New Installations Surge Over 120% YoY — February Analysis of China’s New Energy Storage Projects

In February 2026, China’s new energy storage market sustained its rapid growth momentum, with newly installed capacity increasing by over 120% year-on-year (YoY). Meanwhile, the application structure of the market has undergone adjustments compared with the same period last year.

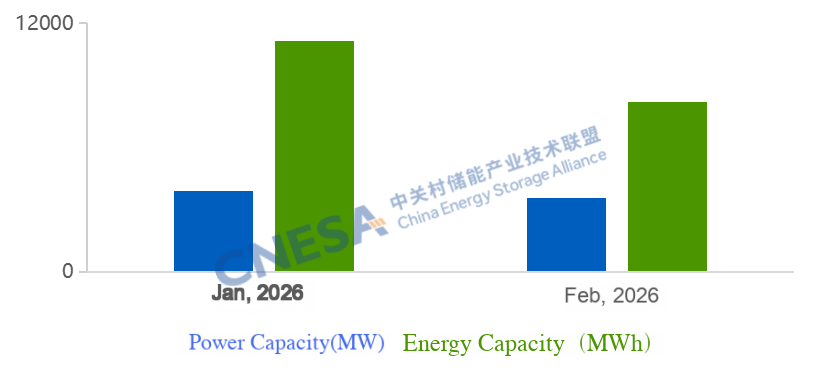

Short-term fluctuations do not alter long-term growth trend: In February, newly installed capacity reached 3.6 GW, representing a YoY increase of over 120% and a month-on-month (MoM) decline of 31%. Despite the short-term slowdown, the long-term growth trajectory of the energy storage market remains strong.

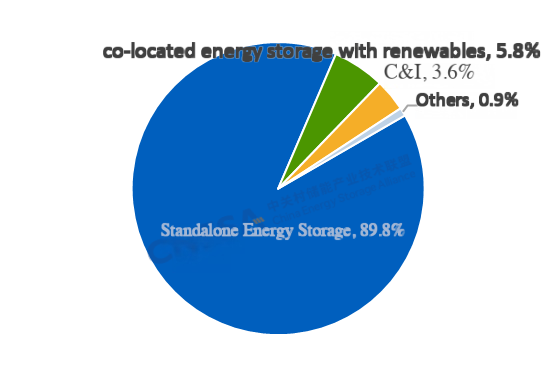

Front-of-the-meter standalone storage drives growth: Standalone energy storage on the generation and grid side became the primary growth driver. In February, standalone storage accounted for 90% of newly added capacity, up 42 percentage points YoY. Newly installed power and energy capacity of standalone storage increased by more than 310% and 270% YoY, respectively.

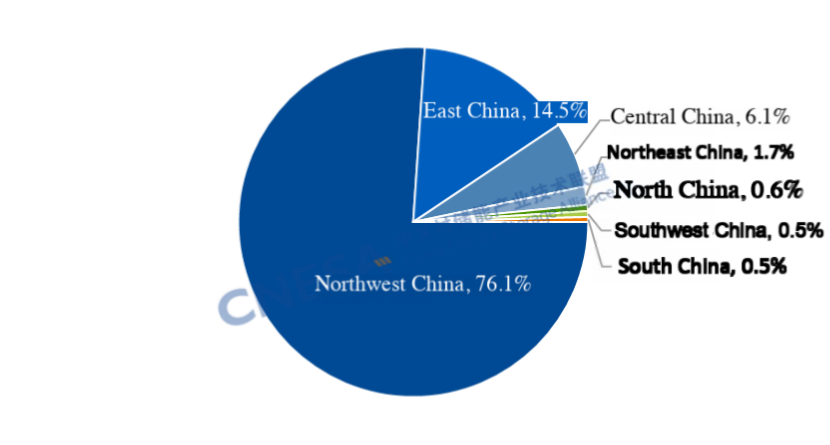

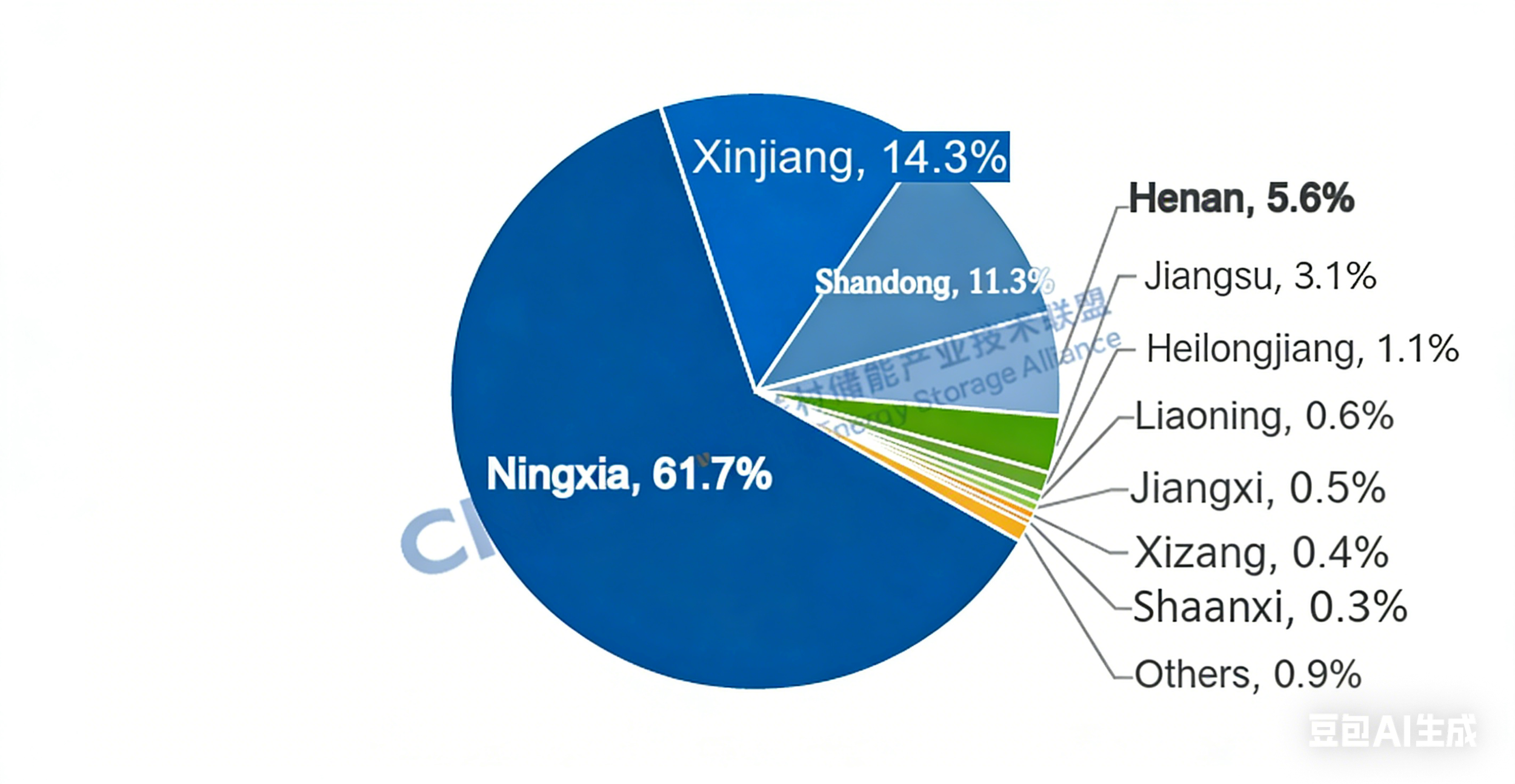

Highly concentrated regional deployment: The Northwest region accounted for over 75% of total additions, with Ningxia alone exceeding 2 GW, contributing more than 60% of the national total.

According to incomplete statistics from China Energy Storage Alliance(CNESA), China commissioned 3.56 GW / 8.19 GWh of new energy storage capacity in February 2026, representing YoY increases of +120% / +95% and MoM declines of -31% / -21%.

The MoM decline was mainly due to project construction cycles and the impact of the Spring Festival holiday. However, the YoY growth exceeding 120% indicates a fundamentally positive market outlook. Notably, front-of-the-meter (FTM) installations reached 3.4 GW, up 147% YoY, effectively doubling the total monthly additions.

Key Market Characteristics in February

1. Standalone Storage Surges Over 270%, Driving Market Expansion

In terms of application structure, standalone energy storage dominated the market. It accounted for 90% of total newly installed power capacity, up 42 percentage points YoY and 8 percentage points MoM. Newly added capacity reached 3.2 GW / 7.4 GWh, with YoY growth of +313% / +274%, becoming the main driving point of energy storage market. All newly commissioned standalone energy storage projects reached at least the 100 MW level, with the number of such projects rising by 29% year-on-year, alongside the commissioning of two gigawatt-scale projects.

Installations on the generation side and behind-the-meter (BTM) user side experienced a temporary decline. Newly installed capacity on the generation side reached 217.3 MW / 474.3 MWh, down 65% / 72% year-on-year and 41% / 36% month-on-month. Co-located storage with renewable energy remained the dominant model, covering a range of application scenarios such as aquaculture, solar hybrid projects and desertification control initiatives.

New user-side installations totaled 135.2 MW / 292.7 MWh, down 41% / 42% year-on-year and 51% / 58% month-on-month. The market was highly concentrated, with Jiangsu, Guangdong, and Zhejiang accounting for 90% of total user-side energy storage capacity, while Jiangsu ranked first nationwide in both installed capacity and project count.

On the technology front, lithium-ion batteries continued to scale rapidly, supporting the commissioning of gigawatt-level standalone storage plants. Meanwhile, hybrid systems combining lithium-ion and sodium-ion batteries at the 100 MW level were deployed, and aqueous organic flow batteries were implemented on the user side, providing more diversified technological pathways for long-term development.

2. Regional Concentration Intensifies, Northwest China Dominates

In February, regional concentration of new installations was pronounced. The Northwest region added 2.7 GW, accounting for 76% of the national total. The combined share of the Northwest and North China regions exceeded 90%. Ningxia added 2.2 GW / 4.4 GWh of new capacity, ranking first nationwide in both power and energy scale and setting a new monthly record for the region. This surge was driven by the grid connection of several gigawatt-scale shared energy storage projects and storage systems paired with large renewable energy bases.

By the end of 2025, Ningxia’s renewable energy capacity reached 57.32 GW, accounting for 65.5% of total grid capacity under centralized dispatch. Solar power has surpassed coal-fired generation to become the largest power source in the region. Due to the intermittency of renewables—characterized by surplus generation during the day and shortages at night—demand for grid services such as peak shaving and frequency regulation has surged. A coordinated development model integrating wind, solar, thermal power, and energy storage is rapidly taking shape. Looking ahead, energy storage is expected to generate revenue through multiple channels, including capacity compensation, spot market trading, frequency regulation services, ramp rate support and so on.

In addition, Ningxia has introduced policies encouraging private capital participation in energy storage investment. In February, a gigawatt-scale storage project developed by Jiayang Energy was commissioned, demonstrating strong investor confidence in the region. At the end of February, the region released its first batch of 2026 private investment promotion projects, including 22 energy storage projects with a total scale of 4.15 GW / 14.4 GWh, providing a solid pipeline for continued market growth.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China