Latest News

New Installations Surge Over 120% YoY — February Analysis of China’s New Energy Storage Projects

In February 2026, China’s new energy storage market sustained its rapid growth momentum, with newly installed capacity increasing by over 120% year-on-year (YoY). Meanwhile, the application structure of the market has undergone adjustments compared with the same period last year.

In February 2026, China’s new energy storage market sustained its rapid growth momentum, with newly installed capacity increasing by over 120% year-on-year (YoY). Meanwhile, the application structure of the market has undergone adjustments compared with the same period last year.

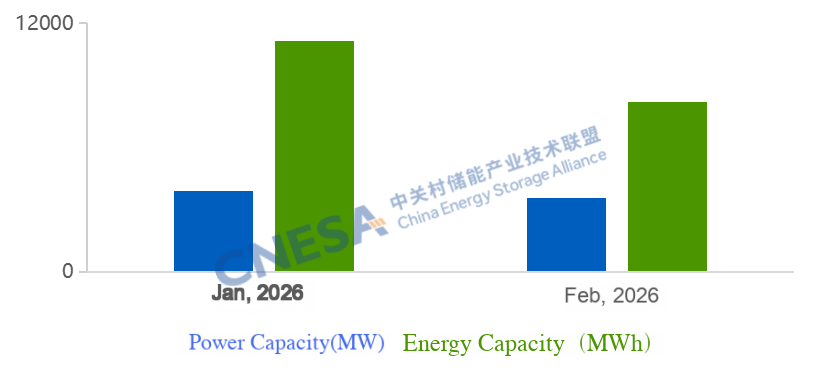

Short-term fluctuations do not alter long-term growth trend: In February, newly installed capacity reached 3.6 GW, representing a YoY increase of over 120% and a month-on-month (MoM) decline of 31%. Despite the short-term slowdown, the long-term growth trajectory of the energy storage market remains strong.

Front-of-the-meter standalone storage drives growth: Standalone energy storage on the generation and grid side became the primary growth driver. In February, standalone storage accounted for 90% of newly added capacity, up 42 percentage points YoY. Newly installed power and energy capacity of standalone storage increased by more than 310% and 270% YoY, respectively.

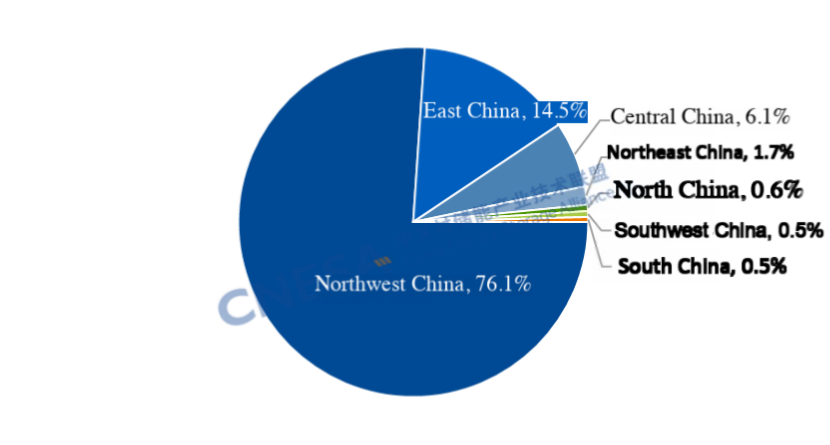

Highly concentrated regional deployment: The Northwest region accounted for over 75% of total additions, with Ningxia alone exceeding 2 GW, contributing more than 60% of the national total.

According to incomplete statistics from China Energy Storage Alliance(CNESA), China commissioned 3.56 GW / 8.19 GWh of new energy storage capacity in February 2026, representing YoY increases of +120% / +95% and MoM declines of -31% / -21%.

The MoM decline was mainly due to project construction cycles and the impact of the Spring Festival holiday. However, the YoY growth exceeding 120% indicates a fundamentally positive market outlook. Notably, front-of-the-meter (FTM) installations reached 3.4 GW, up 147% YoY, effectively doubling the total monthly additions.

Key Market Characteristics in February

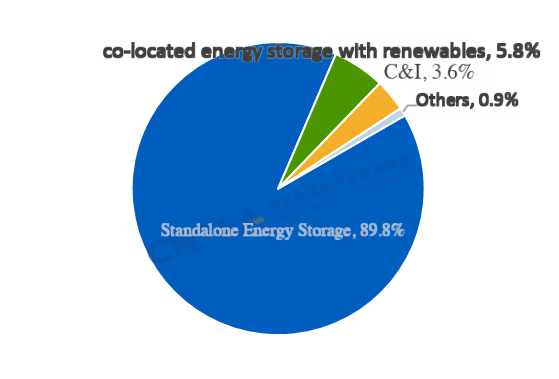

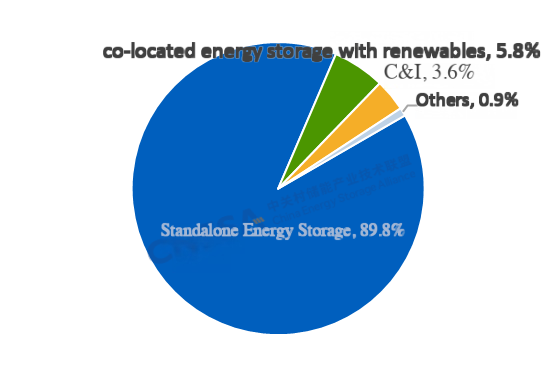

1. Standalone Storage Surges Over 270%, Driving Market Expansion

In terms of application structure, standalone energy storage dominated the market. It accounted for 90% of total newly installed power capacity, up 42 percentage points YoY and 8 percentage points MoM. Newly added capacity reached 3.2 GW / 7.4 GWh, with YoY growth of +313% / +274%, becoming the main driving point of energy storage market. All newly commissioned standalone energy storage projects reached at least the 100 MW level, with the number of such projects rising by 29% year-on-year, alongside the commissioning of two gigawatt-scale projects.

Installations on the generation side and behind-the-meter (BTM) user side experienced a temporary decline. Newly installed capacity on the generation side reached 217.3 MW / 474.3 MWh, down 65% / 72% year-on-year and 41% / 36% month-on-month. Co-located storage with renewable energy remained the dominant model, covering a range of application scenarios such as aquaculture, solar hybrid projects and desertification control initiatives.

New user-side installations totaled 135.2 MW / 292.7 MWh, down 41% / 42% year-on-year and 51% / 58% month-on-month. The market was highly concentrated, with Jiangsu, Guangdong, and Zhejiang accounting for 90% of total user-side energy storage capacity, while Jiangsu ranked first nationwide in both installed capacity and project count.

On the technology front, lithium-ion batteries continued to scale rapidly, supporting the commissioning of gigawatt-level standalone storage plants. Meanwhile, hybrid systems combining lithium-ion and sodium-ion batteries at the 100 MW level were deployed, and aqueous organic flow batteries were implemented on the user side, providing more diversified technological pathways for long-term development.

2. Regional Concentration Intensifies, Northwest China Dominates

In February, regional concentration of new installations was pronounced. The Northwest region added 2.7 GW, accounting for 76% of the national total. The combined share of the Northwest and North China regions exceeded 90%. Ningxia added 2.2 GW / 4.4 GWh of new capacity, ranking first nationwide in both power and energy scale and setting a new monthly record for the region. This surge was driven by the grid connection of several gigawatt-scale shared energy storage projects and storage systems paired with large renewable energy bases.

By the end of 2025, Ningxia’s renewable energy capacity reached 57.32 GW, accounting for 65.5% of total grid capacity under centralized dispatch. Solar power has surpassed coal-fired generation to become the largest power source in the region. Due to the intermittency of renewables—characterized by surplus generation during the day and shortages at night—demand for grid services such as peak shaving and frequency regulation has surged. A coordinated development model integrating wind, solar, thermal power, and energy storage is rapidly taking shape. Looking ahead, energy storage is expected to generate revenue through multiple channels, including capacity compensation, spot market trading, frequency regulation services, ramp rate support and so on.

In addition, Ningxia has introduced policies encouraging private capital participation in energy storage investment. In February, a gigawatt-scale storage project developed by Jiayang Energy was commissioned, demonstrating strong investor confidence in the region. At the end of February, the region released its first batch of 2026 private investment promotion projects, including 22 energy storage projects with a total scale of 4.15 GW / 14.4 GWh, providing a solid pipeline for continued market growth.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

Sharp Pullback! User-Side Energy Storage Additions in January Down 58% Year-on-Year

In January 2026, China’s user-side new energy storage market recorded a year-on-year decline of more than 50% in newly added capacity. The pace of project filings slowed while quality improved, and market deployment shifted toward larger single projects and more capital-intensive investments.

In January 2026, China’s user-side new energy storage market recorded a year-on-year decline of more than 50% in newly added capacity. The pace of project filings slowed while quality improved, and market deployment shifted toward larger single projects and more capital-intensive investments.

The user-side energy storage market experienced a clear correction, with installed capacity down 58% year-on-year. Commercial and industrial (C&I) energy storage accounted for more than 90% of total additions.

The East China region contributed over three-quarters of newly commissioned capacity. Jiangsu led the nation, accounting for 60% of total installed capacity.

Nationwide, the number of newly filed user-side projects fell by 38% year-on-year, while the average size of individual projects increased by 87%. Core markets—Jiangsu, Guangdong, and Zhejiang—continued to lead, as user-side deployment shifted from small, distributed projects toward larger-scale, more centralized investments.

Analysis of User-Side New Energy Storage Projects in January

In January, newly commissioned user-side energy storage capacity totaled 166.2 MW / 456.5 MWh, representing -58% / -39% year-on-year and -81% / -73% month-on-month. The following characteristics were observed.

(1) Installed capacity of user-side energy storage

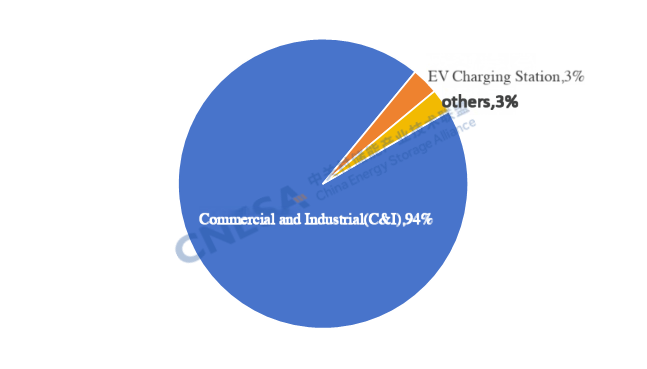

In January, the market remained dominated by C&I applications, accounting for over 90% of total additions. Newly commissioned C&I projects reached 156.7 MW / 435.4 MWh, down 60% / 41% year-on-year and 82% / 74% month-on-month.

From a technology perspective, all newly commissioned projects adopted electrochemical energy storage. Lithium iron phosphate (LFP) batteries accounted for more than 99% of installed power capacity. In the long-duration energy storage, one 7-hour photovoltaic-plus-storage integrated smart power station project and one 4-hour solid-state lead battery energy storage project were commissioned.

Figure 1. Application distribution of newly commissioned user-side new energy storage projects in January 2026 (MW %)

Source: CNESA DataLink

Note: “C&I” includes industrial facilities, industrial parks, and commercial buildings; “Others” include mining areas, oilfields, rail transit, data centers, etc.

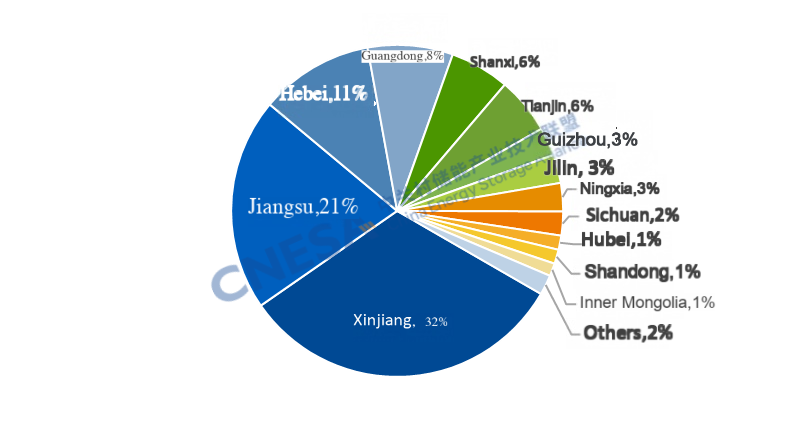

(2) Regional Distribution of User-Side Energy Storage

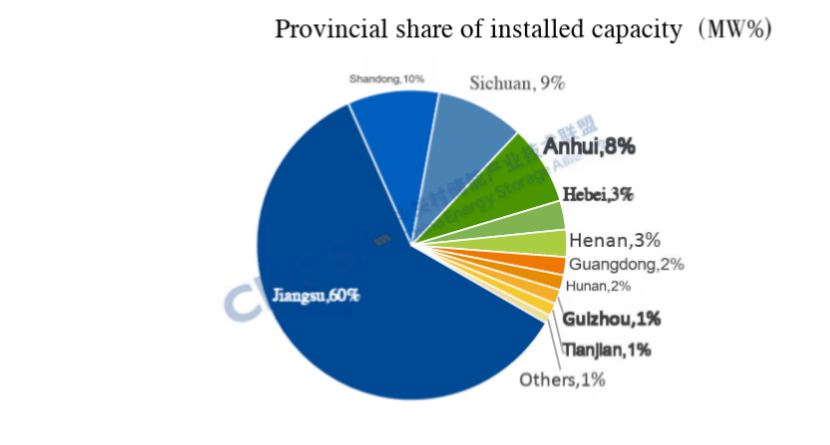

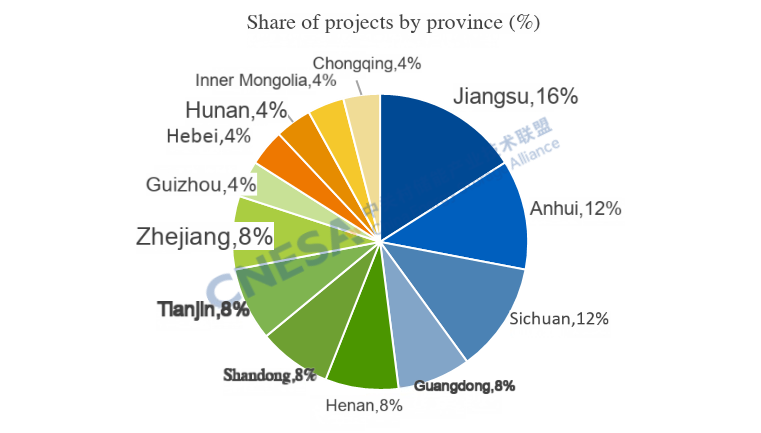

By region, newly commissioned projects were distributed across 13 provinces, including Jiangsu, Anhui, Shandong, Sichuan, and Guangdong. East China dominated the January market, accounting for 78% of newly added capacity and 44% of total project numbers.

At the provincial level, Jiangsu ranked first nationwide, contributing 60% of total installed power capacity and 16% of newly commissioned projects. Both installed capacity and project count ranked first nationally. This performance was driven by a combination of power market reforms, demand response incentives, strong C&I demand, and the centralized grid connection of large-scale projects.

On the policy front, multiple supportive measures were introduced, accelerating the transition of user-side energy storage business models from “fixed arbitrage” to “volatility-driven optimization.” In January, Jiangsu implemented new power market reforms, with the Jiangsu Energy Regulatory Office releasing the Implementation Rules for the Jiangsu Medium- and Long-Term Power Market (Draft for Comments). These rules marked a shift in C&I electricity pricing from fixed time-of-use tariffs to fully market-based pricing. In the short term, this reduced fixed peak–valley arbitrage margins; however, in the medium to long term, more frequent price fluctuations are expected to create diversified arbitrage opportunities for projects with advanced forecasting and intelligent dispatch capabilities. In addition, as of January 1, 2026, Jiangsu officially implemented full market participation for all renewable electricity, making photovoltaic-plus-storage integration a necessity for smoothing output profiles and enhancing market-based revenues. During the critical winter peak demand period, user-side storage projects could also participate in demand response programs, earning peak-shaving compensation of up to RMB 4.8/kWh, significantly improving short-term revenue certainty and incentivizing projects to connect to the grid within the policy window.

On the demand side, structural factors continued to underpin market growth. January marked the winter peak electricity demand season in Jiangsu. On January 20, the province’s maximum load reached 135 GW, a new winter record and the highest nationwide for six consecutive years. Grid balancing and supply security pressures highlighted the system value of user-side storage. As a major manufacturing province with a high concentration of energy-intensive industries, Jiangsu faces strong demand for peak shaving, valley filling, and demand charge optimization. In January, peak–valley price spreads remained above RMB 0.6/kWh, supporting stable combined returns from energy arbitrage and demand management. Moreover, Jiangsu’s large installed base of distributed photovoltaics further amplified demand for storage, as pairing PV with storage under full market participation policies enables off-peak discharge and enhances project economics.

From a market structure perspective, growth in Jiangsu exhibited clear characteristics of scale and concentration. In January, several large projects—such as the 300 MWh user-side energy storage project of Jiangsu Huiran Industrial Co., Ltd.—along with multiple projects exceeding 5 MW / 40 MWh, were commissioned. Large-capacity projects accounted for the majority of additions, reinforcing Jiangsu’s “fewer projects, higher capacity” market profile. In addition, Jiangsu benefits from a well-developed local energy storage industrial chain. Through full-chain coordination, economies of scale, resource sharing, technology reuse, and business model innovation, system-level costs—including initial investment, operations, and lifecycle costs—can be significantly reduced, providing a strong industrial foundation for continued user-side market growth.

Figure 2. Provincial distribution of newly commissioned user-side new energy storage projects in January 2026

Source: CNESA DataLink

(3) Project Filings

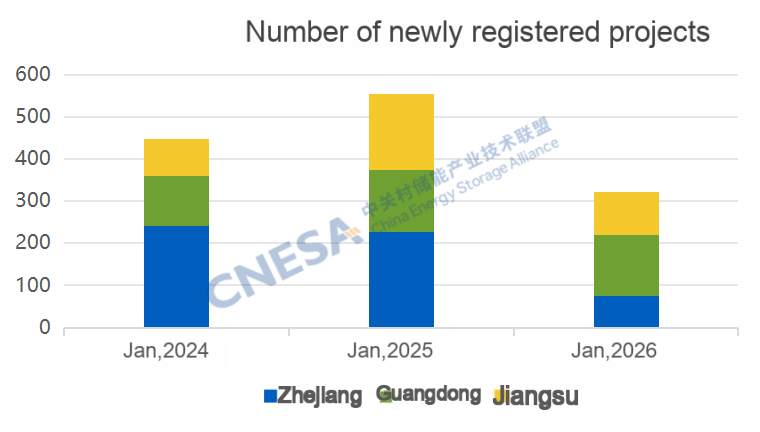

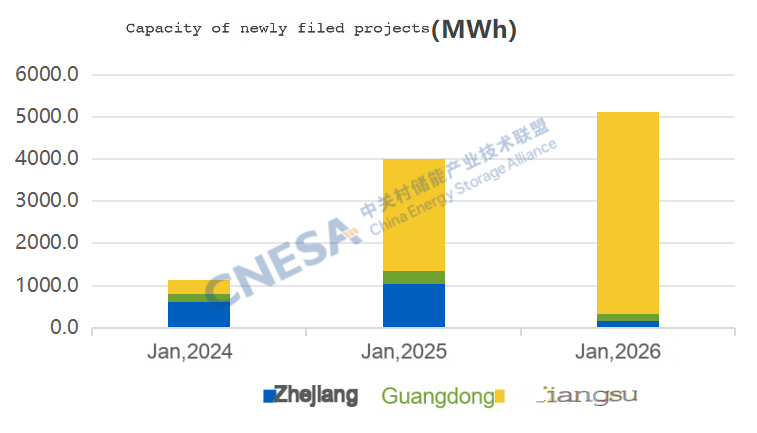

From the perspective of project filings, January saw a “less but better” trend nationwide. The user-side market shifted from distributed expansion to scale and centralized development. The number of newly filed user-side projects fell by 38% year-on-year, while total filed capacity increased by 16%, and the average project size of single projects rose by 87%. In traditional markets, Jiangsu, Guangdong, and Zhejiang together added 321 new projects, down 42% year-on-year, while total energy capacity increased by 28%. Jiangsu recorded the largest total filed capacity, while Guangdong led in the number of newly filed projects. Over the past three years, Jiangsu has consistently seen year-on-year growth in both total filed capacity and average project size in January. This January, Jiangsu’s newly filed capacity rose 81% year-on-year, while project numbers declined 44%, resulting in an average project size roughly three times that of the same period last year—highlighting a clear trend toward larger individual projects. By contrast, Zhejiang continued to see declines in newly filed projects. In January, the number of projects fell 67% year-on-year, and total capacity declined 86%.

Figure 4. Newly filed energy storage projects in Zhejiang, Guangdong, and Jiangsu in January over the past three years

Source: CNESA DataLink

Overall Analysis of New Energy Storage Projects in January

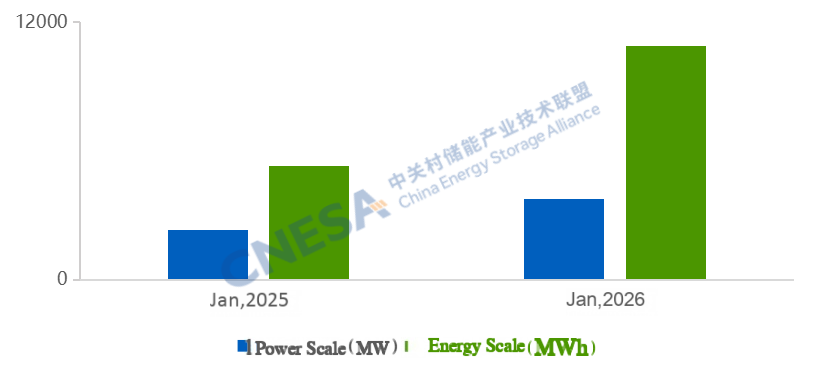

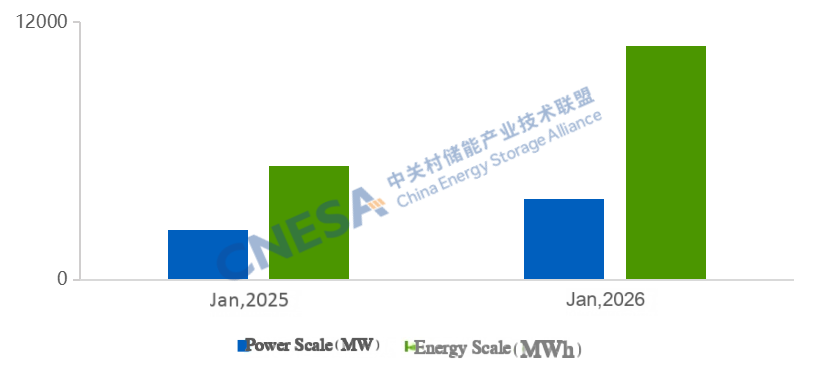

According to incomplete statistics from China Energy Storage Alliance (CNESA), total newly commissioned new energy storage capacity in China reached 3.78 GW / 10.90 GWh in January 2026, representing +62% / +106% year-on-year, but -84% / -86% month-on-month. Despite the sequential decline, year-on-year growth exceeded 60%, signaling a positive start to the year for the new energy storage market.

Figure 5. Newly commissioned new energy storage capacity in China in January 2026

Source: CNESA DataLink

Note: Year-on-year comparisons are based on the same period of the previous year; month-on-month comparisons are based on the immediately preceding period.

China Energy Storage Alliance adheres to standardized, timely, and comprehensive data collection methodologies to continuously track energy storage project developments. Leveraging long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses to support industry decision-making. Since June 2025, the Alliance’s monthly project analysis has been divided into two dedicated reports—Source-Grid-Side Market and User-Side Market. This issue focuses on the user-side market in January 2026.

For more comprehensive project information, authoritative data, and in-depth market insights, please visit www.esresearch.com.cn or access the CNESA DataLink mini program to explore detailed datasets and research reports. Customized data consulting services are also available through CNESA’s official support channels. CNESA is committed to providing full-cycle, high-quality data services for the industry.

At this critical juncture of diversified business model transformation for user-side energy storage, the ESIE 2026 will bring together leading enterprises from across the industry. The event will feature major launches of new C&I and residential storage products, alongside a series of high-level forums, including:Energy Storage Applications in Zero-Carbon Industrial Parks; Energy Storage + AIDC Collaborative Development;Energy Storage and Emerging Business Models;Distributed PV-plus-Storage;PV–Storage–Charging Integration;Overseas Energy Storage Project Development, Operation, and Practice;The Role and Value of Energy Storage in Virtual Power Plants.These sessions will provide in-depth analysis of market shifts and offer a one-stop platform spanning product showcases, operational best practices, and ecosystem collaboration. We cordially invite you to attend and explore pathways to breakthrough and growth in the evolving user-side energy storage landscape.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

10.9 GWh! Newly Added New-Type Energy Storage Capacity in January Doubled Year-on-Year

China’s new-type energy storage market witnessed a strong start in January 2026. Newly commissioned capacity in January increased by over 60% year-on-year, while the market’s underlying structure showed notable adjustments compared with the same period last year.

China’s new-type energy storage market witnessed a strong start in January 2026. Newly commissioned capacity in January increased by over 60% year-on-year, while the market’s underlying structure showed notable adjustments compared with the same period last year.

A Strong Start to the Year: Newly added capacity: 3.8 GW / 10.9 GWh in January, representing a

year-on-year increase of 62% / 106%, marking a positive opening for the new-type energy storage

market.

Accelerated Deployment of Independent Energy Storage: In January, independent energy

storage accounted for nearly 90% of newly added capacity, up 41 percentage points year-on-

year. Newly added power and energy capacity of independent energy storage grew by over 240% /

290% year-on-year. Xinjiang ranked first nationwide in both power and energy capacity, with 1 GW

of newly commissioned independent energy storage.

Rise of Third-Party Enterprises: Third-party enterprises accounted for 45% of newly added

installed capacity, once again surpassing local energy groups and the “Big Five and Small Six”

state-owned power generation groups. The trend toward a diversified investment landscape has

become increasingly evident.

Accelerated Deployment of Diverse Technologies: Beyond mainstream lithium-ion batteries,

alternative technologies such as compressed air energy storage (CAES), flow batteries, and

flywheels are being deployed at a faster pace, supporting the industry’s long-term development.

Overall Analysis of New-Type Energy Storage Projects in January

According to incomplete statistics from the CNESA DataLink, in January 2026, newly commissioned new-type energy storage projects in China reached a total installed capacity of 3.78 GW / 10.90 GWh, representing year-on-year increases of 62% and 106%, respectively, and month-on-month declines of 84% and 86%. Monthly new added capacity growth exceeded 60% year-on-year, underscoring a positive market outlook at the beginning of the year.

Figure 1: Installed Capacity of Newly Commissioned New-Type Energy Storage Projects in China, January 2026

Source: CNESA DataLink

Note: Year-on-year (YoY) comparisons are based on the same period of the previous year; month-on-month (MoM) comparisons are based on the immediately preceding statistical period.

Analysis of Generation- and Grid-Side New-Type Energy Storage Projects in January

In January, newly added generation- and grid-side new-type energy storage capacity reached 3.62 GW / 10.44 GWh, up 87% / 130% year-on-year, and down 84% / 87% month-on-month. Key characteristics include:

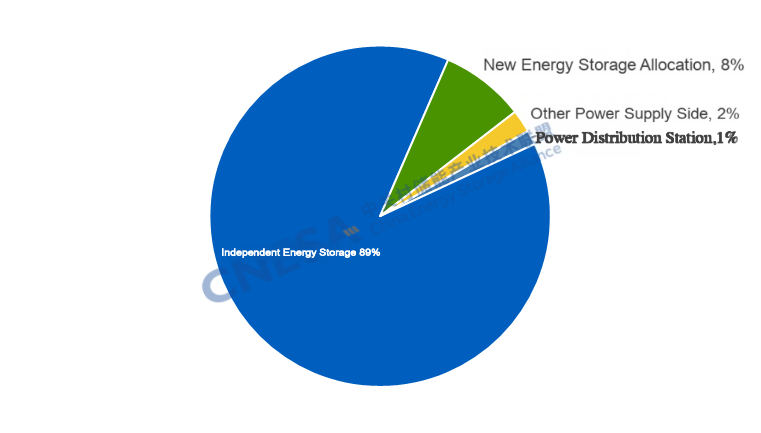

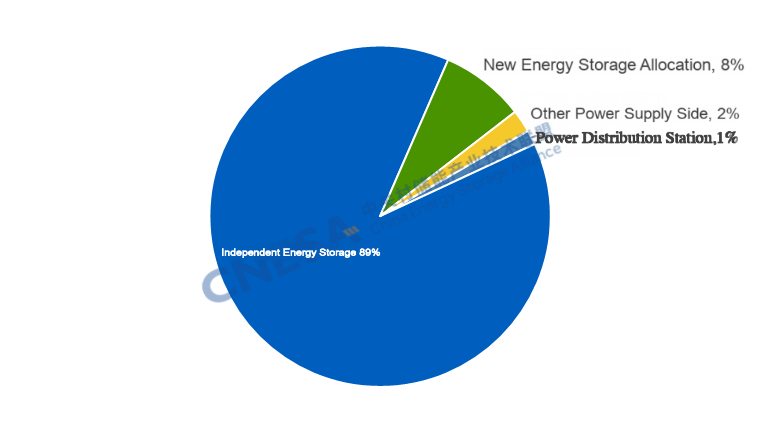

1.Independent energy storage accounted for 89% of new installations, up 41 percentage

points year-on-year and 12 percentage points month-on-month.

Newly added independent energy storage reached 3.2 GW / 9.6 GWh, up 249% / 298% year-on-year, and down 84%/87% month-on-month. The number of projects with capacities of 100 MW and above increased by 122% year-on-year, accounting for 85% of total projects—29 percentage points higher than the same period last year. By contrast, power-generation-side new-type energy storage additions were 366.5 MW / 740.3 MWh, down 64% / 65% year-on-year and 92% / 95% month-on-month. Among these, renewable-plus-storage projects accounted for 79% of power capacity, spanning diversified application scenarios such as desertification control, thermal–renewable–storage multi-energy integration, and hydro–solar–pumped storage integration.

Figure 2: Application Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

Note: “Others” include substations, emergency power supplies, etc.

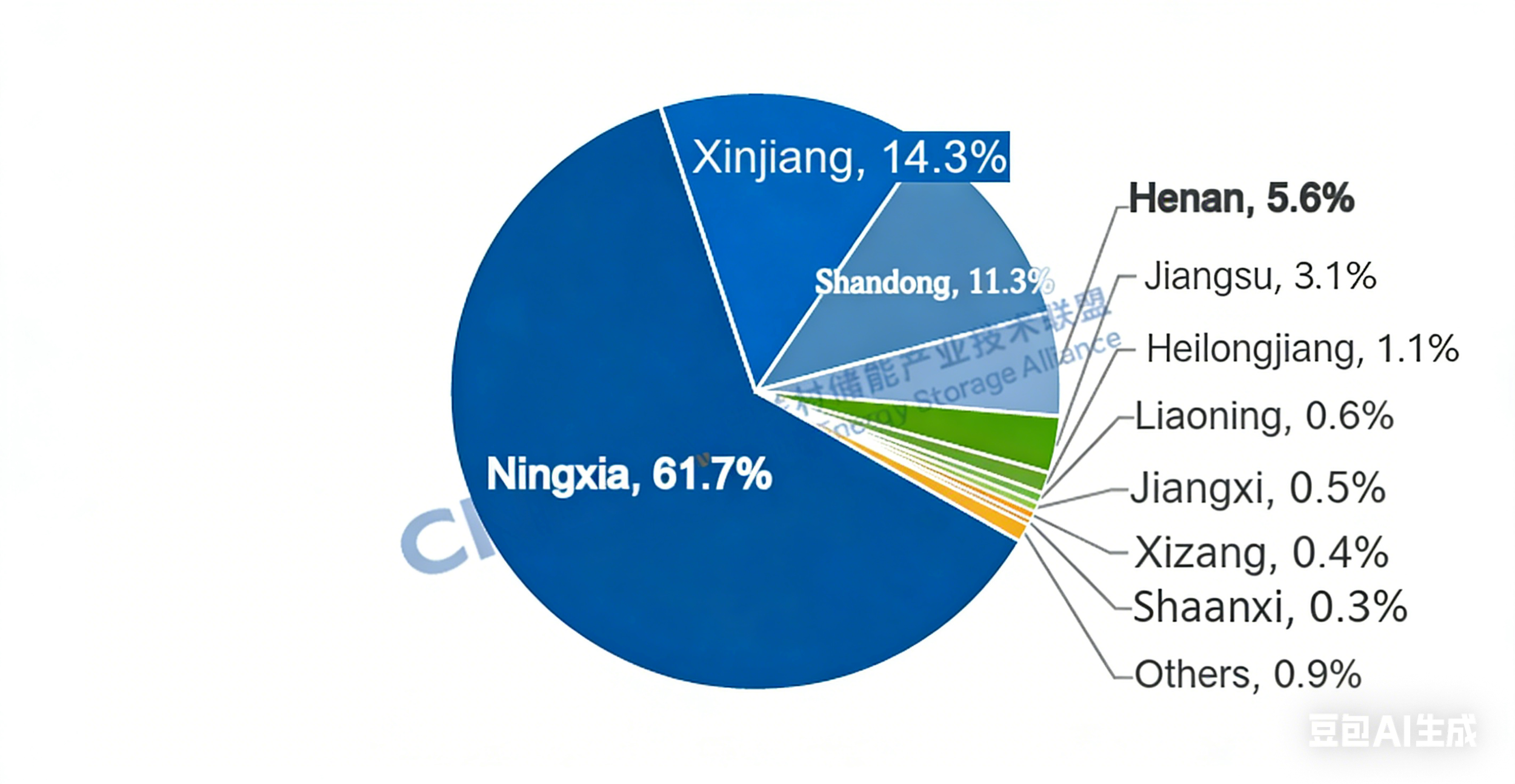

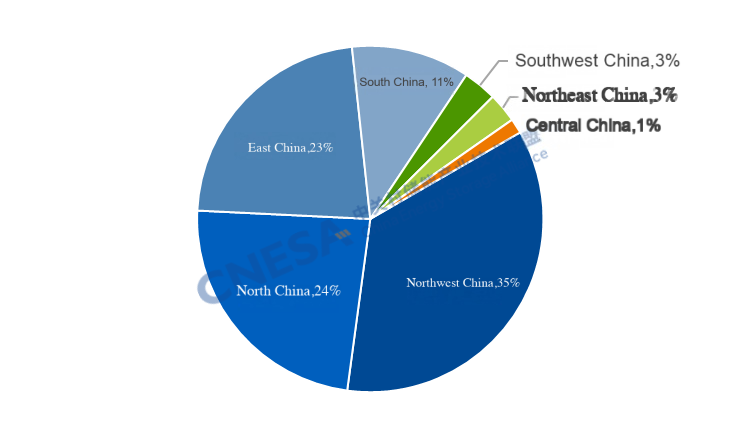

2. Northwest China Accounted for Over 35% of New Capacity, with Xinjiang Leading

In January, the Northwest region ranked first nationwide, accounting for 35% of newly added capacity. Combined, the Northwest and North China regions contributed more than half of the national total. By province, Xinjiang recorded newly added capacity of 1.2 GW / 4.3 GWh, ranking first nationwide in both power and energy capacity.

By the end of January, Xinjiang’s installed renewable energy capacity exceeded 160 GW, accounting for 64% of the region’s total power capacity. Due to its distance from eastern and central load centers, Xinjiang has historically faced wind and solar curtailment challenges. In 2025, wind and solar utilization rates in Xinjiang were 91.0% and 86.3%, respectively—both below the national average. Growing pressure for renewable energy consumption and the need to mitigate grid fluctuations have driven large-scale deployment of new-type energy storage in the region. At the start of the year, several major projects were commissioned in quick succession, including the 500 MW / 2,000 MWh Ruoqiang energy storage project by Xinjiang Green Development Power, the 200 MW / 800 MWh grid-forming energy storage project by Huaneng Jingshun, and the 200 MW / 800 MWh energy storage project by LiXin Energy, demonstrating strong pilot and demonstration effects.

In terms of revenue mechanisms, Xinjiang has formed a relatively mature model combining capacity compensation, electricity energy trading, and ancillary services. On May 19, 2023, the Xinjiang Development and Reform Commission issued the Notice on Establishing and Improving Supporting Policies for the Healthy and Orderly Development of New-Type Energy Storage, introducing capacity compensation for grid-connected independent energy storage projectsand specified the implementation standards for 2023, 2024, and 2025, providing predictable early-stage policy support for independent energy storage projects in Xinjiang. . Although the original policy expired at the end of 2025, the clarification at the national level regarding capacity pricing mechanisms for grid-side independent energy storage is expected to lead to new local policies in Xinjiang, further improving long-term revenue certainty. With the rollout of ancillary service market rules in July 2025 and the transition of Xinjiang’s power spot market to continuous settlement trial operation, independent energy storage is expected to increasingly generate revenue through spot market arbitrage.

Moreover, Xinjiang has established a complete energy storage industry chain, covering batteries, PCS, BMS, and system integration. Large-scale manufacturing bases established by leading energy storage companies, together with local supply chains, have significantly reduced logistics and system integration costs, enhancing project economics. As grid upgrades and transmission channel construction progress, energy storage demand in Xinjiang is expected to be further released.

Figure 3: Regional Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Figure 4: Provincial Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

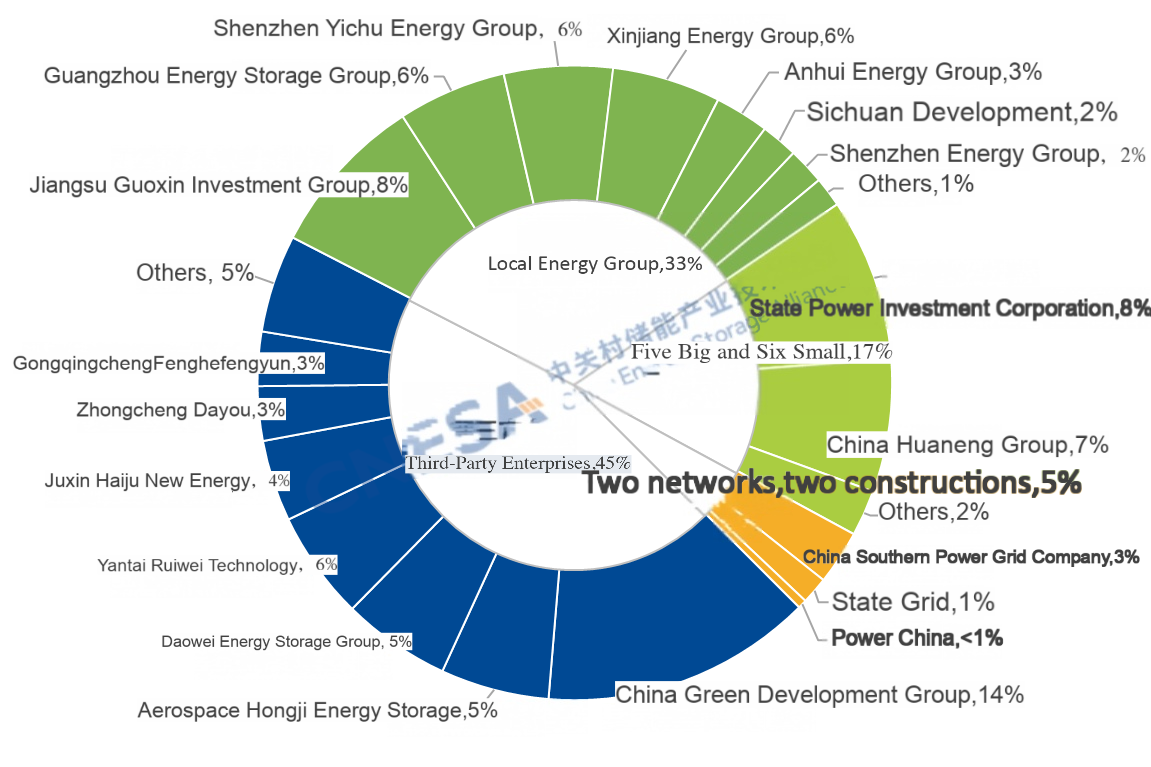

3. Faster Deployment of Projects Invested by Third-Party Enterprises, the trend toward

diversification of energy storage investment entities has become increasingly evident.

In January, projects invested and developed by third-party enterprises—including China Green Development Group, Aerospace Hongji Energy Storage, and Daowei Energy Storage Group—were commissioned one after another. Third-party enterprises accounted for 45% of newly added installed power capacity, ranking first among all investor categories. Driven by rising market demand, supportive national policies, diversified technology pathways, and declining technology costs, the investment entity diversification trend became more pronounced in the first month of 2026.

Figure 5: Owner Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink Global Energy Storage Database

Note: Third-party enterprises refer to companies other than large state-owned power generation groups, the two major grid companies, their construction subsidiaries, and local energy groups.

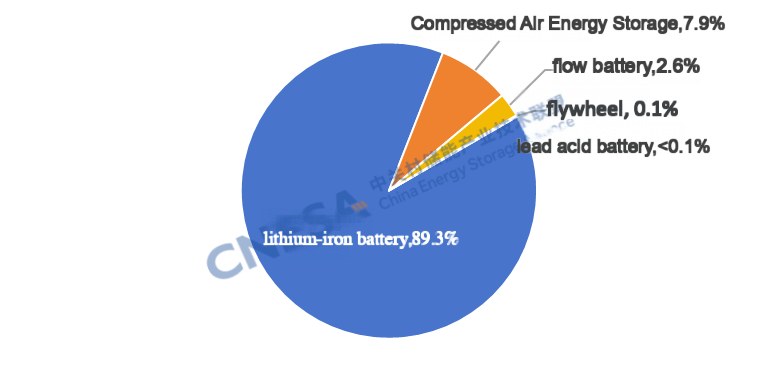

4. Accelerated Deployment of Long-Duration Energy Storage Technologies

From a technology perspective, newly commissioned generation- and grid-side projects were dominated by lithium iron phosphate (LFP) batteries, accounting for 89% of installed power capacity, followed by compressed air energy storage (8%) and flow batteries (3%). Long-duration energy storage technologies—represented by CAES and flow batteries—as well as hybrid frequency regulation systems, are being deployed at an accelerating pace. Notable projects include the 300 MW Jiangsu Huai’an salt cavern CAES demonstration project, the Phase I Baicheng vanadium redox flow battery energy storage power station, and the Changyang Longzhouping vanadium redox flow battery energy storage project. In addition, a lithium battery + flywheel frequency regulation project by Shaanxi Energy was commissioned.

Figure 6: Technology Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

China Energy Storage Alliance (CNESA) continues to track energy storage project developments based on standardized, timely, and comprehensive data collection criteria. Leveraging long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses of energy storage installations, providing valuable references for industry decision-making. Since June 2025, CNESA’s monthly energy storage project analysis has been divided into generation- and grid-side and user-side market reports. This edition focuses on an in-depth interpretation of the generation- and grid-side market in January 2026.

For more comprehensive project information, authoritative data, and in-depth market analysis, please visit www.esresearch.com.cn or access the CNESA DataLink via the mini-program. For customized data consulting services, please contact CNESA through the official QR code. CNESA is committed to providing full-cycle, high-quality energy storage data services to industry stakeholders.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

Major Breakthrough Achieved in the R&D of the World’s First and Most Powerful Single-Unit Compressed Air Energy Storage Compressor

Recently, China has achieved a major breakthrough in the research and development of compressed air energy storage(CAES) technology . Developed jointly by the Institute of Engineering Thermophysics, Chinese Academy of Sciences(IET, CAS) and ZHONG-CHU-GUO-NENG(BEIJING)TECHNOLOGY CO.,LTD., the world’s first CAES compressor with the largest single unit power has successfully passed the third-party testing accredited by CNAS. According to the test results, the compressor achieved maximum discharge pressure of 10.1MPa, a maximum power output of 101MW and an operating range of 38.7% to 118.4% under variable conditions and an efficiency of 88.1% at maximum discharge pressure, reaching an internationally leading level.

Recently, China has achieved a major breakthrough in the research and development of compressed air energy storage(CAES) technology . Developed jointly by the Institute of Engineering Thermophysics, Chinese Academy of Sciences(IET, CAS) and ZHONG-CHU-GUO-NENG(BEIJING)TECHNOLOGY CO.,LTD., the world’s first CAES compressor with the largest single unit power has successfully passed the third-party testing accredited by CNAS. According to the test results, the compressor achieved maximum discharge pressure of 10.1MPa, a maximum power output of 101MW and an operating range of 38.7% to 118.4% under variable conditions and an efficiency of 88.1% at maximum discharge pressure, reaching an internationally leading level.

The compressor is one of the most critical core components of a compressed air energy storage system. During the energy storage process, it will compress the atmospheric pressure air to high-pressure state and store it in gasometers, converting electric energy to pressure energy and thermal energy of the air. Through independent innovation, the research team overcame key technical challenges including overall system design and optimization, full 3-Dimensional flow optimization, long rotor complex shafting structure design and high-efficiency variable operating condition control, successfully developing the world’s first CAES compressor with a single unit power exceeding 100MW, featuring fully independent intellectual property rights. Compared with existing CAES compressors, its single-unit power has increased by more than 100%, unit costs have been significantly reduced and it offers advantages including high efficiency, high pressure and a wide operating range.

The Institute of Engineering Thermophysics, Chinese Academy of Sciences has been a pioneer in China’s CAES research since 2005. Through continuous efforts for over 20 years, it originally proposed new principles for advanced compressed air energy storage, developed several critical technologies including system design for full operating conditions system design, wide-load compressors, high-efficiency compact heat exchangers and high-load expanders; It has established a comprehensive R&D and design system covering “system design-key components-integrated control; it has also taken the lead in building national demonstration projects for 1.5MW-10MW-300MW advanced CAES. The successful development of the CAES marks an important milestone of world compressed air energy storage technology, which will drive the technology to a new level.

The above work was supported by projects including Chinese Academy of Sciences Strategic Priority Research Program (Category A), National Key Research and Development Program of China and National Natural Science Foundation of China (NSFC) Young Scientists Fund (Category A), among others .

Looking ahead, ZHONG-CHU-GUO-NENG will actively promote the application of this compressor and continue to enhance its capabilities in technological innovation, manufacturing, and engineering implementation. Through the transformation and wider application of major scientific and technological equipment achievements, the company aims to deliver high-end equipment with higher efficiency, better performance, and lower costs, thereby driving high-quality industrial development and supporting China’s energy transformation and sustainable development of regional economies.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

Annual Power Cost Savings Exceed RMB 60 Million ! Great Power’s 107MW/428MWh Hydropower-based Aluminium User-side Energy Storage Project is Commissioned

On January 16th, a 107.12MW/428.48MWh green hydropower-based aluminium user-side energy storage project jointly developed by Great Power and Henan Zhongfu Industry was officially commissioned in Guangyuan, Sichuan Province.

On January 16th, a 107.12MW/428.48MWh green hydropower-based aluminium user-side energy storage project jointly developed by Great Power and Henan Zhongfu Industry was officially commissioned in Guangyuan, Sichuan Province.

Designed and delivered under an EPC contract by Sichuan Zefeng Electric Power Design, the project achieved full-capacity grid connection by the end of 2025 after just five months of construction. It stands as a landmark project for green energy transformation in northern Sichuan and a benchmark case for energy-extensive industry implementing “source-grid-load-storage” integration.

Electricity stored at the facility is directly supplied to the electrolytic aluminium production system, primarily leveraging peak-valley electricity price arbitrage to reduce operating cost. According to estimates, the project is expected to lower electricity costs for electrolytic aluminum by approximately RMB 140 per tonne, delivering annual power cost savings of over RMB 60 million. Meanwhile, it will cut 52,000 tons carbon commission per year, providing a commercially viable solution to address high electricity costs and decarbonization pressures faced by energy-extensive industries.

Building on this project, the two partners will be committed to advance the development of a “zero-carbon aluminum industrial park” in Guangyuan. It plans to introduce advanced intelligent technology to build a virtual power plant (VPP) capable of engaging in power trading and grid dispatch. During the 15th Five-Year Plan period, the project developers will further expand the deployment of solar PV, wind power, green power direct supply and intelligent microgrids, ultimately establishing a safe and controllable regional intelligent micro-grid dominated by new energy, providing a practical model for developing a national new-type power system.

_______________________________________________

The Great Power has confirmed its participation in the 14th Energy Storage International Conference and Expo, register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

RMB 180 Billion! China Southern Power Grid Hit a New High for Investment in 2026

Expanding effective investment is a key lever for stabilizing growth and improving people’s livelihoods. According to China Southern Power Grid, the company has embarked RMB 180 billion for fixed-asset investment in 2026, marking a record high for fifth consecutive year, with an annual growth rate of 9.5%. Investment will be directed primarily toward the development of a new-type power system, the growth of strategic emerging industries and the enhancement of high-quality power supply services, providing solid support for a strong start to the 15th Five-Year Plan period.

Expanding effective investment is a key lever for stabilizing growth and improving people’s livelihoods. According to China Southern Power Grid, the company has embarked RMB 180 billion for fixed-asset investment in 2026, marking a record high for fifth consecutive year, with an annual growth rate of 9.5%. Investment will be directed primarily toward the development of a new-type power system, the growth of strategic emerging industries and the enhancement of high-quality power supply services, providing solid support for a strong start to the 15th Five-Year Plan period.

A strong start is decisive, and the opening moves sets the pace. China Southern Power Grid stays committed to the decisions and arrangements of the CPC Central Committee and the State Council, fully fulfilling its responsibilities as a centrally administered state-owned enterprise. Leveraging the power grid’s advantages-- large investment scale, long industrial chain, wide coverage, and strong spillover effects-- the company has expanded fixed-asset investment for five consecutive years. By appropriately advancing the deployment of energy and power infrastructure, it aims to better serve high-quality economic and social development.

Proactively serving the broader national agenda and fully advancing the implementation of major national strategies. China Southern Power Grid is actively supporting efforts to boost domestic consumption by using “two major” and “two new” projects to drive effective investment, and by advancing major projects under the “15th Five-Year Plan”. The company will intensify the renewal of grid infrastructure and digital and intelligent transformation with no less than RMB 50.6 billion to be invested in large-scale equipment renewal this year. To promote coordinated urban-rural regional development, the company will fully boost the construction of world-level bay area, advance power infrastructure development in Hainan ahead of demand and address weak links in grid facilities in Yunnan, Guizhou, and Guangxi. In Hainan, major projects including the 500kV offshore wind transmission are set to break ground this year, accelerating energy structure transformation and injecting strong momentum for Hainan Free Trade Port construction. In Guangxi, 220kV Weizhou Island cross-sea interconnection project has completed submarine cable laying and is scheduled to be commissioned in the first quarter of this year. In support of high-quality Belt and Road cooperation, thei China-Laos 500kV interconnection project is expected to be fully commissioned in the first half of the year.

Driving industrial upgrading and building a modern industrial system. China Southern Grid focuses on strengthening modern grid infrastructure, accelerate to built a backbone grid centered on flexible DC interconnections, intensify distribution network upgrades, and promote high-standard digital and intelligent grid planning and development. In Guangdong, the Guangzhou Tianhe Tangxia flexible DC project is scheduled to be commissioned by year-end. Using internationally leading multi-terminal flexible DC power interconnection control technology, the project will provide a new solution for reliable power supply to high-density load centers in mega-city grids. In Yunnan, the second interconnection project for Dulongjiang is planned to start construction in the first quarter, aiming to establish a demonstration zone for digital and intelligent microgrids. To foster and expand strategic emerging industries, China Southern Grid will accelerate the expansion and quality improvement of charging and battery-swapping infrastructure, strengthen the “Dianhong” ecosystem, and proactively deploy new frontiers such as marine energy and embodied intelligence. In Shenzhen, the largest vehicle-to-grid demonstration station in the Guangdong–Hong Kong–Macao Greater Bay Area will be commissioned in the first quarter, further accelerating the development of a “city of ultra-fast charging.” China Southern Grid will also promote high-quality and efficient power supply services by implementing a three-year action plan to improve power quality and launching targeted initiatives to enhance electricity services for people’s livelihoods. In Guizhou, power support projects for 610 clusters of rural wooden-house villages in the Qiandongnan Miao and Dong Autonomous Prefecture are scheduled to be fully completed and commissioned within the year.

Upholding dual-carbon goals and advancing “Two-Type” development. The company is supporting the high-quality development of renewable energy by coordinating large-scale development with high-level grid integration, enhancing the observability, controllability, and dispatchability of renewables, and improving intelligent dispatch and control capabilities. These efforts will support the addition of 40 million kilowatts of new renewable energy capacity this year. In Guangdong, the Yangjiang Sanshan Island offshore wind power flexible DC transmission project is more than halfway complete and is scheduled to be commissioned by year-end, delivering approximately 6 billion kWh of green electricity annually directly to the Guangdong–Hong Kong–Macao Greater Bay Area. To integrate into the national power productivity layout, construction of projects such as the Tibet–Guangdong DC transmission and Hunan–Guizhou flexible power interconnection is accelerating, facilitating the import of clean electricity from outside regions. CSG is also promoting the integrated development of electricity, carbon, and computing power, building new infrastructure that combines “power + computing,” upgrading the integrated operation platform, and advancing the development of a number of zero-carbon industrial parks and factories.

register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Adress: No. 55 Yudong road, Shunyi District, Beijing China

2025 Marks the First Year of Mass Production for Large Energy Storage Cells! 500Ah+ Mass Deliveries, ESIE 2026 Energy Storage Expo Invites Global Buyers to Explore New Opportunities

2025 marks a pivotal year for the energy storage industry. The large energy storage cells, which were once limited to “theoretical parameters”, will officially bid farewell to the technical competition phase and enter the practical testing stage of capacity release, yield improvement, and project implementation. Leading enterprises like CATL, EVE, Envision, HTHIUM, and SUNWODA have successively achieved mass production and delivery, and with the intensive landing of GWh-level strategic cooperation and accelerated expansion into overseas markets, this marks the transition of large-capacity cells from lab prototypes to commercial applications. The speed at which energy storage systems are evolving to higher energy density and lower cost has far exceeded industry expectations.

2025 marks a pivotal year for the energy storage industry. The large energy storage cells, which were once limited to “theoretical parameters”, will officially bid farewell to the technical competition phase and enter the practical testing stage of capacity release, yield improvement, and project implementation. Leading enterprises like CATL, EVE, Envision, HTHIUM, and SUNWODA have successively achieved mass production and delivery, and with the intensive landing of GWh-level strategic cooperation and accelerated expansion into overseas markets, this marks the transition of large-capacity cells from lab prototypes to commercial applications. The speed at which energy storage systems are evolving to higher energy density and lower cost has far exceeded industry expectations.

1. The Race for 500Ah+ Cell Mass Production Intensifies: Leading Enterprises Show Impressive Results

2025 is the “explosive year” for the mass production and delivery of large energy storage cells, with many battery companies accelerating capacity ramp-up, and products of 500Ah and above being extensively landed, demonstrating strong commercialization capabilities:

CATL: The 587Ah energy-specific storage cell began mass production in

June, with a daily output of over 220,000 units from its Jining base. By December, it had shipped 2GWh, with an expected annual output of 3GWh, taking the lead in entering into GWh-level commercial-scale applications;

EVE: The 628Ah cell, mass-produced at the end of 2024, achieved the production of 750,000 cells in 2025, and in September, it was successfully used in the world’s first 100MWh-level project--200MW/400MWh independent energy storage station in Ling Shou, Hebei with overseas shipments proceeding in parallel;

Envision: The 500+Ah cell, produced at its Cangzhou plant, has already been exported immediately after mass production, and next-generation 700Ah+ products are also in the mass production preparation phase;

HTHIUM: The world’s first 1,175Ah ∞Cell was launched and mass-produced, while the 587Ah cells were simultaneously delivered in Xiamen base. In October, a 6.25MWh energy storage system, equipped with the 1,175Ah cells, was successfully shipped to Europe;

SUNWODA: The 684Ah stacked cell began mass production in September, and by the end of December, 1 million cells had been produced, highlighting its fast mass production capability.

Additionally, companies such as cornex, GREAT POWER, CALB, RJE, Narada, GOTION HIGH-TECH, REPT BATTERO, and AC New Energy have announced mass production schedules for 500Ah+ and 600Ah+ products. The competition in the large energy storage cell market is expected to fully intensify in 2026.

2. GWh-level strategic partnerships become the mainstream, supply chain synchronization trend emerges

As cell technology gradually converges, supply chain stability and cost control have become the core of market competition. The collaboration model between system integrators and battery companies is evolving toward long-term, large-scale, and deep integration. By the end of 2025, heavy GWh-level orders have emerged, reshaping the industry’s collaboration landscape:

CATL and HYPER STRONG signed a procurement agreement for no less than 200GWh from 2026 to 2028, with the 587Ah cell already being used in the 400MW/2400MWh energy storage project in Baotou;

HTHIUM and CRRC Zhuzhou Institute reached collaboration for 120GWh of energy storage products supply during the 15th Five-Year Plan period, covering the full range products from 314Ah to 1,175Ah;

EVE and Rochenergy signed a three-year 20GWh collaboration agreement, with 10GWh dedicated to the 628Ah/588Ah large-capacity cells;

Sungrow and Sunwoda have deepened their collaboration, with their Powertitan 3.0 energy storage system set to apply the 684Ah large-capacity cell.

These long-term strategic partnerships not only ensure mutual capacity demand but also drive early-stage collaborative development between systems and cells, becoming an industry trend, deeply integrating product performance and safety systems to reduce costs and improve efficiency for energy storage projects.

3. Accelerating overseas expansion! China’s large energy storage cells lead the global long-duration storage market

Leveraging the advantage of complete industry chain, China’s large energy storage cells are rapidly expanding globally. The results of overseas market expansion in 2025 are significant, evolving from single-product exports to system solutions and standards:

CATL’s 530Ah cells, coupled with a 4GWh energy storage system, will supply Vena Energy in Singapore.

EVE Energy’s 628Ah cells successfully secured a 2.2GWh order from Australia’s EVO Power and signed a 1GWh energy storage system project with TSL Assembly.

The global expansion of China’s large energy storage cells not only opens up the long-duration storage market overseas but also enables Chinese energy storage technology standards and solutions to gain global recognition, showcasing China’s core competitiveness in global energy storage industry. Currently, while the 500Ah+ cells are still in a period of rapid development with diverse sizes and specifications, industry consensus is clear: 6MWh+ energy storage systems will accelerate the replacement of the previous 5MWh+ solutions, continuously driving down the cost per unit of energy storage. From mass production and deliveries and strategic partnerships to global project implementation, 2025 undoubtedly marks the “first practical year” for large energy storage cells transitioning from laboratory prototypes to station applications.

4. Focus on ESIE 2026! The vane of global energy storage industry , connecting professional buyers with core resources

As large-capacity cell technology rapidly evolves and global markets continues to expand, the industry urgently needs an efficient platform to connect cutting-edge technology, market dynamics, and supply chain resources. As a “vane” for the energy storage industry, the 14th Energy Storage International Conference & Expo (ESIE 2026) will be grandly held from March 31 to April 3, 2026, at the Capital International Exhibition & Convention Center Beijing China.

So far, leading industry enterprises including CATL, EVE, Envision, HTHIUM , SUNWODA, Cornex, GREAT POWER, CALB, RJE, Narada, GOTION HIGH-TECH, REPT BATTERO, and AC NewEnergy have confirmed their participation. This year’s exhibition will focus on key areas such as large energy storage cells, long-duration storage, energy storage system integration, and integrated solar+storage+charging solutions. It will serve as a high-end platform for new product launches, technical exchanges, and business negotiations, offering global energy storage professional buyers a precise matchmaking channel.

Whether seeking cutting-edge technology collaborations, exploring quality supply chain resources, or planning global energy storage projects, ESIE 2026 will be an unmissable annual event for industry professionals. We sincerely invite global energy storage professional buyers and upstream and downstream enterprises to gather in Beijing to explore new trends in the industry and seize new opportunities for industrial upgrading.

Address: Capital International Exhibition & ConventionCenter Beijing China

When: March 31 – April 3, 2026

Highlights: Leading enterprises gathering, new product launches, precise supply-demand matchmaking, authoritative trend interpretations

Exhibition and Visitor Inquiries: Mr. Cao: +86 135 5271 2189, Mr. Wang: +86 135 8188 5520, Mr. Li: +86 135 8174 1680, Mr. Zhao: +86 182 1018 8771, Ms. Bai: +86 180 3145 1007

A 100-Billion-Yuan Market for Power Battery Recycling Is on the Horizon!

Source: Xinhua News Agency

At a press conference on the standardization of power battery recycling held by the State Administration for Market Regulation (SAMR), it was revealed that China is about to enter the large-scale retirement phase of power batteries, based on their service life projections. The domestic market for power battery recycling is expected to exceed 100 billion yuan by 2030. According to statistics, in 2024, China’s total volume of recycled power batteries surpassed 300,000 tons, corresponding to a market size of over 48 billion yuan.

Liu Hongsheng, Director-General of the Department of Standards and Technology under the SAMR, stated that SAMR, together with the Ministry of Industry and Information Technology and other relevant departments, has been actively advancing the formulation and release of national standards covering the entire industrial chain of power battery recycling. These standards provide strong technical support for the development of the recycling industry.

To date, 22 national standards have been issued in China for power battery recycling and utilization. These cover areas such as general requirements, management specifications, dismantling procedures, residual energy testing, regeneration and reuse, lithium-ion waste recycling, and recycled black mass, effectively supporting and guiding the high-quality development of the industry.

Xie Zaichun, Deputy Director-General of the Fujian Provincial Administration for Market Regulation, noted that Fujian Province, as a key production base for power batteries in China, has achieved deep integration of technological innovation and standard development, forming a replicable and scalable model for standardization demonstration.

Brunp Recycling, a subsidiary of CATL, has transformed its self-developed DRT directional recycling technology into an advanced industrial standard, achieving 99.6% recovery rates for nickel, cobalt, and manganese, and 96.5% for lithium. In 2024, the company processed over 120,000 tons of used batteries and produced 17,100 tons of regenerated lithium salts.

Quanzhou Qingneng New Energy Technology Company has established a comprehensive standard system and, in 2024, processed 238 tons of retired batteries, achieving 238 tons of carbon reduction and generating 23 million yuan in output value.

Liu Hongsheng added that SAMR will accelerate the construction of a standard system for power battery recycling and utilization, focusing on areas such as green design, residual energy detection, discharge, storage, and directional recycling. The goal is to further enhance the role of standards in supporting and leading the sustainable development of China’s power battery recycling industry.

CENSA Upcoming Events:

1. Dec.4-5 | 2025 China Energy Storage CEO Summit | Xiamen, Fujian

Register Now to attend

Read more: http://en.cnesa.org/new-events-1/2025/12/4/dec4-5-2025-china-energy-storage-ceo-summit

2. Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Oct 31, 2025.

Sign up for our free monthly newsletter to stay informed about the Chinese energy storage market.