10.9 GWh! Newly Added New-Type Energy Storage Capacity in January Doubled Year-on-Year

China’s new-type energy storage market witnessed a strong start in January 2026. Newly commissioned capacity in January increased by over 60% year-on-year, while the market’s underlying structure showed notable adjustments compared with the same period last year.

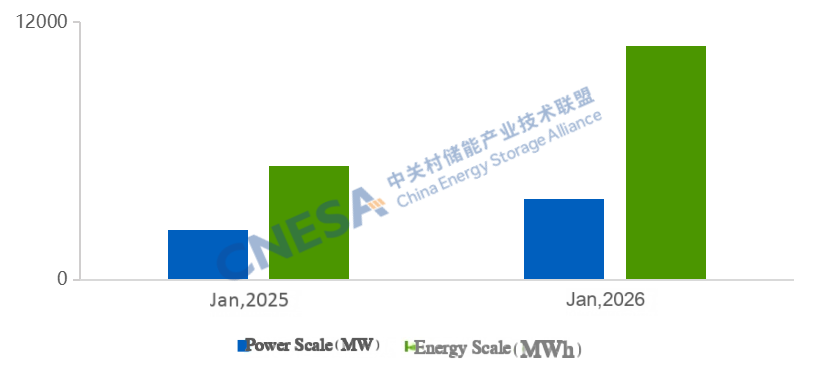

A Strong Start to the Year: Newly added capacity: 3.8 GW / 10.9 GWh in January, representing a

year-on-year increase of 62% / 106%, marking a positive opening for the new-type energy storage

market.

Accelerated Deployment of Independent Energy Storage: In January, independent energy

storage accounted for nearly 90% of newly added capacity, up 41 percentage points year-on-

year. Newly added power and energy capacity of independent energy storage grew by over 240% /

290% year-on-year. Xinjiang ranked first nationwide in both power and energy capacity, with 1 GW

of newly commissioned independent energy storage.

Rise of Third-Party Enterprises: Third-party enterprises accounted for 45% of newly added

installed capacity, once again surpassing local energy groups and the “Big Five and Small Six”

state-owned power generation groups. The trend toward a diversified investment landscape has

become increasingly evident.

Accelerated Deployment of Diverse Technologies: Beyond mainstream lithium-ion batteries,

alternative technologies such as compressed air energy storage (CAES), flow batteries, and

flywheels are being deployed at a faster pace, supporting the industry’s long-term development.

Overall Analysis of New-Type Energy Storage Projects in January

According to incomplete statistics from the CNESA DataLink, in January 2026, newly commissioned new-type energy storage projects in China reached a total installed capacity of 3.78 GW / 10.90 GWh, representing year-on-year increases of 62% and 106%, respectively, and month-on-month declines of 84% and 86%. Monthly new added capacity growth exceeded 60% year-on-year, underscoring a positive market outlook at the beginning of the year.

Figure 1: Installed Capacity of Newly Commissioned New-Type Energy Storage Projects in China, January 2026

Source: CNESA DataLink

Note: Year-on-year (YoY) comparisons are based on the same period of the previous year; month-on-month (MoM) comparisons are based on the immediately preceding statistical period.

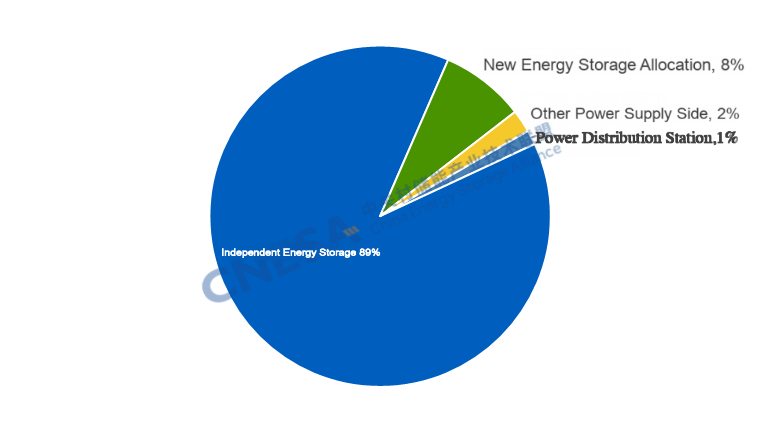

Analysis of Generation- and Grid-Side New-Type Energy Storage Projects in January

In January, newly added generation- and grid-side new-type energy storage capacity reached 3.62 GW / 10.44 GWh, up 87% / 130% year-on-year, and down 84% / 87% month-on-month. Key characteristics include:

1.Independent energy storage accounted for 89% of new installations, up 41 percentage

points year-on-year and 12 percentage points month-on-month.

Newly added independent energy storage reached 3.2 GW / 9.6 GWh, up 249% / 298% year-on-year, and down 84%/87% month-on-month. The number of projects with capacities of 100 MW and above increased by 122% year-on-year, accounting for 85% of total projects—29 percentage points higher than the same period last year. By contrast, power-generation-side new-type energy storage additions were 366.5 MW / 740.3 MWh, down 64% / 65% year-on-year and 92% / 95% month-on-month. Among these, renewable-plus-storage projects accounted for 79% of power capacity, spanning diversified application scenarios such as desertification control, thermal–renewable–storage multi-energy integration, and hydro–solar–pumped storage integration.

Figure 2: Application Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

Note: “Others” include substations, emergency power supplies, etc.

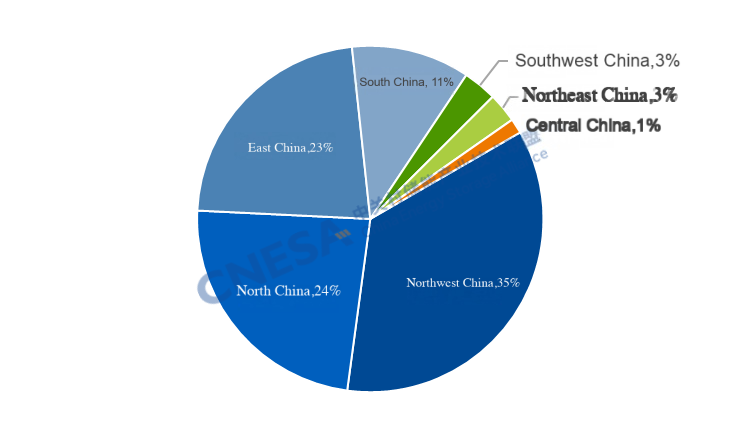

2. Northwest China Accounted for Over 35% of New Capacity, with Xinjiang Leading

In January, the Northwest region ranked first nationwide, accounting for 35% of newly added capacity. Combined, the Northwest and North China regions contributed more than half of the national total. By province, Xinjiang recorded newly added capacity of 1.2 GW / 4.3 GWh, ranking first nationwide in both power and energy capacity.

By the end of January, Xinjiang’s installed renewable energy capacity exceeded 160 GW, accounting for 64% of the region’s total power capacity. Due to its distance from eastern and central load centers, Xinjiang has historically faced wind and solar curtailment challenges. In 2025, wind and solar utilization rates in Xinjiang were 91.0% and 86.3%, respectively—both below the national average. Growing pressure for renewable energy consumption and the need to mitigate grid fluctuations have driven large-scale deployment of new-type energy storage in the region. At the start of the year, several major projects were commissioned in quick succession, including the 500 MW / 2,000 MWh Ruoqiang energy storage project by Xinjiang Green Development Power, the 200 MW / 800 MWh grid-forming energy storage project by Huaneng Jingshun, and the 200 MW / 800 MWh energy storage project by LiXin Energy, demonstrating strong pilot and demonstration effects.

In terms of revenue mechanisms, Xinjiang has formed a relatively mature model combining capacity compensation, electricity energy trading, and ancillary services. On May 19, 2023, the Xinjiang Development and Reform Commission issued the Notice on Establishing and Improving Supporting Policies for the Healthy and Orderly Development of New-Type Energy Storage, introducing capacity compensation for grid-connected independent energy storage projectsand specified the implementation standards for 2023, 2024, and 2025, providing predictable early-stage policy support for independent energy storage projects in Xinjiang. . Although the original policy expired at the end of 2025, the clarification at the national level regarding capacity pricing mechanisms for grid-side independent energy storage is expected to lead to new local policies in Xinjiang, further improving long-term revenue certainty. With the rollout of ancillary service market rules in July 2025 and the transition of Xinjiang’s power spot market to continuous settlement trial operation, independent energy storage is expected to increasingly generate revenue through spot market arbitrage.

Moreover, Xinjiang has established a complete energy storage industry chain, covering batteries, PCS, BMS, and system integration. Large-scale manufacturing bases established by leading energy storage companies, together with local supply chains, have significantly reduced logistics and system integration costs, enhancing project economics. As grid upgrades and transmission channel construction progress, energy storage demand in Xinjiang is expected to be further released.

Figure 3: Regional Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

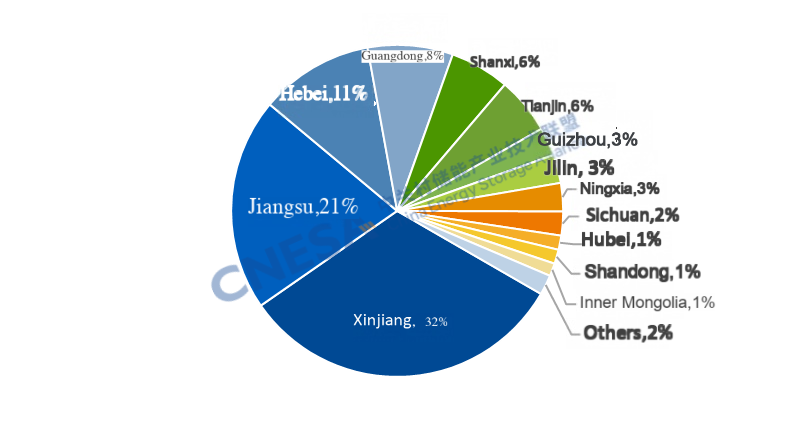

Figure 4: Provincial Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

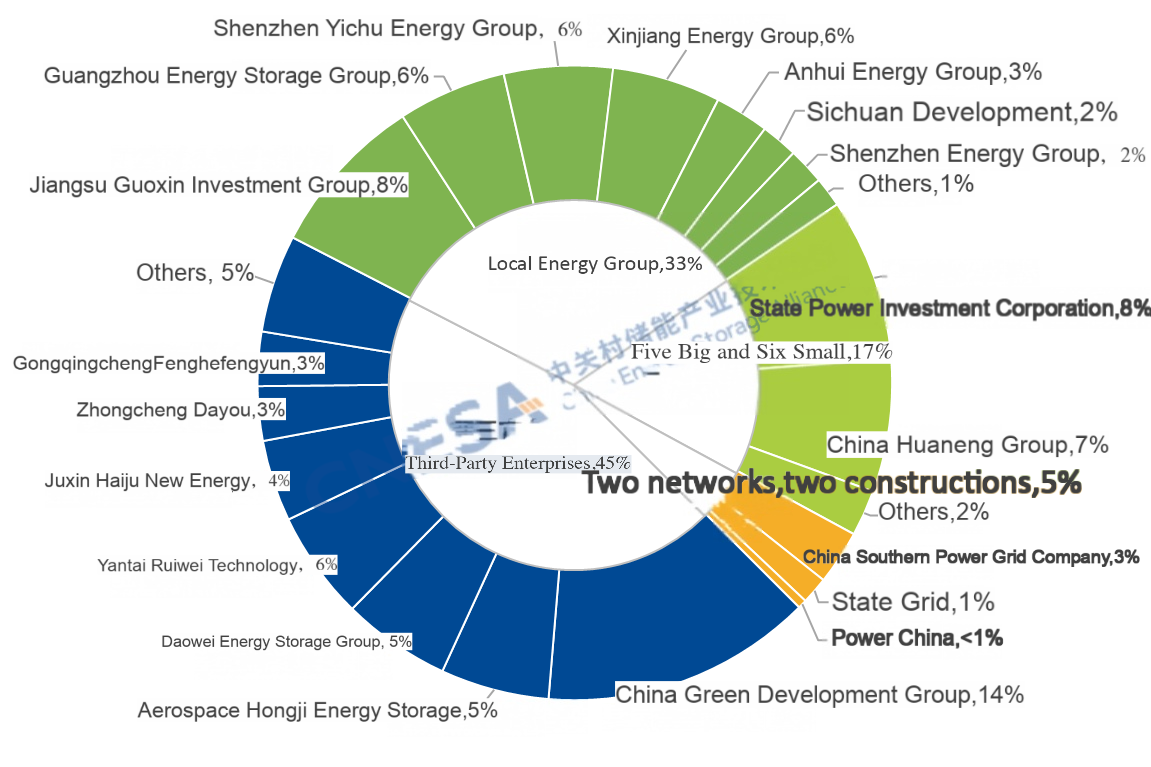

3. Faster Deployment of Projects Invested by Third-Party Enterprises, the trend toward

diversification of energy storage investment entities has become increasingly evident.

In January, projects invested and developed by third-party enterprises—including China Green Development Group, Aerospace Hongji Energy Storage, and Daowei Energy Storage Group—were commissioned one after another. Third-party enterprises accounted for 45% of newly added installed power capacity, ranking first among all investor categories. Driven by rising market demand, supportive national policies, diversified technology pathways, and declining technology costs, the investment entity diversification trend became more pronounced in the first month of 2026.

Figure 5: Owner Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink Global Energy Storage Database

Note: Third-party enterprises refer to companies other than large state-owned power generation groups, the two major grid companies, their construction subsidiaries, and local energy groups.

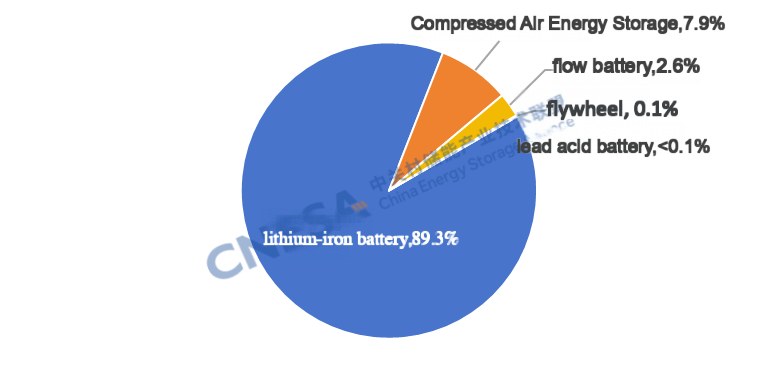

4. Accelerated Deployment of Long-Duration Energy Storage Technologies

From a technology perspective, newly commissioned generation- and grid-side projects were dominated by lithium iron phosphate (LFP) batteries, accounting for 89% of installed power capacity, followed by compressed air energy storage (8%) and flow batteries (3%). Long-duration energy storage technologies—represented by CAES and flow batteries—as well as hybrid frequency regulation systems, are being deployed at an accelerating pace. Notable projects include the 300 MW Jiangsu Huai’an salt cavern CAES demonstration project, the Phase I Baicheng vanadium redox flow battery energy storage power station, and the Changyang Longzhouping vanadium redox flow battery energy storage project. In addition, a lithium battery + flywheel frequency regulation project by Shaanxi Energy was commissioned.

Figure 6: Technology Distribution of Newly Commissioned Generation- and Grid-Side New-Type Energy Storage Projects in January 2026 (MW%)

Source: CNESA DataLink

China Energy Storage Alliance (CNESA) continues to track energy storage project developments based on standardized, timely, and comprehensive data collection criteria. Leveraging long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses of energy storage installations, providing valuable references for industry decision-making. Since June 2025, CNESA’s monthly energy storage project analysis has been divided into generation- and grid-side and user-side market reports. This edition focuses on an in-depth interpretation of the generation- and grid-side market in January 2026.

For more comprehensive project information, authoritative data, and in-depth market analysis, please visit www.esresearch.com.cn or access the CNESA DataLink via the mini-program. For customized data consulting services, please contact CNESA through the official QR code. CNESA is committed to providing full-cycle, high-quality energy storage data services to industry stakeholders.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China