption policy published this month cover many of the same topics, but is believed to be pretty weak in comparison with the 2012 draft proposal. Industry players have even dubbed the new rules “Renewable Energy Quota Lite.”

The new energy consumption policy does suggest the creation of a “green certificate” trading mechanism, which would allow utilities unable to meet their renewable energy consumption targets to trade with utilities who consume above their own target. It’s an interesting idea, but it lacks an existing management mechanism, and it doesn’t get to the heart of the problem – that China’s dispatch rules, transmission infrastructure, and regulatory support for distributed energy are still inadequate.

Regulatory gridlock notwithstanding, the government has attempted to address this problem through a variety of channels:

1) Promoting local consumption

Given that renewable energy resources are concentrated in China’s north, the National Energy Administration has been eager to encourage communities in that region to consume locally-generated renewable energy. To do so, the government has expanded direct electricity trading provisions for large consumers.

The results from this effort have been mixed, due to the fact that these areas have very few load centers to begin with. Even local consumers that do directly consume renewable energy often do so in a package deal that includes coal-fired generation to manage wind variability. In reality, these consumers are still buying very little power from renewable sources.

2) Power-to-gas

One option that has been under examination since 2012 has been power-to-gas, in which electricity is used to power hydrogen reformers. This hydrogen can then be transported to load centers via traditional pipelines. A number of influential organizations have begun research or demonstration projects in power-to-gas, including State Grid, Shenhua Group, and China Energy Conservation and Environmental Protection Group.

This method faces challenges as well. A stable hydrogen market is a prerequisite for commercializing power-to-gas, and such a market does not yet exist in China. Additionally, pipelines are firmly under the control of China’s oil companies, who so far have not been proactive in exploring this business model.

3) Energy storage

Combining energy storage with wind and solar production has already drawn significant attention in China. But regulatory barriers still stand in the way of making it a commercially-viable solution.

Let’s take a hypothetical lithium-ion battery energy storage system priced at 3000 RMB (US$460) per kWh, including all supporting equipment. If the battery operates to spec for 3000 cycles at 80% DOD, can the numbers pencil out?

The short answer is no. Such a system would have a lifetime cost of 1.04-1.25 RMB (US$0.16-0.19) per kWh discharged. China’s current feed-in tariff compensates wind generators at a rate between 0.47 and 0.54 RMB (US$0.07-0.08) per kWh. At these rates, generators using energy storage to store wind-produced electricity during times of grid congestion face the hard math that storing electricity costs more than it earns when fed into the grid.

Now, this math changes when those batteries can be dispatched to provide other services, particularly ancillary services to the grid. China’s ancillary services markets are still focused on generator responsibility, and are not yet open to the value that energy storage technologies can provide.

China’s grid is an institution with enormous inertia, so changes are bound to be slow. Nonetheless, we expect that China’s support for energy storage as an emerging technology and its concurrent power sector reforms are a positive signal that changes are on the way.

Divining China's Energy Future

Reading the “Internet+” Smart Energy Development Guidelines

On February 29th, 2016, the NDRC, NEA, and Ministry of Industry and Information Technology released Guiding Opinions on “Internet+” Smart Energy Development.

This policy document focuses on the Energy Internet, a concept which has engulfed Chinese energy and grid circles for more than a year.

With the release of this document, we have an official take on the future of China’s grid.

The Opinions established a definition for this Energy Internet concept: “a new industry development model based on a deeply integrated network of energy production, transmission, storage, consumption and markets. It is characterized by device intelligence, energy diversity, information symmetry, distributed generation and demand, a flat structure, and open exchange.”

Until now, energy storage in China has been perceived as a set of technologies or devices used in certain links in the grid. But the Opinions take a different approach, describing energy storage as a standalone link in the energy chain, alongside production, transmission, and consumption. This is the first time that national government bodies have recognized energy storage as a separate and critical part of the future energy system.

The Energy Internet covers power, heat, oil and gas, and transportation. By highlighting energy storage as an independent link in the energy chain, policymakers are laying a foundation for the beneficial use of energy storage across the board.

The Opinions take a broad look at energy storage, calling for the development of “high-capacity, low-cost, high-efficiency and long-lived energy storage products and systems in electricity, thermal, and clean fuel storage.” This inclusive approach places energy storage at the center of the interconnections between power, heat, transportation and gas networks.

Bulk Energy Storage and Renewables Integration

The Opinions argue “suitably-sized energy storage facilities should be located in energy production centers to optimize grid and energy system operation."

At present, energy storage facilities used for renewables integration are generation-side resources, co-located with particular power stations. The Opinions call on years of operational experience and institutional input to suggest that energy storage functions better as a shared resource located in areas with high energy production. This maximizes the value of expensive storage installations by serving multiple stations at once.

Better sited energy storage would also gain value by giving grid operators the ability to tap into other operational benefits of the technology.

Some experts estimate that energy storage installations equaling 5-10% of the generation capacity in a renewable energy producing region would be sufficient to address intermittency issues. With China’s 12th Five-Year Plan calling for 200 gigawatts of wind by 2020, the grid would benefit from an additional 10-20 gigawatts of energy storage – an enormous opportunity.

Distributed Energy Storage – the Future of the Industry

The Opinions also promote the deployment of “distributed energy resources in communities, rooftops, and homes through the use of grid-friendly, effective and distributed energy storage.”

Distributed energy storage has attracted a lot of attention for its flexibility, low capital requirements, and value to the consumer by supporting on-site solar generation, demand response, and bill management.

The Opinions also bring up networked management of energy storage devices, calling for energy storage device databases, remote operation and control of distributed storage devices, and energy storage cloud platforms. It encourages modular system design, standardization, networked control over second-life batteries, and support for unhindered and flexible energy exchange. The document also promotes energy storage as a provider of backup power, peak shaving, frequency regulation, and other services.

But because China’s residential electricity rates are so low, residential energy storage is not yet profitable. However, in some industrial parks and among some high-energy consuming businesses, users are beginning to consider solar-plus-storage as a way to reduce electricity bills.

While the present opportunities for energy storage are limited, China remains committed to revolutionizing its energy system. This means that demand response, time-of-use rates and demand charges are likely to grow. As these policies spread and mature, distributed energy storage may well become an attractive market.

The Opinions also mention electric vehicles: “Promote the use of used EV batteries in stationary energy storage. Build an operational EV cloud platform based on elements of the grid, energy storage and distributed energy consumption. Explore the use of electric vehicles in networked platforms to participate in direct energy trading, demand response, and other models.”

According to official targets, China aims to bring five million electric vehicles to the road by 2020. Electric vehicle charging can have a serious impact on the grid, and so having effective control over distributed EV batteries to provide peak shaving, frequency regulation, or engage in demand response could help maximize the value of electric vehicles.

According to the Opinions, the rollout of the Energy Internet model is set to take place in two phases. From 2016 to 2018, the government will support pilot demonstration projects of different types and scales. From 2019-2025, the emphasis will be on diversification and scaled-up development, and establishing the Energy Internet as a driver of GDP growth.

While its clear that China is a long way from achieving these goals, its telling that national decision-making bodies are endorsing such powerful language to describe their vision of the grid to come. What's most uncertain is how China's vested grid interests will adapt to -- or resist -- these changes.

University of New South Wales Partners with Chinese Torch Program

Australia and China are embarking on a decade-long collaboration effort to spark international energy and environmental innovation.

In a meeting on March 1, 2016, a leadership delegation from University of New South Wales met with representatives of the Chinese Ministry of Science and Technology’s Torch Program in Beijing. The two organizations aim to establish long-term research and development partnerships between UNSW and Chinese businesses through the development of an Innovation Precinct at the university. The meeting also included representatives from Chinese businesses in the fields of energy and environment, new materials, and biotechnology.

The Torch Program, established in 1988, strives to promote technology transfer and the commercialization of innovative technologies by developing international partnerships and high-tech industrial parks in China and around the world.

The Chinese program dovetails with UNSW’s recently announced 2025 Strategic Plan, which includes among its initiatives the development of a A$50 million Innovation Precinct. According to UNSW’s innovation statement released last year, the precinct “will bring together industry, small to medium sized enterprises (SMEs), entrepreneurs, investors and policy makers from around the world.”

As part of the proposed collaboration, the university is offering special services to international companies in exchange for industry investment in the university, according to Laurie Pearcey, director of international strategy for Greater China and India at UNSW.

The university is offering rent-free office space for international companies on the university's campus, as well as access to a team of business development advisers to help support the companies in their bids to enter the Australian and New Zealand markets.

At the heart of the program is the opportunity for collaborative research between UNSW experts and industry researchers. This collaboration is undergirded by the university’s commitment to provide full-ride scholarships for PhD students selected by industry partners, opportunities for permanent residency visas, and an innovative IP sharing scheme.

The IP sharing mechanism, called Easy Access IP, is designed to hasten commercialization of university-developed technologies via partnerships with industry. UNSW offers free IP licensing to select companies that invest in the university’s research efforts. As long as the companies allow continued university research, acknowledge UNSW as the inventor, and put the technology into use within three years, the university grants these companies permanent licensing to university IP.

Pearcey emphasized that UNSW is internationally recognized as a research leader in renewable energy, having set numerous world records in solar cell efficiency. The university also has top-tier facilities used to simulate solar cell manufacturing, and boasts its status as a national leader in providing research grant funding for collaborative research projects.

The formal partnership between the Torch Program and UNSW is expected to be signed in April, and the first round of industry partners will be announced in the third quarter of 2016.

Power Retail Pilots Open in Guangzhou, Chongqing

Citic Tower, Guangzhou, Credit: wyliepoon / Flickr

This February, two major Chinese cities announced the launch of new electricity distribution pilot projects. In these projects, private electricity retailers will provide electricity services directly to consumers, representing a major step forward in China’s eagerly awaited power sector reforms.

The Guangzhou Development District

The first of these reforms takes place in Guangzhou. According to a policy released by the Guangdong Economy and Information Technology Commission, the Notice on Launching Retail Reforms in the Guangzhou Development District, entities within the Guangzhou Development District that consume at least 10 gigawatt-hours of electricity per year may participate in a direct electricity purchasing program. These entities may either purchase electricity in a bilateral agreement with generators or choose an electricity retailer.

As a result of these reforms, power plant owner Hengyun and Guangzhou Economic Technology Development Zone State-Owned Asset Investment Company, formed an electricity retailer, Guangzhou Suikai Electric Services. It’s important to note that the distribution grid is owned by the development district. As Hengyun owns generators that can serve the District and because the district itself – rather than China’s giant state-owned grid company -- owns the distribution grid, the entire value chain from generation to distribution is controlled by this newly-formed utility.

Although on paper it looks as if only consumers meeting a minimum consumption of 10 GWh will be able to participate in the retail market, it’s likely that smaller users will be able to participate by aggregating their loads.

Reforms in Chongqing

Retail reforms are also taking effect at an industrial park in Chongqing. On February 3rd, the Chongqing Liangjiang Changxing Electric Co. signed agreements with twelve businesses located at the Liangjiang New Area. Electricity sales to the first of these companies will begin this March.

This electric retailer was formed by four companies: Chongqing Liangjiang Group, Yangtze Power, Fuling Julong Electric, and Zhongfu Thermoelectric. Chongqing Liangjiang Group is a state-owned distribution grid developer responsible for the Liangjiang New Area. Yangtze Power, the country’s largest listed hydropower company, owns a number of large power stations including the Gezhouba and Three Gorges Dams. Fuling Julong is a state-owned enterprise primarily involved in power generation and retail, electrical equipment and transmission maintenance. Zhongfu Thermoelectric is a thermal generation owner.

The retailer formed by these companies covers each link in the power chain, from generation to retail. Although the distribution grid at the Liangjiang New Area is partly owned by the grid, any new additions will be built and owned by the retail utility.

The Role of Industrial Parks in Retail Reform

One reason that retail pilot projects are taking off in these two industrial parks first is the fact that the retailers in these cases are vertically integrated from generation to distribution. It’s important that in each case, the industrial park owner is a part owner of the utility, allowing the utility to gain control over the park’s assets – such as the distribution grid. Moreover, the utility is guaranteed to have customers in the companies that operate in the park. This vertical integration is expected to result in savings of 26 million yuan (US$4 million) in 2016.

It’s unusual for business and industrial parks to own their own distribution grids, which makes the Guangzhou Development District a special case. Though now that electricity retail is now opening up, yet-to-be-built industrial parks are likely to become a focus point in retail reform.

Where does energy storage sit in all of this?

For industrial parks with access to their own generation, retail reforms are likely to vastly reduce electricity prices. These reforms also open up possibilities for distributed generation and microgrid development, both of which do well when combined with energy storage technologies.

Additionally, now that retail companies are directly serving industrial parks, there is likelihood that consumers will have access to a wider range of services, including energy efficiency, energy management, and demand response. Freed from the shackles of the traditional grid system, energy storage has new opportunities ahead.

China’s Top 10 Energy Storage Headlines of 2015

China’s energy storage market made big strides in 2015. Major policy shifts last year – from power sector reform, to microgrids, to demand response – brought new opportunities to the table for energy storage.

Looking back, our experts weighed on the state of the market to bring you the top ten energy storage stories from 2015.

1. China Announces New Power Sector Reforms

Without a doubt, China’s power sector reform tops the list of important energy storage stories last year.

Beginning last March, China’s dormant power sector reform regime fired back up, with major policy releases marking adjustments to China’s generation, retail, and consumption regulations.

The heart of the reform rests in a landmark policy piece published by the State Council and CPC Central Committee, called Further Deepening the Reform of the Electric Power System, widely known as Document No. 9 (9号文). This document established that this round of reforms would:

- Maintain a monopolized transmission system, but open up generation and distribution to market competition

- Open up competitive electricity retail pricing

- Establish the groundwork for diversified energy trading

- Promote demand-side management and energy efficiency programs

- Increase the ratio of renewable energy in the country’s generation mix

China’s reform strategy thus far has strived for institutional separation between government bureaus and market entities, between generators and grid operators, and between main grid services and unrelated business operations in other sectors.

Document No. 9 states that the current round of reforms will open up market competition in generation and retail electricity markets and promote private investment in distribution infrastructure. Most importantly, the document calls for strengthened government oversight and control over grid planning.

In 2016, we expect these reforms to open up new opportunities for energy storage, particularly in demand response, ancillary services, and distributed generation.

2. National Energy Administration Releases Microgrid Guidelines

In July, the NEA shook up the microgrid space, announcing that each of China’s provincial governments should begin planning microgrid pilot projects. In the Guiding Opinions on New Energy Microgrid Pilot Projects, the NEA specified that these pilot projects should strive to integrate high penetrations of variable renewable energy sources.

This document emphasized the importance of energy storage, suggesting that policymakers are increasingly aware of the benefits energy storage can bring to microgrids.

The policy made no mention of specific subsidies for these projects, only stating that “new energy microgrid projects [should] be economically reasonable, given a certain degree of policy support.” Microgrid developers in China currently face challenges due to the lack of regulatory structures that colleagues in the United States and Japan rely on to drive value – such as widespread time-of-use rates, tiered electricity tariffs, and compensation for peak shifting and frequency regulation services. However, the opening up of retail electricity markets is expected to be an opportunity to develop these common-sense changes.

3. New Lithium-ion Battery Industry Regulations

Last year, the Ministry of Industry and Information Technology published new policies to better regulate China’s sprawling lithium-ion battery industry. The regulations specify that battery manufacturers should meet a number of production criteria to earn necessary government certifications.

Beyond manufacturing baselines, the regulations also set requirements for product quality, establishing minimum standards for cycling and energy density.

In comparison to previously published regulations, these are relatively relaxed. Nonetheless, this round of industry regulations should have some effect in cleaning up a disorganized industry and establishing further battery manufacturing standards down the road.

4. A Broad Push for Demand Response

As China’s economy shifts from manufacturing to service, load profiles are expected to change as well. Recognizing the challenges of a peakier load profile due to more grid-connected air conditioners and other high-consumption devices, the National Development and Reform Commission (NDRC) and the Ministry of Finance has taken an active role in promoting demand response pilot programs in select cities across China’s urban east coast.

The China Energy Storage Alliance was selected as the first certified load aggregator for the city of Beijing, putting us at the forefront of the effort to roll out demand response in China. On August 12th, for example, CNESA helped reduce load by 70 MW as Beijing’s peak load hit new highs. Although demand response providers still face myriad challenges in China, we expect to see increased institutional support for demand response as a result of last year’s successes.

5. Molten Salt Thermal Solar Storage Heats Up

In September, the National Energy Administration announced an RFP for thermal solar procurements totaling one gigawatt.

Notable for energy storage providers is the fact that the government required each project to include at least one hour of energy storage at rated capacity. Looking at the projects submitted so far, industry watchers could expect see a 4 GWh bump in energy storage capacity in China by 2018 from these procurements alone.

6. It’s All About the Energy Internet

If there’s been one catchphrase on everyone’s lips, it’s been the “Energy Internet.”

The Energy Internet (or the Smart Grid, as it’s described in other circles) is a term to describe energy systems characterized by a high degree of renewable distributed generation, wide deployments of a variety of energy storage technologies, and energy exchange between prosumers.

The idea has caught on quickly among China’s energy policymakers. Last April, the NEA held its first conference on the Energy Internet, resulting in the country’s first action plan to focus on distributed generation, microgrids, demand-side management, contract energy management, data-based services, and other business models and products.

With government support, companies like IESLab, NARI Technology, Shenzhen Clou Electronics are combining devices and big data analysis to shift from traditional sales to infrastructure-as-a-service. Meanwhile, leading inverter manufacturers Sungrow Power Supply and Xiamen Kehua are expanding into energy storage. In the EV space, Qingdao TGOOD Electric and Zhejiang Wanma Co. are building EV charging stations across the country.

CNESA has been at the leading edge of these developments as well. Last December, CNESA and ENN Energy held the 2015 Energy Storage and Energy Internet Research Summit, with support from the National Energy Administration. Tsinghua University’s Energy Internet Innovation Institute and North China Electric Power University’s Energy Internet Research Institute co-organized the event, which brought over 150 academic and industry experts together to discuss how to support further research on building out the Energy Internet. This closed-door event focused on the common needs of the energy storage industry and the Energy Internet in order to help clarify new opportunities and business models for energy storage.

7. Financial Sector Interest in Energy Storage

As anywhere, a significant barrier to entry for energy storage technologies in China is a lack of financing sources to support commercialization and deployment.

To help resolve this problem, CNESA signed a three-year agreement with the Bank of Beijing last June, opening up one billion Chinese yuan in potential financing for CNESA member companies.

The agreement also aims to facilitate the creation of a crowdsourced equity fund to support smart grid development, supported by Chinese capital funds Mingwu Capital, Kaiwu Capital, Qingyu Fund, and a number of CNESA member companies.

8. Retail Reforms and New T&D Reform Pilots

One key element in China’s most recent round of power sector reforms will involve changing tariff structures for transmission and distribution services.

On April 15th, the NDRC published a document announcing the first steps on that road, including an expansion of T&D reform pilot programs and signaling the intention to hasten tariff reform.

For context, outside of Shenzhen and Inner Mongolia – where T&D tariff reforms were first piloted – grid operators are not held to any tariff structure. Rather, they make margins off the difference between the wholesale price and regulated retail price of electricity.

Now, additional provinces and regions are now taking up tariff reforms, including Anhui, Hubei, Ningxia, and Yunnan. The NRDC has specified that grid operators will be compensated based on “authorized costs plus a reasonable profit” – essentially a regulated grid transmission fee. The document also called on all remaining provinces to examine existing T&D assets, costs, and profit structures to begin laying the foundation for nationwide reforms.

Retail reforms are also driving changes in the power sector. Until recently, electricity retail was firmly in the hands of the large electricity monopolies controlling China’s T&D assets. In the few months since power sector reforms were announced, though, over ten companies have registered as electricity retailers.

With the opening of China’s retail market come opportunities for innovative retailers to provide new services to end-use consumers and to tap into new value streams through distributed generation, EVs, smart homes, and energy storage.

9. Growing Policy Support for EVs and Charging Infrastructure

In 2015, government policies on electric vehicles moved beyond subsidies and support mechanisms to begin engaging in greater industry regulation and technical standardization.

The government has continued to release policies supporting EV charging infrastructure deployment. In a set of guiding opinions published in September, the State Council emphasized the need for increased EV charging deployments to keep up with China’s surging consumer demand. The Opinions call for greater deployments, improved services, and better technical standardization .

In October, four national-level ministries jointly published the 2015-2020 EV Charging Infrastructure Development Guidelines, calling for “12,000 new centralized charging stations and 4.8 million distributed charging stations to meet demand from the national goal of 5 million electric vehicles,” by 2020.

Battery recycling has also gained national recognition. In September, the NDRC and MIIT published a draft paper guiding industrial policy for EV battery manufacturing and recycling. It also aims to establish a recycling and reuse system for these batteries.

10. Energy Storage China 2015 Held in Beijing

Last June, CNESA held its fourth annual Energy Storage China conference and expo in Beijing’s Crowne Plaza Hotel. The event was co-organized by event organizer Messe Dusseldorf and supported by the National Energy Administration

Kicking off with a training session on June 2nd, the four-day event featured sessions on global market developments, electric vehicles, stationary energy storage technologies, and distributed solar plus energy storage. The event also included an in-depth exploration of energy storage opportunities in light of China’s new power sector reforms. CNESA marked the event by releasing its annual energy storage industry white paper, which covers major trends in energy storage in China and around the world.

Energy Storage China 2015 was supported by an international coalition of energy storage trade associations, including BVES (Germany), CESA (California), IESA (India), and the Global Energy Storage Alliance. Last year’s event drew 700 attendees from over 10 countries, who enjoyed access to Chinese policymakers and leading utilities, generators, and energy storage solution providers. Attendees learned about global industry and regulation trends from 80 experienced speakers, and had the chance to promote their products, understand new business models, meet potential clients, and establish themselves in China’s growing market.

Energy Storage China 2016 will be held May 10-12th at the Beijing International Convention Center.

What's ahead for 2016?

2016 is going to be a big year for China. This March, China's national legislature is expected to approve the 13th Five-Year Plan, a far-reaching document that will guide investment and growth targets through 2020.

In this context, China watchers should expect a changing landscape for energy storage in 2016. Here's our take.

A Look Ahead at 2016: A Message from CNESA Secretary-General Tina Zhang

2015 was a landmark year for energy storage in China.

Season's greetings from the China Energy Storage Alliance.

In March, the government announced long-awaited power sector reforms that promise new opportunities for energy storage in an increasingly market-based power system.

Policymakers prepared the country’s next Five-Year Plan, the policy lodestone which will guide China’s development through 2020. This carefully crafted document is the key to meeting China’s ambitious energy and environmental targets.

And in the Paris COP21 talks, China emerged as a world leader by arguing that clean energy can be a tool to simultaneously address climate change and meet development goals.

Looking ahead, all indicators point to continued strong growth in clean energy and a greater role for markets and innovation in China’s transition to a more sustainable economy.

Of course, this transition is already well underway. As of September, China has installed 38 gigawatts of grid-connected solar, and the country reached 100 gigawatts of wind capacity earlier this year.

Now it’s our turn.

Energy storage is going to be a big part of China’s energy revolution, and policymakers know it. Last month, China’s national governing body called for increased deployments of energy storage and smart grids, higher penetrations of distributed generation, a greater share of renewables in China’s energy mix, more efficient and low-carbon dispatch, and greater numbers of electric vehicles on the road.

For now, China’s energy storage market remains dominated by pumped hydro: only 106 megawatts of China’s 21.9 gigawatts of energy storage capacity come from battery storage, according to CNESA’s Energy Storage Project Database. Nevertheless, this number still puts China among the top five countries in terms of grid-connected battery capacity, and installations are rising fast. On average, China’s battery storage capacity has more than doubled each year since 2010.

But it’s not just batteries making the news. In October, China’s top energy ministry collected bids for concentrating solar power generation demonstration projects -- most of which included molten salt energy storage. Several more gigawatts of CSP projects are in the pipeline, suggesting that thermal energy storage in China is finally starting to turn the corner.

Where do we see the industry going in 2016 and beyond?

Microgrids and Distributed Generation

About half of China’s non-hydro energy storage capacity is paired with microgrids or distributed generation, and we foresee that these will remain strong growth areas in the coming year. Successful demonstration projects have proven that China’s islands and remote western regions are prime targets for energy storage deployments, while industrial parks, hospitals, data centers, and other urban buildings are now coming into the spotlight. And last July, the government announced a plan to promote renewable energy-based microgrids nationwide, a great sign for the development of solar-plus-storage in China.

Demand-side Management

There is enormous potential for energy storage in demand side management, thanks to policy commitments from the highest levels of government. Last year, Chairman Xi Jinping announced a campaign to promote efficient energy use in order to meet the country’s carbon emissions and air pollution targets. This drive – as well as our industry connections and technical knowledge – is why CNESA was selected by the Beijing municipal government to lead a demand response pilot program in Beijing. This past August, we helped reduce peak load by 70 megawatts just as demand was set to reach a new nationwide record.

Electric Vehicles

We’re also excited by the future of electric vehicle grid integration. It’s no secret that China’s EV market is booming; automakers sold over 130,000 plug-in electric vehicles in the first three quarters of 2015, double the number sold in the same period last year. This is a great step forward in the electrification of China’s transportation sector, but it also represents a huge challenge for Chinese grid operators – a challenge that energy storage and smart grid technology companies are well-positioned to solve.

While China's energy storage market is primed for growth, challenges still remain.

China is still an emerging market, with all the risks that can bring. Regulatory changes are forthcoming, but there is still a great deal of uncertainty and a lack of well-defined value streams. That’s why our team works hard to keep you informed via our monthly newsletter, annual white paper, and customized market and policy insights.

Strong partnerships are also a must, which is one reason we organize China’s premier energy storage conference each year. In June, we held our fourth annual Energy Storage China Conference and Expo, our largest to date with over 700 attendees and 60 presentations from top policymakers, industry leaders, and energy researchers. The event is a great opportunity to learn more about China’s energy storage ecosystem and to make lasting partnerships in the world’s largest emerging market. I invite you to join us for next year’s event, to be held May 10-12th in Beijing.

Since 2010, CNESA has brought you the latest developments and opportunities for partnerships in energy storage. In 2016, I hope you’ll join us as we lead the way towards building a cleaner, smarter and stronger world.

China's Grid and the Electric Car

Courtesy: BYD

Thanks to generous subsidies and incentive programs, electric vehicle sales in China are booming. Chinese EV drivers enjoy a number of perks, including tax incentives when purchasing a vehicle and exemptions from restrictions designed to reduce traffic congestion.

In part due to these measures, sales of plug-in electric vehicles have soared. In the first nine months of 2015, automakers sold 136,733 units – twice the amount sold in the same period last year, according to Wards Auto.

These policies are part of a drive to put 5 million new energy vehicles (NEVs) on Chinese roads by 2020. Although it’s unclear whether or not this target will be met, it is certain that the grid will be faced with new challenges and opportunities as more plug-in electric vehicles hit the road.

In particular, Chinese regulators will need to begin examining how electric vehicle demand response can help address grid instability and support China’s transition to a low-carbon power system.

Electric vehicles and demand response

As the transportation sector electrifies, electricity consumption patterns will change. In order to meet demand, utilities need capacity and incentive mechanisms to address potential spikes in consumption. A study commissioned by the Regulatory Assistance Project and the International Council for Clean Transportation compared the expected impact on peak load in various countries as the number of plug-in electric vehicles rises. The report found that China’s grid was particularly susceptible to disruption in cases of high EV penetration.

To avoid power shortages, Chinese regulators will need to adopt measures to minimize the impact of electric vehicle charging on the grid. Policymakers have several options on the demand side to do this.

Programmable charging

Programmed charging allows grid operators to control EV load. In this model, EVs receive signals from the grid to optimize efficiency and reduce grid impact, while also factoring in battery constraints and the user's charging requirements.

EV programmable charging can be regarded as a flexible demand response resource, providing a certain amount of peak shaving functionality. Via smart grid signals and time-of-use pricing incentives, EV owners can be encouraged to charge their vehicles when wholesale electricity prices are low. Entities like charging facility operators and vehicle companies can act as load aggregators, earning subsidies and lowering EV lifetime ownership costs via participation in such demand response programs.

Large scale implementation of programmable charging faces several problems: chargers and charging stations do not all support remotely programmed control, there are issues with ITC standards and data compatibility issues, and there is a lack of attractive pricing mechanisms and business models.

Vehicle-grid integration (V2G)

Vehicle-to-grid integration (V2G) takes the role of EVs a step further by using the vehicle battery to provide grid services, including peak shaving, frequency regulation, renewables smoothing, and non-power supporting functions. An NRDC study, Electric Vehicles, Demand Response and Renewable Energy – Jointly Advancing Low Carbon Development, estimated that vehicle-to-grid integration could yield billions of yuan in cost savings each year by using electric vehicles for flexible capacity.

But V2G, while technologically feasible, still requires a great deal of standardization and business model development. Most EVs and charging infrastructure do not support output to the grid, ancillary service markets are not open to such participants, and the extra wear and tear on vehicle batteries will be a disincentive unless proper compensation is provided to vehicle owners. These challenges are compounded in China due to a regulatory framework that makes market-driven demand response particularly challenging.

Demand Response with Chinese Characteristics

China’s current load management mechanisms are, to a large degree, vestiges of the planned economy era. Chinese grid operators typically rely on administrative rationing during electricity shortages, rather than market-based demand response.

Nonetheless, China is implementing a small number of demand response pilot programs, including one in Beijing, which are helping set the stage for policy reforms expected to be released soon. In March 2015, the government introduced power sector reforms addressing issues that will affect demand response: pricing reforms, ancillary services markets, and the opening up of wholesale electricity markets. Those reforms will be followed by more specific policy measures later this year.

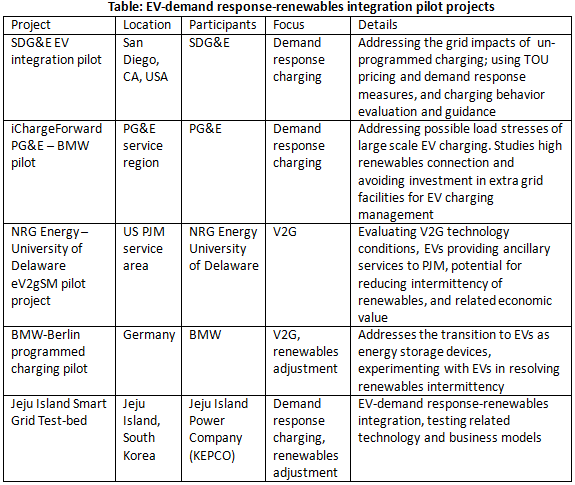

In the meantime, more demonstration projects integrating electric vehicles and grid operations are needed. Internationally, there are a number of demonstration projects which may serve as good models.

At the time of writing, we are unaware of any electric vehicle demand response programs in mainland China. But with record-breaking electric vehicle sales unlikely to slow down, we fully expect to see these programs coming soon.

Original article by Daixin Li, translation by Matt Stein, editing by Charlie Vest.

Dispatches from San Diego

This is part one in a four-part series on CNESA's trip to San Diego for the Energy Storage North America conference and expo. See parts two, three, and four.

We're happy to be here in San Diego. We're at the center of an energy revolution, and top industry leaders, academics and policymakers are here to show us what they've learned so far.

On the Ground in California’s Energy Revolution

Energy Storage North America 2015 began with site visits to San Diego’s most innovative energy storage projects. Byron Washom, director of strategic energy initiatives at UC San Diego, showed us how his university is leading the way in microgrids and energy storage.

Byron Washom at the UCSD Microgrid.

UC San Diego is operating a campus microgrid containing a diverse array of technologies, including solar PV-powered EV charging stations, fuel cell storage, thermal storage for cooling, diesel backup generators, and a number of interesting experimental projects that reflect the university’s commitment to exploring the next wave of energy storage technologies.

The first thing that strikes you about UC San Diego is its size. Washom commented that serving the electrical needs of the campus is akin to serving a city of 90,000 people. This has provided both challenges and opportunities for the school.

Maxwell's 30kW solar-smoothing system

Washom has pioneered what he terms a “Motel 6” model for testing new energy storage systems. By laying the groundwork for a container-sized system in various locations on campus, he can carry out testing on whatever systems come his way. We saw a 30kW, 5-minute ultracapacitor installation by Maxwell, being used to smooth out fluctuations due to clouds in a solar PV array built on top of a university theatre. This system will be tested in conjunction with the university's solar forecasting system -- among the most advanced in the world.

BYD has also partnered with UC San Diego to provide a 2.5 MW / 5 MWh energy storage system located on campus. This is a big investment for a campus as large as a small city.

The school's microgrid not only serves the university, but has also helped the community of San Diego through a demand response partnership with the city’s utility, San Diego Gas & Electric. In a recent load event, the university activated its automation systems to adjust thermostats and other non-critical loads to transform the microgrid from an electricity importer into a 3 MW exporter. This 3 MW, Washom said, happened to be just enough to keep the grid up, clearly demonstrating how the right combination of technologies and practices are revolutionizing how utilities and consumers interact.

Keynote Addresses

In the evening, conference attendees met to listen to opening remarks from Janice Lin, conference organizer and founder of Strategen Consulting. She introduced James Avery, chief development officer of San Diego Gas & Electric, who argued that energy storage is the next big opportunity for cleantech players.

Taking a question from the audience about whether utilities had a role to play in the new world of distributed energy, Avery responded by pointing out that for California to reach its carbon emissions targets, the state will need to decarbonize – and thereby electrify – the entire transportation sector. With millions of electric vehicles needing to charge up, there will be a huge demand for electricity – both on a distributed and utility scale.

John Zaruhancik, the president of AES Energy Storage, spoke next. He announced a 20 MW storage project to be built in Dallas, in partnership with Oncor, a Texas utility.

He also talked about the broader meaning and importance of energy as a matter of human livelihood. AES Corporation, which operates the world’s largest fleet of grid-connected batteries, is active in countries which face energy insecurity and instability, such as the Philippines and the Dominican Republic. In his perspective, energy storage is another tool to make people’s lives better, by providing light to read, refrigeration for medicine, and the foundation for a modern economy.

“Clean, unbreakable power,” Zaruhancik said. “That’s what we really want.”

Our trip blog continues in part two for the first full day of presentations and coverage from the expo floor.

CNESA 2015 White Paper

Credit: Crew of ISS Expedition 23

CNESA has released its 2015 White Paper, an overview of the energy storage industry in China and abroad. The report explores trends from 2014 and looks at the newest technologies, concepts and markets shaping energy storage today.

Key topics include:

- The Future of Solar+Storage

- Chinese Energy Storage Policies

- Opportunities in the EV Industry

- China and the Energy Internet

- Outlooks for the Chinese Energy Storage Market

- The State of Energy Storage Technologies

We're happy to release this white paper for free. Our Chinese-language version, with greater detail and in-depth analysis, is available for purchase.

If you want to learn more about the Chinese energy storage market, contact us.

CNESA Demand Response Pilot Goes Online

Summer heat in Beijing. Credit: timquijano

On August 12th, 2015, the Beijing Demand Response Pilot program went online for the first time, as peak load in Beijing reached 18,430 megawatts – a new record. The round of demand response reduced load by about 70 megawatts, helping to ease pressure on the grid.

High summer temperatures led to another record-breaking load on the following day, reaching 18,560 gigawatts. To relieve grid stress, the Beijing Development and Reform Commission (BDRC) and the Beijing Energy Conservation and Environmental Protection Center (BEEC) issued an order to mobilize load integrators to begin reducing load. In the end, load was reduced by about 66 megawatts.

CNESA was the first organization to be recognized as a load integrator in Beijing, so when the dispatch order was given, we helped users engage in demand response. This instance of demand response came through the city’s Demand-Side Comprehensive Management Service Platform, which announced the response action in advance. Our load integration platform received the order and confirmed receipt. This instance demonstrated the capability of CNESA’s demand response platform to seamlessly receive top-down orders, and then divide responsibility and delegate to users. The system also successfully collected data and conducted analysis on user performance.

CNESA is working with the BDRC and BEEC to further improve this pilot program and make the most of our platform. We will learn from the experience of other integrators and improve the platform’s functionality to provide a convenient experience for a growing number of users. We’re also actively exploring how to establish long-term demand response mechanisms so that we can do our part in improving demand response in Beijing.

User demand curve shown on CNESA demand response platform interface

Beijing Demand Response Pilot Program

CNESA is helping the government achieve lower peak loads. Here's how.

Photo: robert anders

Since the promulgation of the Beijing Demand-side Management Pilot Program Financial Incentive Fund Management Guidelines in 2013, demand response programs have been subsidized by the Beijing Ministry of Finance. By the end of 2015, these programs are expected to bring about a total demand reduction of 150 MW from peak loads. The government has chosen to play a leading role in forming supporting pilot institutions that include both energy services companies and consumers.

Our Role

The Beijing development commission has entrusted CNESA to implement a demand response pilot program. As the first organization authorized to manage load integration, CNESA is responsible for developing a demand-side management platform and encouraging qualified consumers to participate. The Commission will provide subsidies to participating organizations.

CNESA has made progress towards achieving improved demand response by:

- Exploring the peak shifting potential among electricity consumers

- Guiding consumers on how to reduce consumption through behavioral changes

- Establishing a demand response platform

CNESA is currently in the process of attracting qualified consumers to join this DSM platform and creating a DSM data infrastructure to manage peak loads.

The demand response platform is critical to achieving demand-side management in the Chinese electricity market. It will help promote demand response across the grid and help establish DSM implementation mechanisms throughout the country. The platform will also demonstrate how consumers can benefit from the market by changing their usage behavior.

CNESA has partnered with ENERBOS, an energy software service provider, to design the platform’s back-end database and develop web applications to link with existing platforms (grid platforms, the CNESA network, and energy consumer platforms), and test functionality.

How it Works

The platform aggregates demand reduction goals from the grid dispatcher and publishes a reduction plan for consumers – including key information such as reduction amount, date and time, relevant areas, subsidy payments, etc. – so that consumers can decide how to reduce demand based on their capabilities and needs. The platform will then confirm which electricity providers and consumers will participate. The platform will monitor the load curve during implementation to evaluate participant performance and calculate subsidies. Lastly, the platform will use this data to guide and improve future actions.

CNESA has also developed a series of automated demand reduction packages to meet the needs of different consumers. This framework uses a distributed network to integrate different sub-systems into a single computerized and centralized structure, through which managers can quickly and conveniently monitor and control the network via a comprehensive graphical user interface. This platform improves grid stability and performance, all while bringing profit to participants.

Energy Storage China 2015 Held in Beijing

Over 700 participants joined CNESA for our 4th annual conference and expo.

On June 3, 2015, CNESA and Messe Dusseldorf held their 4th annual summit — Energy Storage China 2015 — in Beijing, with the support of the National Energy Administration. The event took place over four days, with the theme of “Driving Energy Storage Commercialization: Policy, Technology, and Financial Innovation.” The summit featured discussions on many energy storage applications, proposed future directions for industry development, and broadened commercial possibilities for energy storage.

Global energy storage market steadily advances

As the global new energy industry has developed, renewable energy is gradually moving from a supplementary role towards large-scale substitution of tradition energy. Energy storage technology's role in integrating renewable energy into the grid has gradually emerged, and industry insiders expect the global ES market to exhibit explosive growth.

According to CNESA's database, at the end of 2014 the global grid-connected installed capacity of energy storage was 845.3 MW (not including pumped hydro, CAES or thermal storage). 111.6 MW was installed in 2014, an increase of 15% from the year before. The annual growth rate is also 2% higher in comparison to 2013. China has 84.4 MW of installed capacity, about 10% of the global total.

The US has the largest number of projects and installed capacity. By year's end 2014, the US had commissioned 95 energy storage projects, with installed capacity exceeding 357 MW. Japan is second in installed capacity with 310 MW, and China second in number of projects with 63. In 2014, the US installed the most new capacity, 34.4 MW, with China and Europe following with 31 MW and 27.7 MW respectively.

In terms of technology, sodium sulfur batteries make up the largest share with 40%, followed by lithium ion and lead-acid batteries with 33% and 11% respectively. But, for new capacity in 2014, lithium ion batteries made up 71%, followed by flywheels with 20%.

In application, most energy storage is installed on the grid side for connection of renewables, ancillary services, transmission and distribution, and distributed microgrids. Grid connection of renewables makes up 45%, or 379 MW. In 2014, user-side applications made up 43% of new installations, with ancillary services and T&D following at 28% and 19%.

In investment news, 12 major companies raised over US$400M in energy storage finance in 2014 to fund technology R&D, project installations, market expansion, and deployments. In particular, investors seemed to favor enterprises with more innovative technologies and business models, such as Stem and Aquion Energy.

Rapid development in China’s energy storage industry

While the global ES market is developing at a steady pace, China's storage industry is seeing rapid changes. In March 2015, the CCP Central Committee and the State Council issued long-awaited electricity system reforms, which are already showing positive effects on the clean energy and advanced energy storage industries. This is good news for industry-watchers, who have been awaiting policies introducing market mechanisms into China’s heavily regulated electricity system.

At ESC 2015, CNESA Secretary Tina Jing Zhang announced that, according to CNESA’s database, China had 84.4 MW of ES installed capacity on the grid by the end of 2014 (not including pumped hydro, CAES or thermal storage). This is an increase of 31 MW in a single year—a growth rate of 58%. This is a substantial jump in deployment compared to years past, where 2013 saw only 14% annual growth.

Lithium ion batteries make up 74% of China's installed ES capacity, followed by lead acid batteries and sodium sulfur batteries at 14% and 10%. These three technologies make up about 98% of China's market.

In terms of application, user-side applications account for most of China's market, about 50%, which includes islands, remote areas, industrial parks, and low-carbon city installations. Renewable energy grid integration and electric vehicles make up the second and third largest applications, at 27% and 13%, with most of the former being in wind farm energy storage, and most of the latter being in solar+storage EV charging stations, V2G (vehicle to grid) applications, demand response charging, and second-life EV battery usage.

World-Class Experts Convene at ESC 2015

This year’s conference received support from the German Energy Storage Alliance (BVES), the California Energy Storage Alliance (CESA), the India Energy Storage Alliance (IESA), and the Global Energy Storage Alliance (GESA). Through their support, we were able to host experts from across the world to share their views on the development of the industry.

In the opening ceremony, we were joined by top representatives from government and industry, including: Mr. Shi Dinghuan, chairman of the China Renewable Energy Society and member of the China Energy Storage Expert Committee; Mr. Xu Dingming, advisor to the State Council; Ms. Zhang Yulei, director of the Zhongguancun Industry Office; and Mr. Johnson Yu, chairman of CNESA.

In the following speeches, Ms. Lu Hong of the Energy Foundation China’s Renewable Energy Project shared the findings of a new report, the “China 2050 High Renewable Energy Penetration Study.” Dr. Eicke R. Weber, founding president of BVES and director of the Fraunhofer Institute for Solar Energy Systems, described the rise of Industry 4.0 in Germany, as well as the challenges and opportunities in the energy storage industry today. Darren Gladman, policy manager at the Australia-based Clean Energy Council, presented on industry trends and opportunities in the Australian market. Our speakers also included Rebecca Feuerlicht, project manager for the Center for Sustainable Energy, who shared her insights on California’s Self-Generation Incentive Program (SGIP).

To examine different applications of energy storage technology in depth, participants engaged in smaller seminars on the following topics:

- “China’s Electricity Reforms and Energy Storage Opportunities” – Prof. Zeng Ming, director of the Energy and Electricity Economics Center at the North China Electric Power University, explained the details of China’s new electricity reforms. Mr. QIN Yi, director of the Shenzhen Micro-grid Management System Engineering Laboratory, also shared his insights into the pilot pricing reforms for the transmission grid.

- “Developments in the International Energy Storage Market” – Speakers from around the globe presented on energy storage trends in Australia, Germany, Canada, the EU, India, Japan, and China, then followed up with questions on energy storage business models.

- “Electric Vehicles and Storage” – Mr. Wang Zizhong, director of the dynamics lab at the China North Vehicle Research Institute, proposed suggestions on the future direction of EV batteries. Meanwhile, industry leaders and academics shared their experiences with EV charging and operation models.

- “Advanced Energy Storage” – Experts presented on traditional technologies such as physical, electrochemical, and phase change storage methods as well as emerging technologies like aqueous sodium ion and solid-state lithium batteries.

- “Solar PV plus Storage” – Mr. Wang Sicheng of the National Development and Reform Commission’s Energy Research Institute explained the importance of energy storage as a part of solar deployment. Representatives from the US, Australia, Japan, and China, shared case studies on distributed storage and analyzed financing methods and business models.

Additionally, CNESA released the industry’s top annual report, its 2015 Energy Storage Industry White Paper. The report examines international projects and policies, especially focusing on solar-powered EV charging models and the state of new energy finance. The paper looks at “solar-plus-storage” as a potential model for microgrids, as well as the opportunities that EV battery development is bringing to the industry as a whole. The report also takes a close look at the concept of the “internet of energy.” CNESA hopes that the results of our white paper – along with the hard work of industry members and better business models – will help spur continued development in the Chinese energy storage industry.

This year’s conference drew over 700 participants and 80 speakers from 10 countries. The event was a great chance for sponsors, exhibitors, and other participants to connect with policymakers, grid representatives, integrators, and foreign utilities. Participants learned about the newest global trends, policies, technologies, and business models. By making these connections, participants met new customers and positioned themselves for another successful year.

China's New Electric System Reforms

Credit: Steffen Ramsaler / Flickr

Beginning in March 2015, following years of silence in electric system reforms, China has introduced new policies and documents reforming its electricity generation, retail, usage, and many other sectors.

The leading policy document, Several Opinions of the CPC Central Committee and the State Council on Further Deepening the Reform of the Electric Power System – also known as Policy No. 9 – have established a new framework which officials are referring to as “pipeline in the middle, open at both ends.” China is putting forth a series of reforms in electricity pricing, distribution and retail segments, electricity trading, distributed generation, and other aspects. Combined with the set of policies that followed, we expect that this round of electric system reforms will have a profound impact on China's electricity markets and industries.

(1) Changes to T&D pricing and grid operation models

New electric system reform policies. Source: CNESA

Policy No. 9 separates T&D and retail, establishes a principle of “approved costs plus reasonable profit,” and differentiates T&D prices based on voltage level . The policy also breaks up China's long‐standing model that integrates transmission, distribution, and retail in a single entity. It also puts a stop to practices where grid operators can profit from differences between generation and retail prices. The role of the grid will shift from that of an electricity trading body towards an electricity transmission provider, in which the grid will earn profits through a “toll” in exchange for services.

Before the issuance of Policy No. 9, Shenzhen and Inner Mongolia were T&D reform pilot regions. Another policy document emerging in the wake of Policy No. 9, Notice on Hastening Implementation of Policy No. 9-related Transmission and Distribution Reforms, will expand the pilot program to include Anhui, Hubei, Ningxia, and Yunnan, bringing the number of pilots up to six. We expect that this number will continue to grow.

Following the beginning of Shenzhen's T&D pricing pilot, electricity prices have dropped. From 2015 to 2017, Shenzhen's T&D prices will drop year-by-year: ¥0.1435, ¥0.1433 and ¥0.1428 per kWh, respectively. This is more than ¥0.01 less than 2014 levels. Electricity customers are already realizing the benefits of reform.

The changing role of the grid operator and a clarified T&D price will:

Create flexible electricity trading models

Introduce competitive pricing on the generation and retail sides

Promote the entrance of diverse participants into the electricity market

Improve utilization and efficiency of the entire electricity system

(2) Reforms to price-setting, and the formation of market trading mechanisms

Policy No. 9 clarifies that outside of T&D pricing and public welfare electric pricing, generation and retail prices will be determined by the market. Generators can determine prices through agreements with large users or retailers, or through market competition. In addition, during the process of reform, differences in electricity subsidies among different users will gradually undergo reform.

3) Generation and retail side competition, and a diversity of retail entities

In addition to prices being set by the market, Policy No. 9 shows that following the elimination of public welfare generation and use planning, generation-side generation planning and retail-side electricity usage planning will also be determined more and more by the market. Generation-side and retail-side competition will become much more intense. As private funding of retailers liberalizes, there will be more pathways to breed market entities.

In the new system, high-tech industrial parks and economic zones, privately-funded retailers, utilities such as water, gas, and heat providers, energy service companies, qualified generation companies, microgrid operators/owners, and others can all take part and fight it out in the future retail market.

Before Policy No. 9, Shenzhen's T&D price reform, the first of such reform pilots, had already been active in this respect. On March 24, 2015, Shenzhen's first privately operated retail electric company, Shenzhen Electric Power Retail Co. Ltd. (Shenzhen Dianneng Shoudian Co. Ltd.), officially received its industry and commerce permit. It is also China's first privately-owned retail electric company. Whether more of these companies will appear is a matter that will be watched closely.

(4) New ancillary services market

China's ancillary services have long been provided by grid‐connected power plants, without any ancillary service market. This will change with Policy No. 9.

Policy No. 9 establishes a new “shared responsibility” mechanism for ancillary services. This improves the compensation mechanism for ancillary services provided by grid‐connected power plants. It will use a “those who undertake are those who benefit” principle. It also establishes "shared responsibility, shared gains" mechanisms for user participation in ancillary services. Users, in accordance with their contracts with either generator companies or the grid, can be responsible for a required ancillary service fee, or some other type of economic compensation.

Another new policy document, Guiding Opinions on Improving Electric Operation and Regulation to Promote Greater and Fuller Use of Clean Energy (hereafter referred to as Opinions on Clean Energy), was drafted to promote renewable energy consumption. It also reemphasized the importance of ancillary services, and stressed the establishment and improvement of related mechanisms. These include peak shifting compensation mechanisms, incentivizing the direct purchase of clean energy ancillary services, and advancing the development of electric ancillary services.

(5) Demand side management and new electric service companies

One of the highlights of this electric reform is the simultaneous reform of electricity production and consumption. Policy No. 9 emphasizes demand side management in balancing the grid. The Notice on Perfecting Electric Emergency Mechanisms to Conduct City Pilot Demand Side Management emphasized the need to establish time-of-use pricing, incent the participation of private electricity service companies, and establish online electricity usage monitoring platforms to promote demand side management efforts.

Opinions on Clean Energy, from the angle of renewable energy consumption, also emphasized the importance of demand side management, increased time-of-use price spreads, comprehensive operation and usage subsidy policies, incentives for user participation in peak shifting and frequency regulation, and the establishment of demand side management platforms.

User usage behavior has a large impact on the overall efficiency of the electric system. Through demand side management and demand response, user load can become a dispatchable resource with a certain degree of flexibility. This can lower peak loads and play an important role in providing the grid with peak shifting and ancillary services.

(6) Gradual transition from fossil fuels to renewables, and the creation of distributed energy markets

Opinions on Clean Energy further promotes the usage and consumption of renewable energy after the release of Policy No. 9. Key methods included in the document for advancing renewable energy consumption include comprehensive overall planning for annual electric balancing, strengthening of daily operation regulations, sufficient ancillary services and other benefit compensation mechanisms, and strengthening of demand side management.

Of particular importance, Policy No. 9 emphasizes the establishment of new distributed energy development mechanisms, as well as the complete opening of user-side distributed energy markets. In reality, since the 2013 issuance of the NDRC Notice on Implementing Price Leveraging to Promote the Healthy Development of the Solar PV Industry, which established a ¥0.42/kWh subsidy for power provided by distributed solar PV, many localities launched their own local subsidy plans. However, distributed PV development has not completely been taken up. In 2014, only about 2.52 GW of distributed PV was installed, well short of the 6 GW target.

In the other reforms under Policy No. 9, distributed energy can now become a resource for regional retail companies via usage by specialized ESCOs, in addition to existing models such self‐consumption, grid feed-in, or grid dispatch.

Moreover, distributed energy, especially distributed PV, can work with energy storage and other devices to participate in demand side management, broadening the value of distributed energy. The distributed energy market can likely bring great development opportunities.

Energy storage is a flexible power resource, and has already proven many applications at all levels of the grid from generation down to the user. However, a great many bottlenecks continue to hamper widespread application. Outside of technological performance and cost factors, in China, the lack of appropriate mechanisms for market participation has been a major reason for the slow development of energy storage.

The new reforms will open up Chinese electricity markets such as demand response, ancillary services, and distributed energy, within all of which energy storage can play a major role.

Archive

SUBSCRIBE

Sign up for our free monthly newsletter to stay informed about the Chinese energy storage market.

Quisque iaculis facilisis lacinia. Mauris euismod pellentesque tellus sit amet mollis.