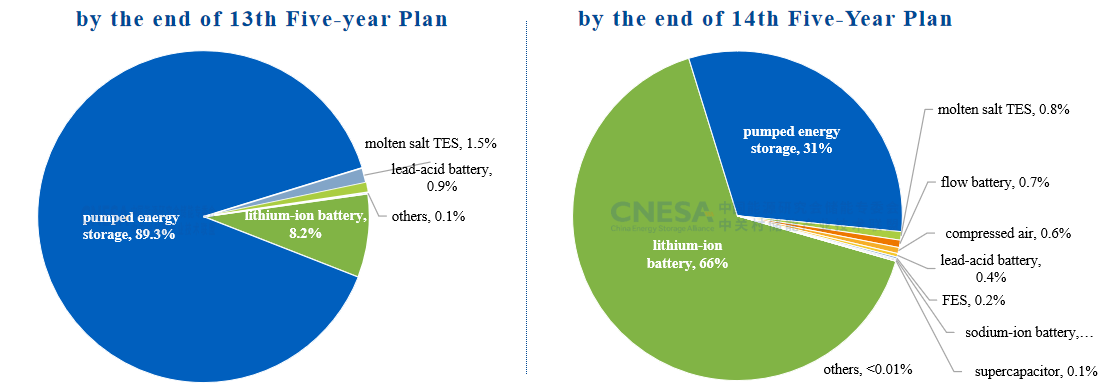

During the 14th Five-Year Plan period, China’s energy storage technology mix witnessed noticeable changes where pumped hydro storage accounted for less than 40% for the first time while the new-type energy storage represented by lithium batteries saw explosive growth.

500MWh!BYD Energy Storage Has Commissioned Its Largest Energy Storage Project in East Europe

On January 8, 2026, a 500MWh standalone Battery Energy Storage System(BESS) project located at Maritsa East 3 in Bulgaria was officially commissioned. The project was the jointly developed by BYD Energy Storage and ContourGlobal under their strategic collaboration which is one of the largest standalone energy storage projects in East Europe.

Tianneng Signs a 1GWh Project in Malaysia, Build a benchmark for Integrated “Solar- Storage- Computing”Solutions

Recently, Tianneng Group signed a strategic agreement with NASDAQ-listed company VCIG Group. The two parties will build a 1GWh AIDC solar energy storage power station in Malacca, Malaysia. The project aims to address the high-energy-consumption challenge of AIDC and will be developed under an “EPC+F” model.

An additional 66.43GW/189.48GWh Added! CNESA DataLink 2025 Annual Energy Storage Data Release

On January 22, Energy Storage International Conference and Expo 2026 Press together with CNESA DataLink 2025 Annual Energy Storage Data Release was held in Beijing, China. Enterprises across the energy storage value chain and authoritative media outlets closely following the sector gather together to review the past developments and look ahead to the future.

During the press, Chen Haisheng, director, Institute of Engineering Thermophysics, Chinese Academy of Sciences Chairman, China Energy Storage Alliance, on behalf of China Energy Storage Alliance (CNESA), delivered a comprehensive overview of the development of China’s new-type energy storage industry in 2025 and shared insights into trends for 2026.

Liu Wei, Secretary General of CNESA reported the preparatory progress of the 14th Energy Storage International Conference And Expo (ESIE 2026). ESIE 2026 is set to achieve comprehensive value upgrade with the core to build a true “energy storage ecosystem exhibition”. It aims to not only attract attention but committed more to create industry value-- through accurate resource matching, in-depth content services and long-term and effective ecosystem connections to establish a platform empowering the full lifecycle growth of energy storage enterprises.

Meanwhile, as China stands at the critical juncture of market-oriented transition for standalone energy storage during the 15th Five-Year Plan period, amid widening regional policy divergence and rising challenges in industrial decision-making, CNESA released the first toolbook-style policy map for standalone energy storage market mechanisms. It will also focus on key policies in 21 provinces, break down their revenue models, explore mechanism highlights and evaluate the profitability level, providing efficient decision-making references for governments, companies and investment institutions and contributing to the industry high-quality development.

01.

Scale of New-type Energy Storage Projects

Total Power Storage Capacity Reaches 213.3GW with New-Type Energy Storage Accounting for Over Two Thirds

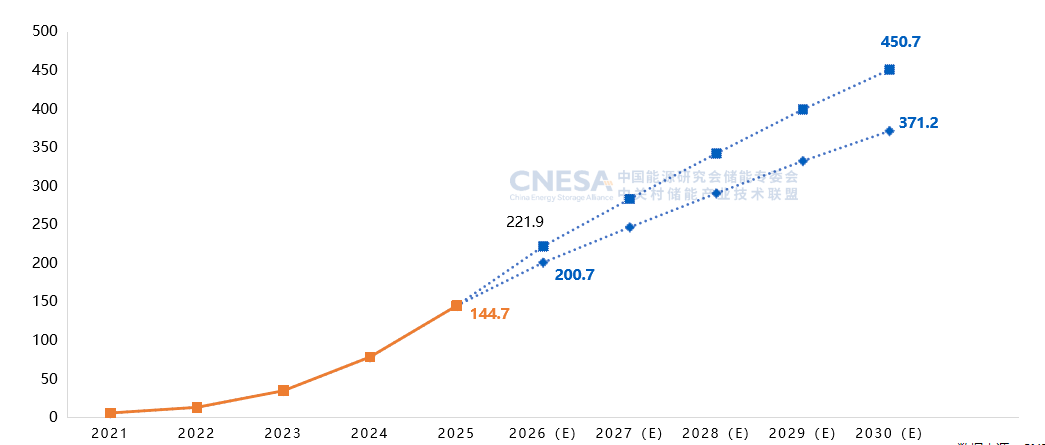

According to the incomplete statistics from CNESA Datalink Global Energy Storage Database, by the end of December, 2025, China’s cumulative installed power storage capacity reached 213.3GW with an increase of +54% year on year. 2025 marks the end year of the 14th Five-Year Plan, the market share of energy storage technologies saw changes compared with that of the 13th Five-Year Plan period. Pumped hydro storage accounted for 31.3% of total capacity, the new-type energy storage represented by lithium battery witnessing leapfrog growth and the cumulative installed capacity of new-type energy storage exceeded two thirds of the total, accelerating the industry’s transition from single dominant technology toward diversified development.

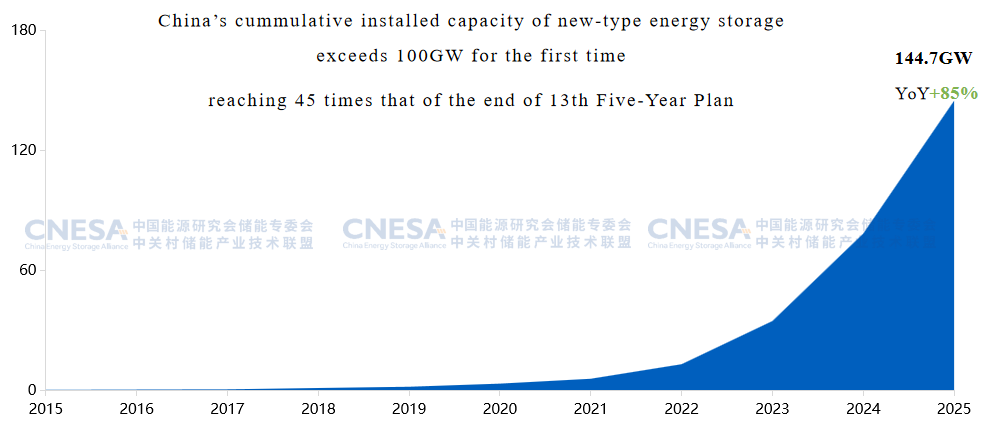

Cumulative Installed Capacity of New-Type Energy Storage Exceeds 100GW

By the end of December, 2025, China’s cumulative installed capacity of new-type energy storage reached 144.7GW, witnessing a year-on-year increase of +85%. It was the first time that China’s cumulative installed capacity of new-type energy storage exceeded 100GW, reaching 45 times that of the end of 13th Five-Year Plan. The major application scenario of China’s new-type energy storage has shifted from being dominated by the user-side (35%) to being primarily standalone energy storage (58%); Thermal power plus storage for frequency regulation (1.4%) and user-side storage (8%) witnessed evident decline; New energy paired storage share remains steady.

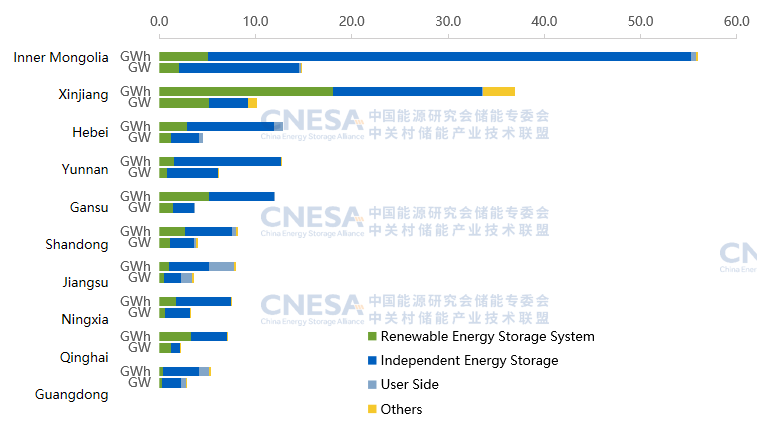

Newly Commissioned Capacity Reaches 66.43GW/189.48GWh

China commissioned 66.43GW/ 189.48GWh of new-type energy storage capacity, with an increase of 52%/73% in power size and energy scale respectively. In terms of regional dispatch, all top 10 provinces’ installed capacity was more than 5GWh, totaling about 90%; Western provinces took full lead, with Inner Mongolia ranking first in both power and energy capacity, surpassing California to become the world’s leading province by scale. Yunnan Province entered the Top10 for the first time.

02. New-Type Energy Storage Bidding and Tendering Market

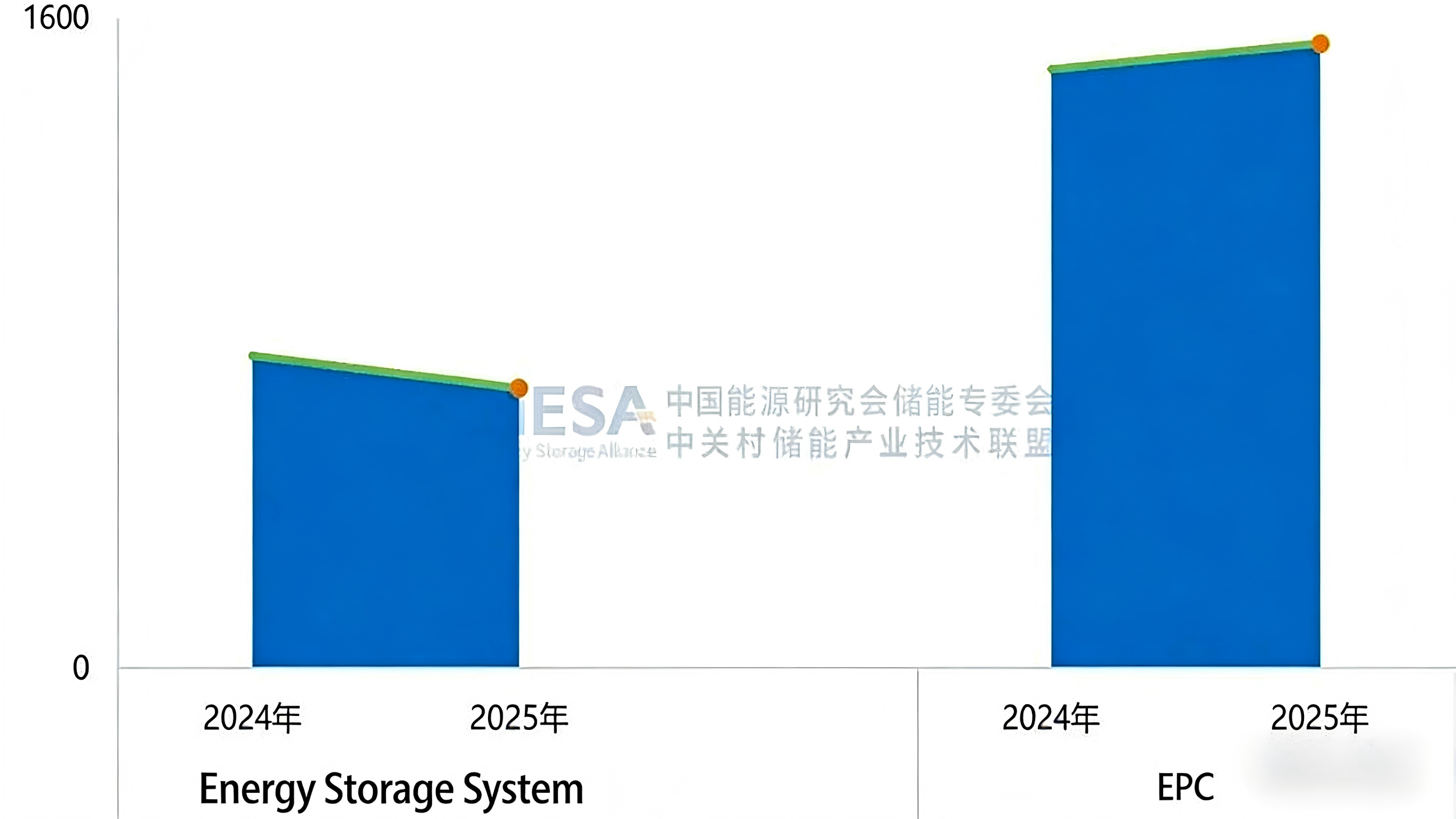

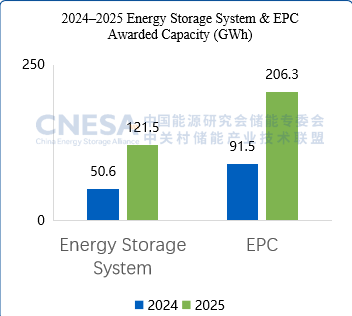

Decline in Energy Storage System Tenders, Increase in EPC Tenders

According to incomplete statistics from CNESA DataLink Global Energy Storage Database,690 energy storage system tender packages (excluding centralized and framework procurement) were issued in 2025, down 10.4% year on year. In contrast, 1,536 EPC tender packages (excluding centralized and framework procurement) were released, representing a 4.5% increase. This shift indicates changing construction preferences in the non-centralized and framework procurement market, with project owners increasingly favoring integrated, turnkey delivery models that outsource construction and risk management.

Winning Bid Volumes for Energy Storage Systems reach 121.5GWh and 206.3GWh for EPC

In 2025, the winning bid volume for energy storage systems (excluding centralized and framework procurement) reached 121.5GWh, up 140.1% year on year. Meanwhile, EPC projects recorded a winning bid volume of 206.3GWh, representing a 125.5% increase.

03. New-Type Energy Storage Policies

High Policy Activity Maintained

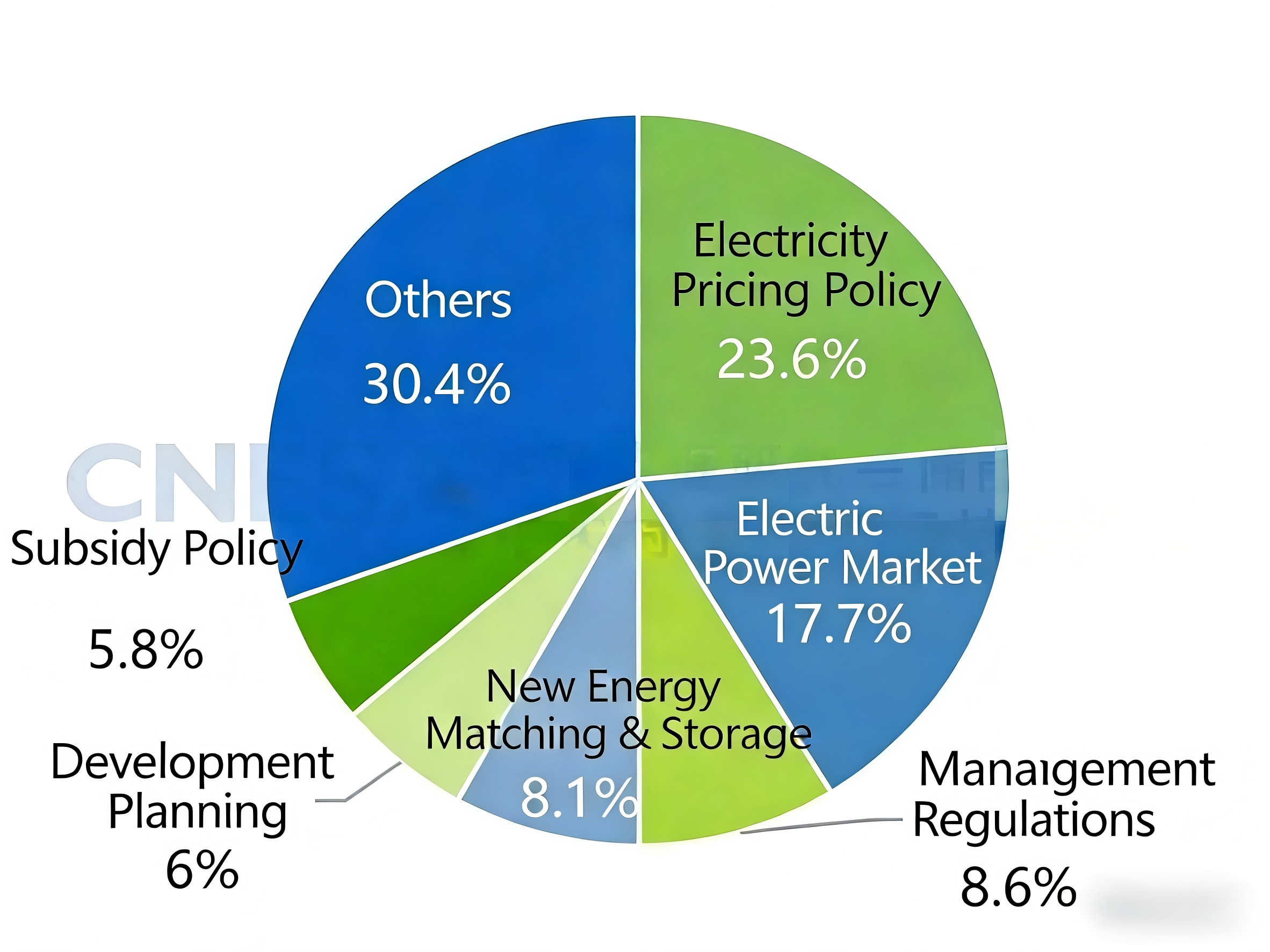

CNESA pays attention to energy storage policy development for a long term and rolled out 869 relevant policies with a year-on-year increase of 13%; Market-oriented reform entered rapid development with electricity pricing and power market policies keeping the heat high and regulatory and management-oriented policies sharing larger proportion.

Many Provinces Have Realized the 14th Five-Year Plan Targets

By the end of 2025, the total installed capacity of provincial new-type energy storage in 14th Five-Year Plan period exceeded 91.6GW. In terms of practical installed capacity, most provinces nationwide have achieved their respective planning targets of the 14th Five-Year Plan.

Commercial and Industrial Energy Storage Moves Toward Marketization, with Cumulative Capacity Expected to Exceed 30GW During the 15th Five-Year Plan

In early 2025, document No. 136 promoted the full market participation of the new energy electricity generation. The medium-and-long-term rules by the end of 2025 canceled artificially prescribed time-of-use pricing for market participants. It can be seen that the load-side users will gradually enter market and commercial and industrial energy storage in 2026 will move towards marketization in phase.

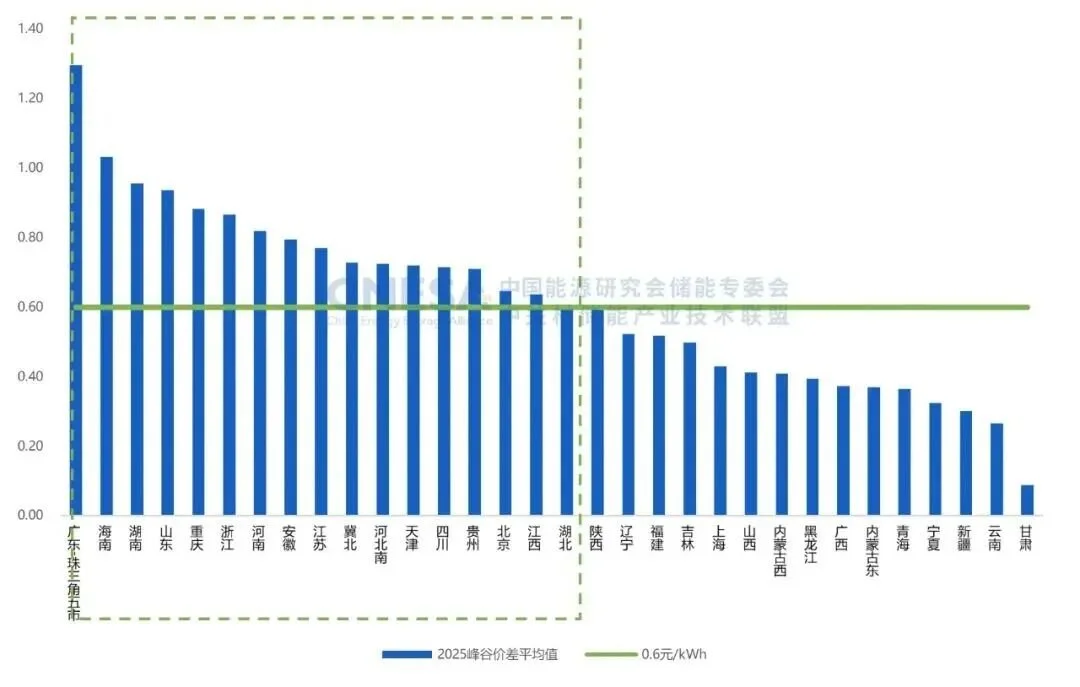

For time-of-use pricing, several places have matched spot market to adjust time-of-use and pricing scope with a general narrowing of price spreads. A majority of regions saw bearish news from the short term. For grid agency purchase electricity price, the average price spread of 32 regions was RMB0.616 per kWh with a year-on-year decrease of 9.4%.

Meanwhile, China encourages commercial and industrial users at 10kv and above to directly participate in the electricity market and gradually narrow the grid agency purchase user scope. Therefore, in the future, the pricing spread arbitrage of commercial and industrial will be decided by the real-time market supply and demand, which is unsustainable only depending on the fixed price spread arbitrage model.

Looking into the 15th Five-Year Plan, commercial and industrial energy storage will keep steady growth with diverse revenue streams, shifting from single “fixed price spread arbitrage model” to “fluctuated market price spread arbitrage+demand charge management+demand response”. The cumulative installed capacity is expected to exceed 30GW.

04.

Outlook for the New-Type Energy Storage

Cumulative installed capacity of new-type energy storage is expected to exceed 370GW by 2030

Looking ahead to the 15th Five-Year Plan, key development trends include:

Policy: New-type energy storage will be driven by market mechanisms, continue to expand new application scenarios and innovate business models together the green value and facilitate the industrial high-quality development.

Technology: The industry has entered a phase of multi-technology coexistence. Diverse energy storage technologies are expected to continue achieving breakthroughs across multiple scenarios and scales throughout the 15th Five-Year Plan period and long-duration energy storage will come into a critical development phase.

Energy Storage Duration: According to CNESA, the average time-spun of cumulative new-type energy storage installations witnessed slow increase between 2021 and 2025 from 2.11 hours to 2.58 hours. From 2026 onwards, the duration growth is expected to speed up evidently, which will reach 3.47 hours by 2030. This change reflects the intensified demand of ongoing technological progress and market for long-duration energy storage. This industry is moving towards in-depth application scenario emphasizing more on energy capacity including energy transfer time and system regulation.

Installation Capacity: Historical statistic shows that China’s new-type energy storage has entered rapid development. Over the past 5 years, the cumulative installation of new-type energy has been 40 times larger. As installed base grows, growth rate slowing down will be definite. Looking into the 15th Five-Year Plan, in spite of moderate development, the large base will continue to generate considerable absolute increase. The cumulative installed capacity in 2030 is expected to exceed 370GW.

Register now to attend Asia’s Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Adress: No. 55 Yudong road, Shunyi District, Beijing China

Amazon buys 1.2GW Sunstone solar-plus-storage project from bankrupt Pine Gate

Annual Power Cost Savings Exceed RMB 60 Million ! Great Power’s 107MW/428MWh Hydropower-based Aluminium User-side Energy Storage Project is Commissioned

RMB 180 Billion! China Southern Power Grid Hit a New High for Investment in 2026

Expanding effective investment is a key lever for stabilizing growth and improving people’s livelihoods. According to China Southern Power Grid, the company has embarked RMB 180 billion for fixed-asset investment in 2026, marking a record high for fifth consecutive year, with an annual growth rate of 9.5%. Investment will be directed primarily toward the development of a new-type power system, the growth of strategic emerging industries and the enhancement of high-quality power supply services, providing solid support for a strong start to the 15th Five-Year Plan period.

CORNEX Secures a 6GWh Energy Storage Order in Egypt, Successfully Expanding Into the North African Market

On January 16th, Cornex New Energy signed a strategic cooperation agreement with Egypt-based partners WeaCan and Kemet.

The agreement was signed by Dai Deming, chairman of Cornex New Energy and Ahmed Salaheldin Abdelwahab Elabd, Chiarman of the Board of Kemet. The signing ceremony was witnessed by Moustafa Kamal Esmat Mahmoud, minister of Egypt’s Ministry of Electricity and Renewable Energy, along with other government officials and senior executives from relevent enterprises.

100MW/200MWh! Sineng Electric Supports Commissioning of Phase I of Nanlang Energy Storage Power Station

The Phase I 100MW/200MWh Nanlang energy storage power station, supplied by Sineng Electric, has now been successfully commissioned and put into operation. As the first large-scale standalone energy storage project on the grid side to be completed and commissioned in Zhongshan, China, the facility not only injects enhanced flexibility into the regional power grid, but establishes efficient and reliable revenue mechanism through an innovative frequency regulation service model.

500MW/200MWh! JD Energy’s First GWh-Level Project Successfully Grid-Connected

In December 2025, the 500MW/2000MWh energy storage project was successfully grid-connected in Dengkou, Inner Mongolia. The energy storage station, standing proudly under the winter sun, is the first GWh-level project delivered by JD Energy. It not only set a new record for the scale of a single project but marked a significant milestone in the company’s development with its outstanding construction achievements.

2025 Marks the First Year of Mass Production for Large Energy Storage Cells! 500Ah+ Mass Deliveries, ESIE 2026 Energy Storage Expo Invites Global Buyers to Explore New Opportunities

2025 marks a pivotal year for the energy storage industry. The large energy storage cells, which were once limited to “theoretical parameters”, will officially bid farewell to the technical competition phase and enter the practical testing stage of capacity release, yield improvement, and project implementation. Leading enterprises like CATL, EVE, Envision, HTHIUM, and SUNWODA have successively achieved mass production and delivery, and with the intensive landing of GWh-level strategic cooperation and accelerated expansion into overseas markets, this marks the transition of large-capacity cells from lab prototypes to commercial applications. The speed at which energy storage systems are evolving to higher energy density and lower cost has far exceeded industry expectations.

Sungrow’s First Energy Storage Plant in the Middle East Launched,with an Annual Capacity of 10 GWh

Egypt has taken a major step toward accelerating its clean energy transition, as Chinese energy storage leader Sungrow and Norwegian renewable developer Scatec partner with the Egyptian government to deliver large-scale solar+storage projects and establish the Middle East’s first battery energy storage manufacturing base, with a planned annual capacity of 10 GWh.

4.8 GWh Installed: Beijing KeRui Supports the Grid Connection of Two Major Grid-Side Energy Storage Projects in Inner Mongolia, Chi

China Mingyang Longyuan’s First 100MW/400MWh High-Voltage Cascade Independent Energy Storage Project Achieves Full-Capacity Grid Connection

Mingyang Longyuan has built a major milestone in China’s energy storage sector with the successful full-capacity grid connection of its first 100MW/400MWh high-voltage cascade independent energy storage project in Ordos, Inner Mongolia. The project’s commissioning highlights the company’s technological strength in large-scale, high-efficiency, and highly reliable energy storage solutions, while reinforcing the critical role of advanced storage systems in supporting grid stability and renewable energy integration.

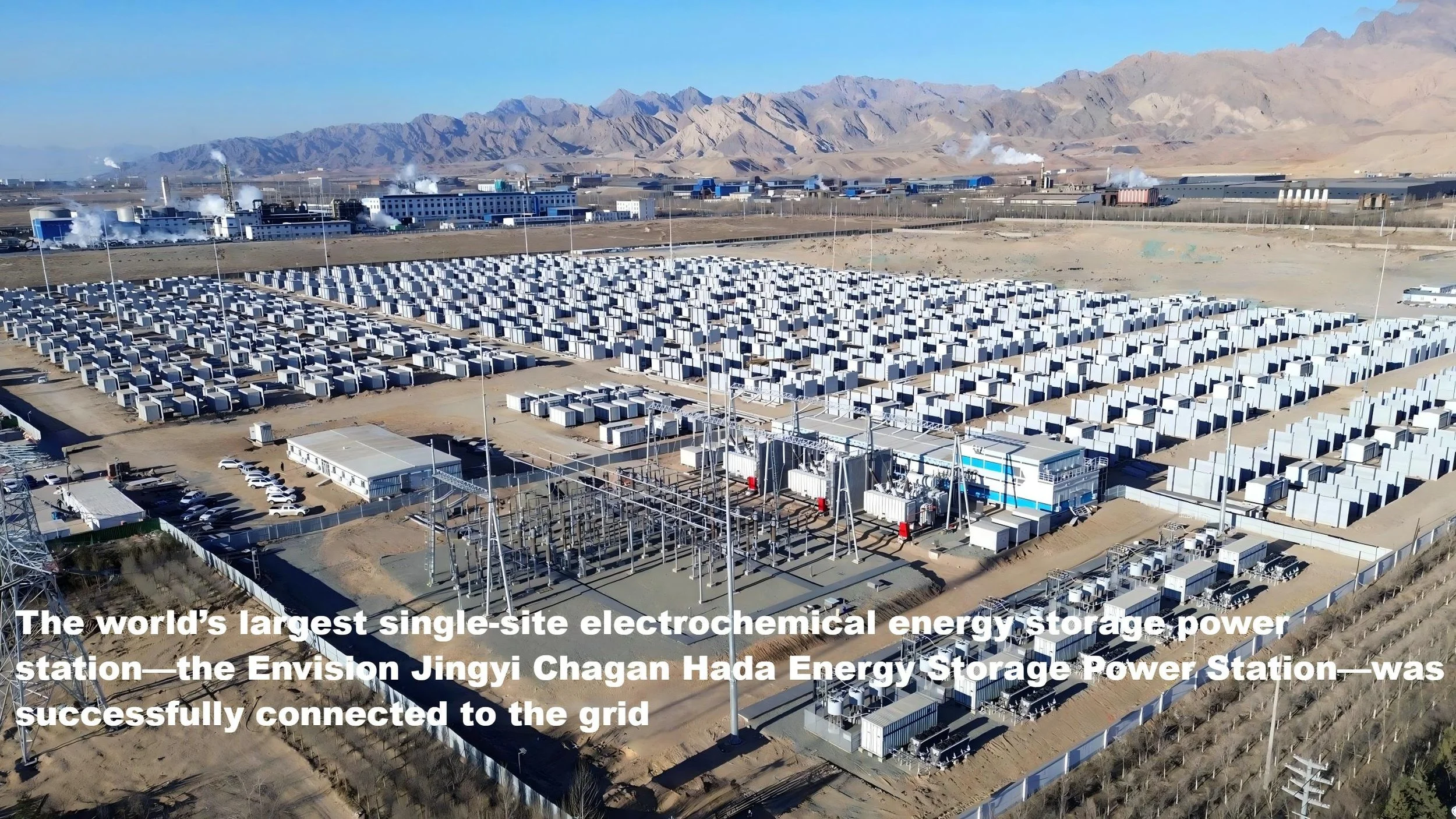

12.8 GWh Energy Storage Cluster Connected to the Grid AI-Powered Energy Storage Reshapes the Future of New Power Systems

The world’s largest single-site electrochemical energy storage power station—the Envision Jingyi Chagan Hada Energy Storage Power Station—was successfully connected to the grid, completing a 12.8 GWh AI-powered energy storage cluster in Inner Mongolia. The project sets new global benchmarks for scale, grid-connection speed, and system reliability, while demonstrating advanced grid-forming capabilities that enable rapid commissioning, deep grid interaction, and large-scale renewable integration.

Google Acquires U.S. Energy Storage Giant for $4.75 Billion

As the global tech giants engage in a frenzied race for AI computing power, a more fundamental battle over “energy supply” is unveiling. Google’s multi-billion dollar power play procured not just an energy storage company but the the “electricity passport” towards the AI-driven future.

I. Blockbuster Acquisition: Acquisition of U.S. Energy Storage Giant for $4.75 Billion

On December 22, Alphabet, Google's parent company, announced that it will acquire Intersect Power, a leading U.S. battery energy storage system developer and operator, for $4.75 billion in cash plus the assumption of debt.

What to watch:

Targeted Assets: The acquisition does not cover the already operational assets but targets its future clean energy power generation projects, data center and energy storage system, totaling 10GWh.

Strategic intention: directly circumvent the crowded traditional grid and build an exclusive “power generation + energy storage” closed loop for AI data center.

The Alphabet CEO said: “ Intersect will help us synchronize the creation of power generation and energy storage system so as to match the added data center load and reshape energy solutions of AI data center.

II. Urgency: The high energy consumption “black hole” of AI data center

It is the tremendous energy pressure alongside generative AI behind the acquisition.

Surge in electricity consumption: the electricity demand is estimated to grow manyfold of data center hubs including State of Texas and California in 2030.

Stringent Reliability requirement: The AI data center requires 99.999% power supply reliability, which is hard to satisfy for traditional grid.

Solutions: Battery Energy Storage System emerges as the key infrastructure to balance the intermittency of renewable energy and achieve 24/7 uninterrupted power supply.

III. Ecological Synergy: Tesla makes an indirect play and broaden the collaboration zone

It is noteworthy that Intersect and Tesla are long-term collaboration partners. Google’s move means Tesla will step into the collaboration zone.

Current collaboration: Many operational energy storage projects of Intersect have employed the Megapack energy storage system of Tesla (like the Oberon 1 GWh project of California)

A huge order: Intersect also signed the 15.3GWh supply contract with Tesla, becoming one of the world’s largest purchasers and operators of this model of energy storage equipment.

IV. Chinese Companies: A head start in the Global data center energy storage arena

In fact, China’s top-tier energy storage companies have identified the opportunities early on, actively expanding their presence in the global “data center + energy storage” sector:

Companies like SUNGROW, SHUANGDENG, HUAWEI, KWLONG, ZTT, NARADA, HTHIUM, ROBESTEC, Potis Edge, Ampace, CLOU, Hopewind, CHNT, KSTAR, Vertiv, DELTA, EATON, VISION, SINEXCEL, JST(JINPAN TECHNOLOGY), TONGFEI, Envicool, Goaland, Shenling, HAIWU and so on has played their respective roles engaging in data center energy construction.

The market demonstrates that China’s supply chain ranging from power sources, battery to management system is becoming an important power to underpin the global AI data center energy transformation.

V. Industry Barometer: the summit forum focuses on “data center + energy storage” future

Google’s acquisition does not stand alone and it points to a global trend: energy storage combined with data center has become the central arena where global technology and energy industry converge.

This trend will be fully represented in the upcoming industry grand.

_____________________________________________________________________________________________

Register now to attend Asia's Largest Energy Storage Trade Show for free:

What: The 14th Energy Storage International Conference & Expo

When: Conferences: March 31 - April 2, 2026

Exhibitions: April 1-3, 2026

Where: CIECC Beijing, China

Address: No. 55 Yudong road, Shunyi District, Beijing China

Breaking Through the Waves and Going Global! Hear the New Expectations from Overseas Markets for China’s Energy Storage

Source: CNESA

On December 3-5, 2025, the 2025 China Energy Storage CEO Summit and the Preliminary Round of the 10th International Energy Storage Innovation Competition, hosted by the China Energy Storage Alliance (CNESA) and co-hosted by Xiamen University, Kehua Digital Energy, and Cornex New Energy, was successfully held in Xiamen.

As CNESA’s flagship concluding event of the year, this summit was anchored in the southeastern coastal region - a strategic hub linking global markets - and was themed “Breaking Waves · Coexisting - Shaping a New Global Energy Storage Ecosystem for 2026.” It brings together senior representatives from energy investment institutions, project developers, asset owners, and EPC companies from Saudi Arabia, Australia, Denmark, Austria, Bulgaria, India, and other countries for in-depth engagement.

International guests focused on topics including project implementation, cooperation models with Chinese companies, grid connection and interconnection standards, and industrial chain collaboration, collectively presenting the global market's genuine expectations of - and directions for cooperation with - China's energy storage industry.

Europe:

Focusing on building long-term partnerships rather than

engaging in short-term transactions.

Renalfa IPP - Chief Investment Officer (Austria / Bulgaria)

Kalina Pelovska

Renalfa IPP is a leading independent power producer in Europe, with more than 5.6 GW of renewable energy assets deployed across Central and Eastern Europe.

“Investment decision-making has evolved from a singular focus on levelized cost of energy to a comprehensive evaluation of system reliability and revenue stability. The strengths of Chinese energy storage companies are expanding from pricing advantages to delivery efficiency, technical responsiveness, and long-term stability. We look forward to jointly cultivating the Central and Eastern European (CEE) energy storage asset market with Chinese companies through joint ventures and co-investment models, building long-term partnerships.”

Solarpro Technology AD - Head of Energy Storage Division (Bulgaria)

Gabriel Nenov

Solarpro is a major EPC contractor and energy storage project developer in Southeast Europe, with extensive experience in PV+BESS projects across Bulgaria, Romania, Greece, and other countries.

“The energy storage market in Eastern Europe is rapidly taking off, but complex grid-connection rules and diverse approval processes place very high demands on information transparency and depth of technical communication. Large-scale projects of 200 MWh and above are becoming mainstream. The Eastern European energy storage market is optimistic about deep collaboration with Chinese partners at the inverter, battery cell, and EMS integration levels. Through standards alignment and early-stage design coordination, project bankability and execution certainty can be significantly improved.”

Australia:

Not Just Batteries, but “Plug-and-Play” System Solutions

Green Gold Energy - Head of Energy Engineering Department (Australia)

Alessandro Wei

Green Gold Energy is a leading renewable energy developer and EPC contractor in Australia, with extensive experience in developing large-scale photovoltaic and battery energy storage projects across South Australia, New South Wales, Victoria, and other regions.

“In the Australian market, the Chinese energy storage supply chain has already built a high level of trust. Looking ahead, there is a stronger expectation for entry through system-level solutions rather than standalone equipment - integrated coordination across PCS, BMS, EMS, and grid-connection models. Australia’s energy storage business model is shifting from frequency regulation-led applications to a parallel model combining medium- to long-duration energy storage arbitrage and capacity assurance, placing higher demands on overall system compliance, long-term O&M capabilities, and localized services. Grid-forming technologies, validation of grid-connection models, and technical confirmation prior to tendering will become key levers for China-Australia collaboration.”

Middle East:

Focusing on long-duration energy storage and system integration

capabilities

Aramco Ventures - President of China Strategic Investments (Saudi Arabia)

Rongtao Sun

Aramco Ventures, the strategic investment arm of Saudi Aramco - the world's largest energy company - is accelerating its global investments in renewable energy, hydrogen, energy storage, and advanced materials.

“The global energy system is rapidly evolving toward a more diversified structure, with energy storage becoming a critical foundational asset. Large-scale energy base projects in the Middle East and North Africa impose higher thresholds for long-duration energy storage, system integration capabilities, and project-level reliability. China holds significant advantages in energy storage manufacturing capacity, industrial clustering, and supply chain completeness. Going forward, we will pay closer attention to the maturity of Chinese energy storage companies in safety standards, long-term operations and maintenance, project documentation systems, and global delivery capabilities. Through joint investments, demonstration projects, and localized deployment, we aim to promote deeper levels of cooperation.”

Nordic Region:

Strong emphasis on full life-cycle services and close coordination

with the power grid

DRSOLAR Denmark ApS - Chief Executive Officer (Denmark)

Salomon Martens

DRSOLAR is a Danish renewable energy system integrator and distributor, with long-term engagement in battery energy storage sales and system services across Nordic and European markets.

“In Denmark and the broader Nordic region, demand for energy storage is shifting from simple grid-connection support to system services and flexibility resources. The market increasingly emphasizes system safety, full life-cycle services, and the ability to collaborate with grid operators. Chinese energy storage products are competitive in performance and delivery. If further alignment can be achieved in certification standards, after-sales systems, and localized technical support, their market penetration will be significantly strengthened.”

RJS Construction ApS - Chief Operating Officer (Denmark)

Robert Kraszewski

RJS Construction is a Danish engineering and EPC service provider involved in the construction and delivery of multiple renewable energy and energy storage projects across Europe.

“From an EPC perspective, European projects place greater emphasis on engineering feasibility and on-site adaptability. Energy storage systems must fully consider construction, commissioning, and O&M conditions during the design phase. Chinese companies perform strongly in modular design and manufacturing efficiency. If closer coordination can be established with local EPC teams, project delivery efficiency can be significantly improved while risks are better controlled.”

India:

Seeking Partners to Scale from Pilot Projects to Full Deployment

At the Energy Storage CEO Summit, representatives of Coca-Cola’s Indian bottling operations expressed clear interest in collaboration. Their purpose for attending was highly practical: “In India, energy storage is booming, so we want to explore this for our company.”

Their demand stems directly from the company’s energy transition efforts. They have already built dedicated solar power plants for their own operations, and their current focus is to use battery energy storage systems to replace grid electricity during peak hours, achieving a better balance between solar generation and energy storage.

Regarding cooperation, they outlined a clear roadmap: “Maybe we can start the pilot project in India. And once if we will find it good, we would scale it up in India and do a business over there with the help of China.” They also explicitly noted that they regard the China Energy Storage Alliance (CNESA) as an important support platform in this field and attended the summit specifically to seek connections through CNESA.

As a key prelude to the 14th Energy Storage International Conference & Expo (ESIE 2026), this year’s China Energy Storage CEO Summit delivered a clear message through its high level of international participation and practice-oriented agenda: the global market not only recognizes China’s manufacturing strength in energy storage, but also expects deeper collaboration across technology standards, ecosystem development, and long-term value creation.

As Chinese energy storage companies further integrate into the global energy system, a new ecosystem built on co-creation, co-development, and shared growth is taking shape. This is no longer merely about exporting products, but a collective journey of technologies, standards, and cooperative models going global together.

CENSA Upcoming Events:

Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Dec 31, 2025.

Countdown: 100 Days to Go! - ESIE 2026 Energy Storage Expo Announces First Batch of Exhibitors

Source: CNESA

The 14th Energy Storage International Conference & Expo (ESIE 2026)

March 31 - April 3, 2026

Capital International Exhibition & Convention Center, Beijing, China

With just 100 days remaining until the opening of the 14th Energy Storage International Conference & Expo (ESIE 2026), anticipation across the industry continues to build. Momentum is accelerating, and companies are actively registering to exhibit.

As exhibitor recruitment enters its final countdown, this landmark event - designed to build industry consensus, drive technological innovation, and foster global exchange - warmly invites energy storage professionals worldwide to gather in Beijing.

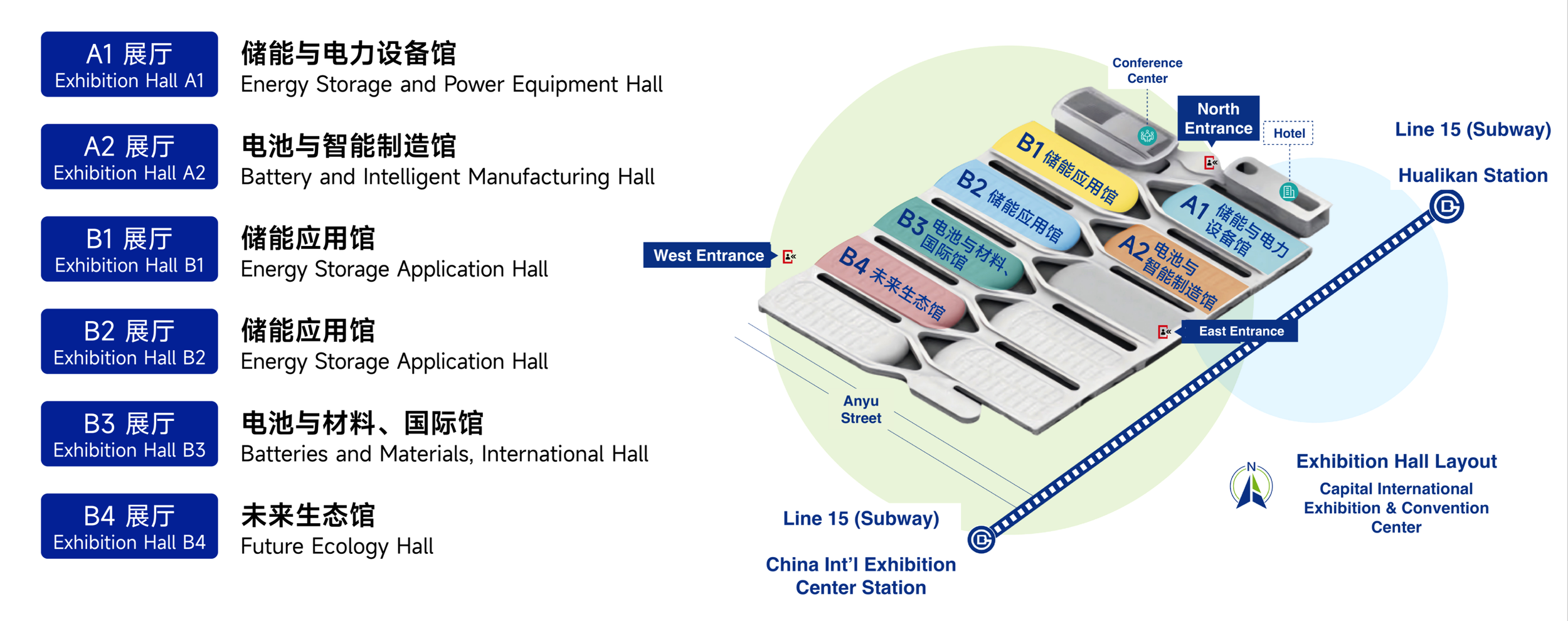

Exhibition Overview

ESIE 2026 will feature 6 themed exhibition halls:

Energy Storage & Power Equipment Hall

Battery & Intelligent Manufacturing Hall

2 Energy Storage Application Halls

Battery & Materials, International Hall

Future Ecology Hall

In addition, 9 specialized zones will be set up, covering:

power equipment, zero-carbon industrial parks, data centers, EV charging infrastructure, fire safety, intelligent manufacturing, hydrogen energy, materials, and testing & certification.

Together, the exhibition comprehensively covers enterprises across the entire upstream and downstream energy storage industry chain.

Figure | Layout Plan of the 14th Energy Storage International Conference & Expo

A1 - Energy Storage & Power Equipment Hall

Well-known brands exhibiting include: HyperStrong, EVE Energy, Zhongqi New Energy, Pengcheng Infinite, CLOU, Zhongchu Guoneng, Great Power, Inpai Battery, Huadian Heavy Industries, Hongzheng Energy Storage, Chint Electrics, Guodian Nanjing Automation, Elecnova, Envicool, Qianye Technology, Tiansu, Futronics, Dafu Integrated Equipment Technology, UTL Electrical, Winsure Communication, Sanwo Liyuan, Fans-tech Electrical, Kait, Qingyuan HeYi, YNTECH, Regal Rexnord, and more.

A2 - Battery & Intelligent Manufacturing Hall

Exhibitors include: CATL, Soaring Electric, XYZ Storage, Kehua Digital Energy, Cornex, Sineng Electric, NR Electric, AlphaESS, Hopewind, Ampace, Nebula Electronics, Autowell, Gaodengsai Energy, RelyEZ, Phoenix Contact, Youxing Shark, Lead Technology, Iron Man Fire Fighting, RePower Technology, Kelvin New Energy, Huasi Systems, Ligoo New Energy, Zonzsin, Tangent, Xenbo Heat Sink, Ubetter, Yaliqu, Heidun Cloud, Luoweite, National Center for Advanced Energy Storage Product Quality Inspection & Testing, Balance Intelligent Fire, and others.

B1 - Energy Storage Application Hall

Participating companies include: CRRC Zhuzhou Institute, Gotion High-Tech, Goldwind, Huawei, Sunwoda, Hoymiles, Hithium, Ganfeng, KE Electric & Hisense, Pylontech, Zhiguang Energy Storage, Liangxin Electrical, Ancheng New Energy, Xingchen New Energy, Gold Electronic, TCL, PULSST, Advantech, Chuancheng Energy Storage, SAV, SGS-CSTC Standards, TYT, Xinyuan Tech, Enerflow, Hysea, Stif, TIG Technology, Candera, TYES Energy Storage, among others.

B2 - Energy Storage Application Hall

Exhibitors include: Sungrow, CALB, Narada, REPT BATTERO Energy, Robestec, Windey Energy, iPotisEdge, TONGFEI, Siyuan Electric, Dongfang Electric, InfyPower, Xiqing, HYXiPOWER, Kgooer, Xiamen Hongfa, Qualtech, REsource Electric, HIGEE, State Energy XinControl, Beijing Micro Control Industrial Gateway Technology, Rongke Power, BMSER, Sinofuse, Southern CIMC, EMKA (Tianjin), Lanrui Electric, Hecheng Smart Electric, ZONZEN, Kefa Electronics, and more.

B3 - Battery & Materials, International Hall

Exhibitors include: Shuangdeng Group, Megarevo, Concord New Energy, Kstar, GoodWe, ZTT, Wocheng, Sigenergy, German Pavilion, Suqian Times, CVC Testing, SHENG YANG Electric, Heyuan Magnetics, Shentong Mechanical & Electrical, TOPOS, Honghaisheng, Dianwei, Carbon Energy Technology, WILO SE, Cergen New Energy, Longxiang Rubber, Onpow Push Button, Hefei Zhiyou Electric, WSF, CHEVRON Electronic, and others.

B4 - Future Ecology Hall

Exhibitors include: Envision Storage, BYD, Trina Storage, Singularity Energy, Longking, CSG Energy Storage, Jinko, State Power Rixin Technology, Contemporary Nebula Energy Technology, iBatteryCloud, Gresgying, CSG Technology, Wincell, ESF Technology, Sino Group, and more.

One-Stop Access to Cross-Sector Energy Storage Innovations

Visitors can explore a wide range of integrated application scenarios, including:

Energy Storage + Industry: Steel, cement, chemicals, petroleum, aluminum, coal, oilfields, and more - discover how energy-intensive enterprises reduce costs and improve efficiency with storage solutions.

Energy Storage + Wind & Solar: BIPV storage, CIPV storage, source-grid-load-storage integration, PV-storage-DC-flexible systems - all solutions for coordinated renewable and storage development.

Energy Storage + Desert & Gobi Mega Bases: Wind-solar-storage bundled transmission, grid-forming storage, multi-energy complementarity (wind + solar + storage + coal/solar thermal), and ecological desert control - unlock efficient desert energy utilization.

Energy Storage + Zero-Carbon Parks / Green Power Direct Supply: Microgrids, distributed PV-storage consumption, dedicated green power lines, peak-valley arbitrage, emergency backup, and green power traceability - ensuring stable green electricity supply.

Energy Storage + Data Centers / Telecom Base Stations: Backup power, peak-valley arbitrage, off-grid power supply, and green power integration - supporting stable and cost-efficient digital infrastructure.

Smart Energy: Smart grids, microgrids, virtual power plants, distributed energy management systems, and energy IoT platforms - key tools for future energy management.

Energy Storage + Transportation: Vehicle-to-grid interaction, charging and swapping facilities, PV-storage-charging stations, EVs, electric heavy trucks, low-altitude economy, and new energy solutions for ports and airports.

Innovative Energy Storage Technologies: Hydrogen energy; chemical storage (sodium-ion, solid-state, aqueous, all-vanadium flow, etc.); physical storage (compressed air, flywheel, gravity, molten salt, etc.).

Preparations for ESIE 2026 have entered the full-scale sprint phase. The organizing committee is advancing all work in a coordinated and efficient manner to deliver a high-level professional exchange platform for the industry.

Exhibition booths are now in short supply, with only a limited number of premium locations remaining. Energy storage enterprises across the entire value chain are warmly invited to join ESIE 2026 - uniting around technological innovation, advancing industrial upgrading, and jointly shaping a high-quality future for the new energy storage industry.

Register Now to attend, free before Dec 31, 2025:

https://mailchi.mp/2a7b423a7efb/esie-2026-registration-socialmedia

New Installations Down 67% YoY: Analysis of China's User-Side New Energy Storage Projects in November

Source: CNESA

In November 2025, newly installed user-side new energy storage capacity in China recorded a year-on-year decline of over 65%.

Compared with October, the market structure showed notable adjustments:

Commercial and industrial (C&I) energy storage accounted for nearly 90%, while long-duration energy storage technologies accelerated deployment.

East China contributed more than half of newly commissioned capacity, with Fujian leading in installed capacity.

Although filing activity in traditional user-side markets (Zhejiang, Guangdong, Jiangsu) declined compared with the same period last year, overall demand remained higher year-on-year. Emerging markets such as Anhui, Henan, and Sichuan are becoming new growth engines driving the national user-side energy storage market.

Analysis of User-Side New Energy Storage Projects in November

In November, newly installed user-side capacity reached 185.27 MW / 555.83 MWh, representing -67% / -57% year-on-year, and -5% / +16% month-on-month. User-side new energy storage projects exhibited the following characteristics:

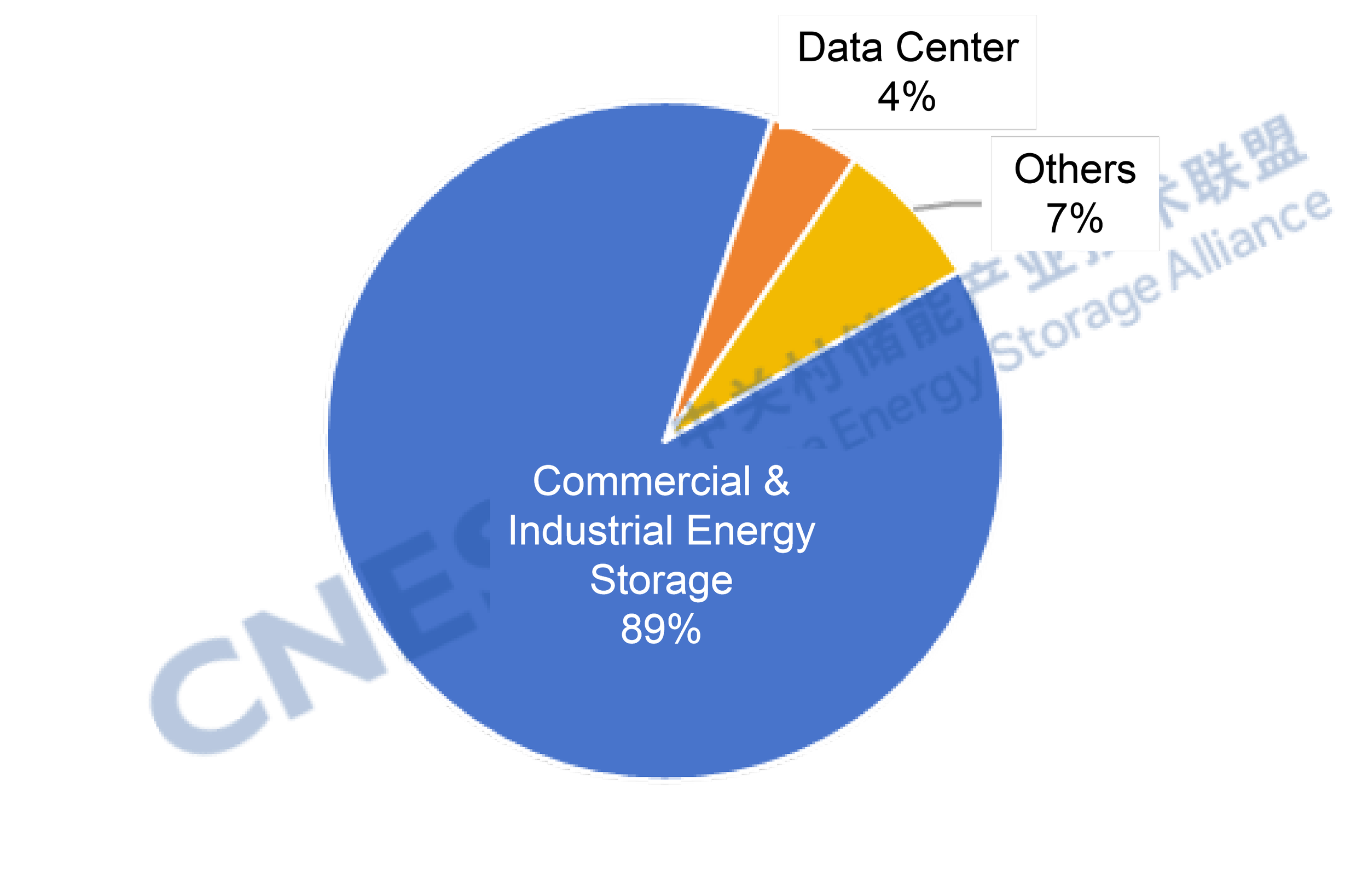

(1) Installed Capacity by Application

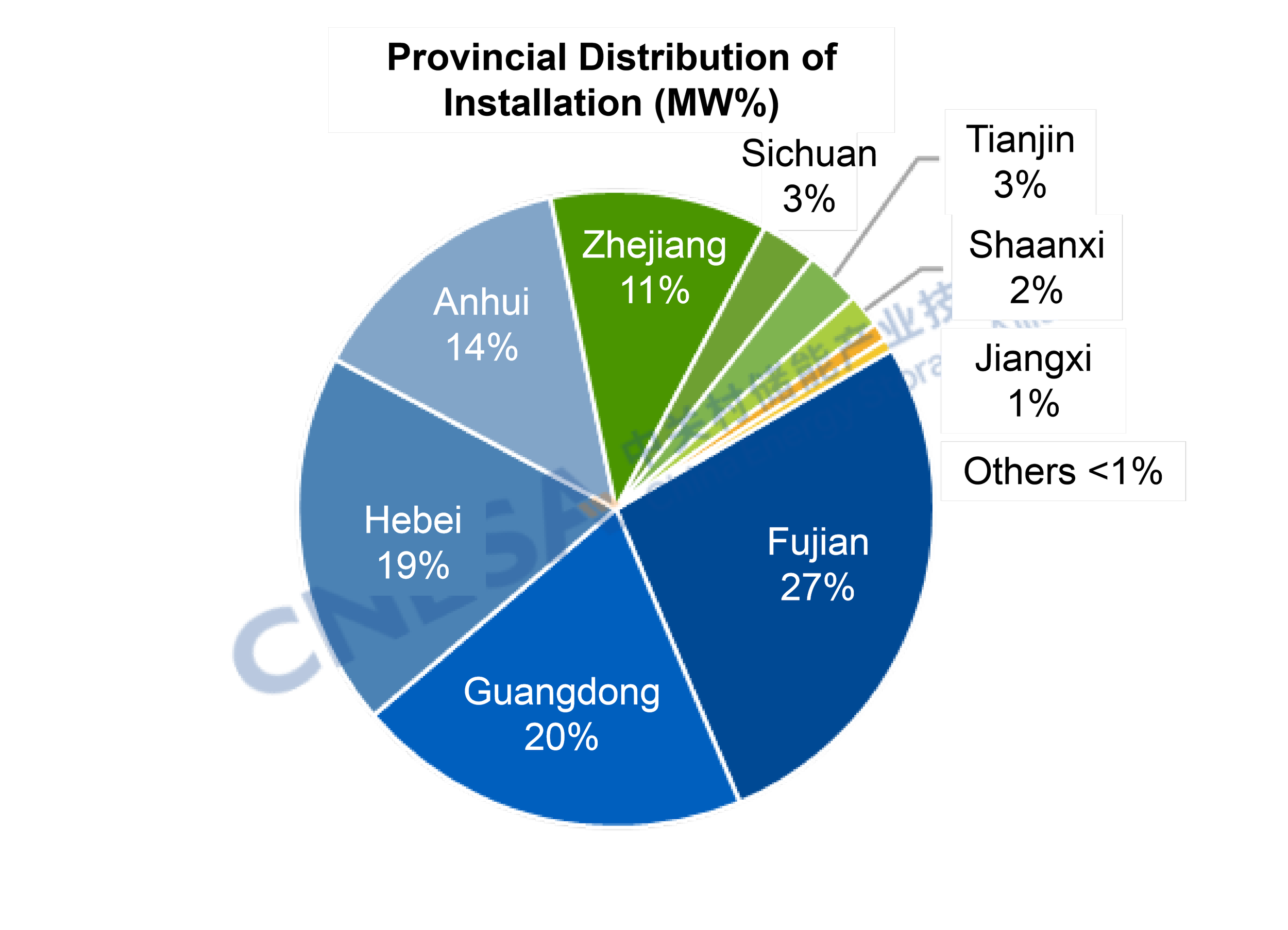

In November, the user-side energy storage market continued to be dominated by C&I applications, accounting for nearly 90% of total installations. Newly installed C&I capacity reached 163.9 MW / 541.3 MWh, -68% / -58% year-on-year, and -9% / +15% month-on-month.

The largest data center user-side energy storage project in Zhejiang was officially commissioned. Rapid development of AI data centers (AIDC) and intelligent computing centers is driving growth in user-side energy storage demand.

From a technology perspective, all newly commissioned projects adopted electrochemical energy storage technologies. Lithium iron phosphate (LFP) batteries accounted for over 99% of installed power capacity. In terms of long-duration storage, one 8-hour, 202 MWh lithium-based C&I energy storage project and one 8-hour, 2 MWh all-vanadium redox flow battery project were completed and put into operation.

Figure 1: Application Distribution of Newly Commissioned User-Side New Energy Storage Projects in November 2025 (MW%)

Data Source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: “C&I” includes industrial facilities, industrial parks, and commercial buildings. “Others” include mining areas, oilfields, remote regions, and municipal institutions, etc.

(2) Regional Distribution of User-Side Energy Storage

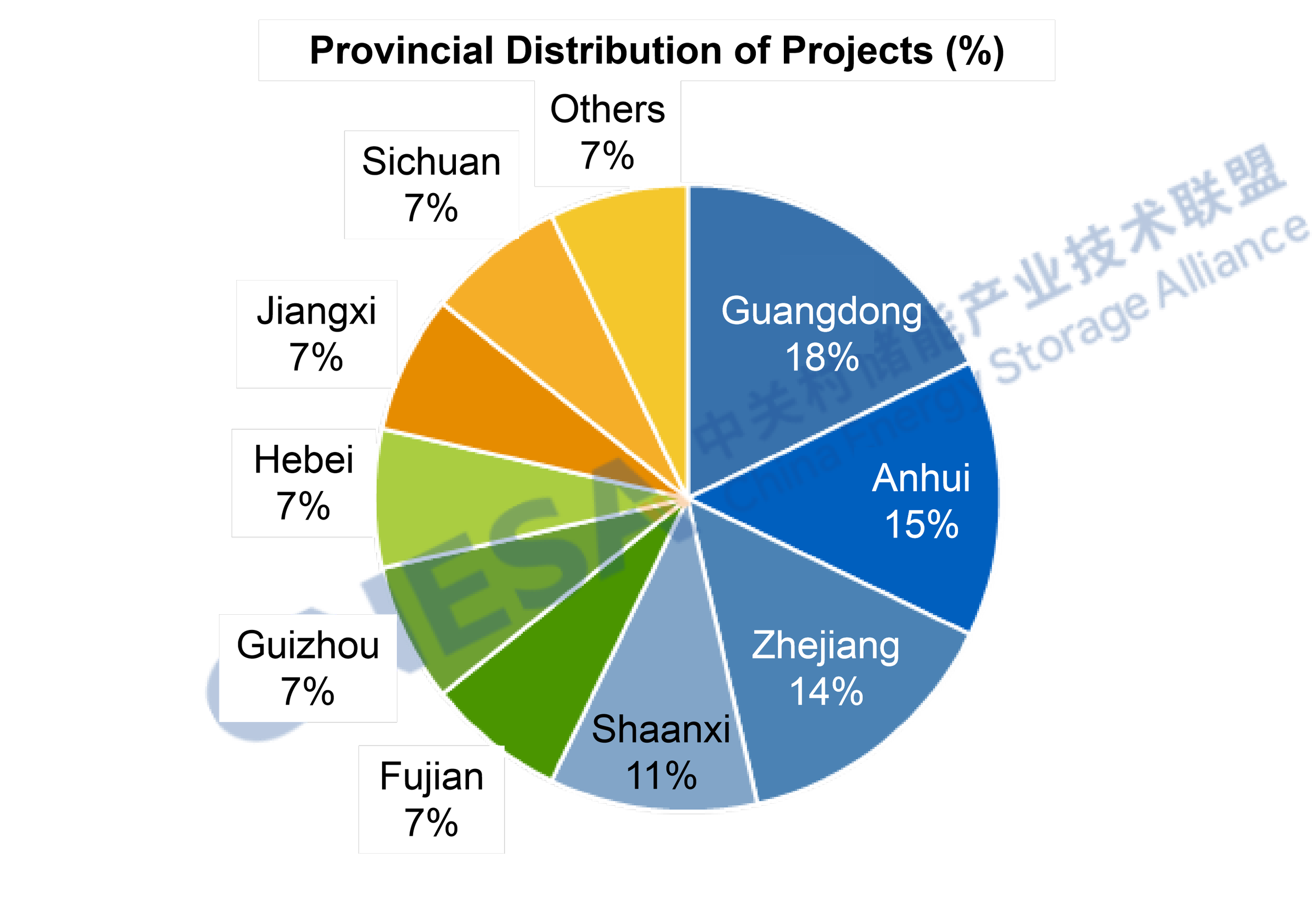

By region, newly commissioned projects were mainly distributed across 11 provinces, including Fujian, Guangdong, Hebei, Anhui, and Zhejiang. East China led the market in November, accounting for 52% of newly installed capacity and 39% of total projects, ranking first nationwide in both installed scale and number of commissioned projects.

At the provincial level, Fujian recorded the largest share of newly installed power capacity, exceeding 25%, while Hebei led in newly installed energy capacity, accounting for 40%. Guangdong had the highest number of newly commissioned projects, representing over 18%, ranking first nationwide.

Fujian hosts a high concentration of energy-intensive industries such as steel and chemicals, where demand for peak shaving, valley filling, and backup power is strong. In addition, diversified application scenarios - including integrated PV-storage-charging systems and virtual power plant aggregation - are being increasingly developed, leaving substantial growth potential for the user-side energy storage market.

From an industrial and supply chain perspective, Fujian is home to the country's largest lithium battery R&D and manufacturing base, with lithium battery production capacity ranking among the national leaders. Driven by leading energy storage companies, a complete local supply chain has been established for core components such as cells, PCS, BMS, and EMS, effectively reducing overall system costs. Moreover, Fujian supports energy storage project financing through green credit and industrial funds, covering multiple project types including pumped hydro storage and new energy storage.

Figure 2: Provincial Distribution of Newly Operating User-Side New Energy Storage Projects in China, November 2025

Data Source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

(3) Filed User-Side Energy Storage Projects

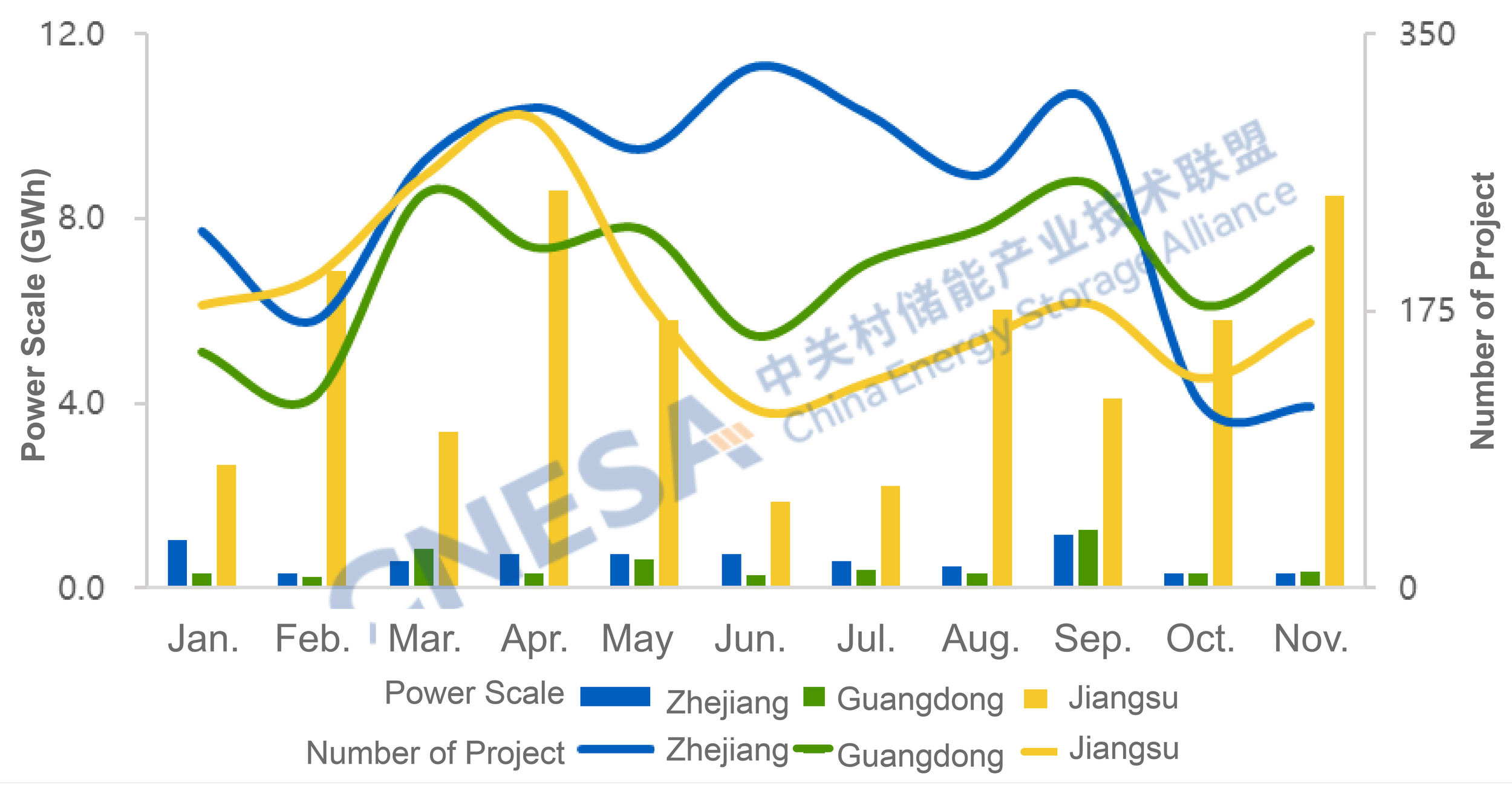

Based on project filings, national user-side market demand in November exceeded the level of the same period last year, with differentiated regional adjustments. Nationwide, both the total scale and number of newly filed user-side projects in November were higher year-on-year, up 8% and 5%, respectively. However, filing activity in traditional markets - Zhejiang, Guangdong, and Jiangsu - declined compared with last year.

Across these three provinces, a total of 497 new projects were filed, down 47% year-on-year, while energy capacity declined 7% year-on-year.

Guangdong recorded the highest number of newly filed projects, but project count fell 25% year-on-year, and scale declined 73%.

Zhejiang saw the largest drop in project count, down 65% year-on-year, with scale decreasing 34%.

Jiangsu recorded a 48% year-on-year decline in project count, but project scale increased 6%.

In November, Jiangsu ranked first nationwide in newly filed project scale. The average project size was approximately twice that of the same period last year, indicating a shift in user-side energy storage development from small-scale, distributed projects toward large-scale, centralized investments in high-quality application scenarios.

Meanwhile, Anhui, Henan, and Sichuan collectively added 440 newly filed projects, up 89% year-on-year and 47% month-on-month, accounting for about 38% of the national total, 5 percentage points higher than in October. Emerging user-side markets represented by Anhui, Henan, and Sichuan are rapidly releasing growth potential and are expected to become new engines driving nationwide user-side energy storage market growth.

Figure 3: Monthly Distribution of Newly Filed Energy Storage Project Scale in Zhejiang, Guangdong, and Jiangsu (January - November 2025)

Data Source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Overall Analysis of New Energy Storage Projects in November

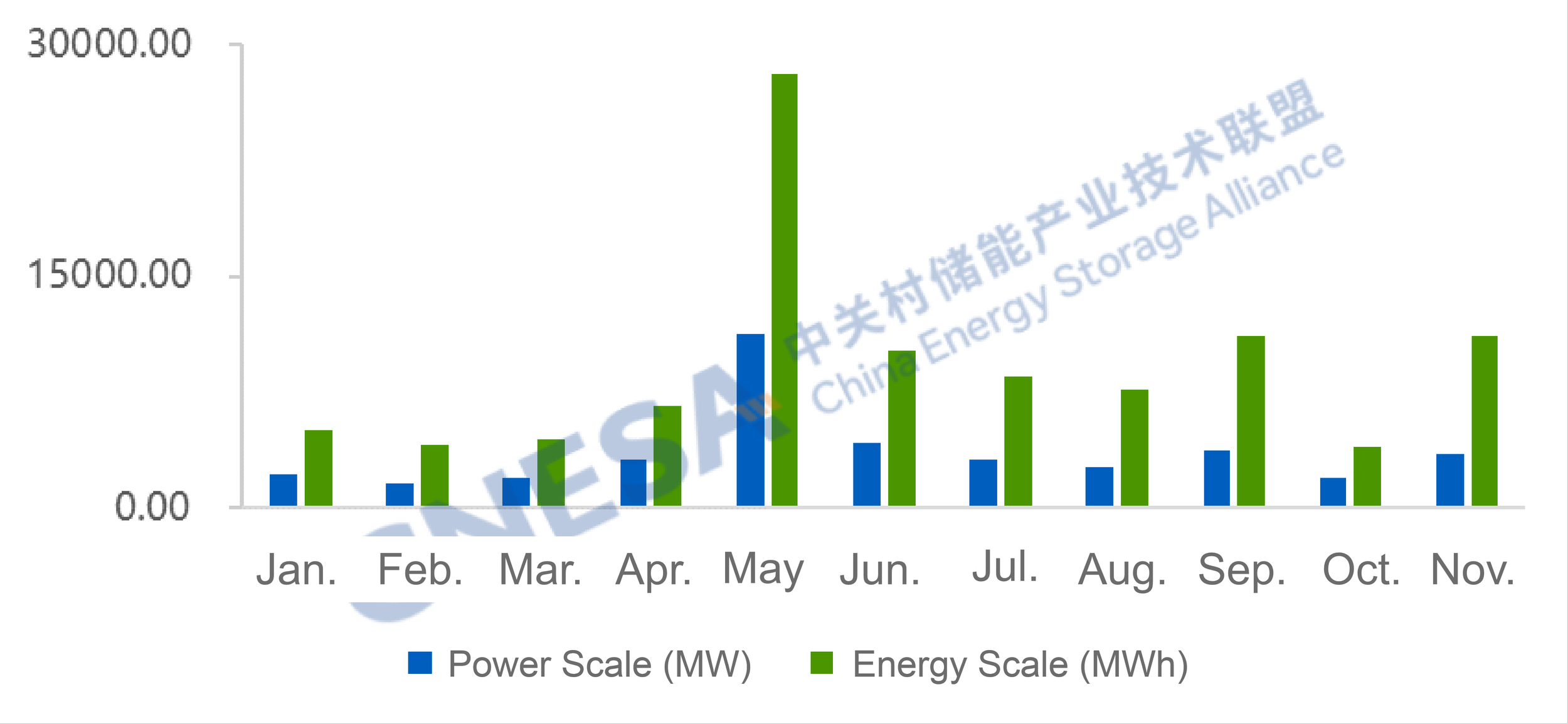

According to incomplete statistics from CNESA, in November 2025, newly commissioned new energy storage projects in China totaled 3.51 GW / 11.18 GWh, representing -22% / -7% year-on-year, and +81% / +180% month-on-month. While monthly additions continued to decline year-on-year, cumulative newly installed capacity in the first eleven months reached 39.5 GW, up 28% year-on-year. Considering the potential for concentrated grid connections ahead of the “12.30” commissioning deadline, total new installations for the year are expected to exceed last year's level.

Figure 4: Installed Capacity of Newly Operating New Energy Storage Projects in China, January - November 2025

Data Source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: Year-on-year comparisons are based on the same period of the previous year; month-on-month comparisons are based on the immediately preceding statistical period.

The China Energy Storage Alliance (CNESA) has consistently adhered to standardized, timely, and comprehensive information collection practices to continuously track developments in energy storage projects. Leveraging its long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses on installed energy storage capacity, providing valuable references for industry decision-making. Since June 2025, the monthly energy storage project analysis has been divided into two sections: “Grid&Source-Side Market” and “User-Side Market”. This issue focuses on interpreting the user-side market in November.

CENSA Upcoming Events:

Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Dec 31, 2025.

Major Report Released: Research on Business Models for the Development of Distributed Energy Storage

On December 16, the Natural Resources Defense Council (NRDC) and the China Energy Storage Alliance (CNESA) jointly held a seminar in Beijing and officially released the report “Research on Business Models for the Development of Distributed Energy Storage.”

Experts participating in the seminar included Wang Shuyang, Deputy Director of the Supply–Demand Interaction Division of the Energy Consumption Research Institute at the China Electric Power Research Institute; Peng Kuankuan, Deputy General Manager of Domestic Marketing at Shanghai Pylon Technology Co., Ltd.; Gao Zhiyuan, Marketing Director of XYZ Storage (Beijing) Co., Ltd.; and Zhang Mingjun, Project Manager and Deputy Dean of the Virtual Power Plant Research Institute at Shanxi Fengxing Measurement & Control Co., Ltd., among others.

Distributed energy storage refers to small-scale energy storage systems deployed on the user side (such as households, factories, and shopping malls), on the distribution network side, or near distributed renewable energy sources. Compared with centralized energy storage, individual distributed storage projects are relatively small in scale, and overall growth has been slower than that of centralized storage.

However, as China further strengthens requirements for the local consumption of renewable energy, distributed energy storage is gradually becoming a key solution to addressing challenges related to nearby renewable energy absorption. Distributed energy storage can store surplus electricity locally, smooth output fluctuations, and significantly improve local renewable energy self-consumption rates and distribution network hosting capacity.

The report “Research on Business Models for the Development of Distributed Energy Storage” analyzes the current business models and major challenges facing distributed energy storage in China. Drawing on international experience and China’s power market development status, the report explores potential directions for business model innovation and proposes recommendations for improving supporting mechanisms.

📎 Report access link:

https://www.esresearch.com.cn/pdf/get_watermark/?id=418&type=report&file=remark_file

In recent years, driven by the declining construction and operating costs of new-type energy storage, the large-scale development and utilization of distributed energy resources, and a series of supportive policy measures, the development of distributed energy storage in China has accelerated significantly. From 2019 to the first three quarters of 2025, China’s cumulative installed capacity of distributed energy storage increased by more than fivefold, rising from 570 MW to 3,638 MW. Six major application scenarios have taken shape, including commercial and industrial (C&I) energy storage, distributed photovoltaic (PV) plus storage, green power direct supply, distribution transformer area energy storage , virtual power plants (VPPs), and energy storage paired with EV charging and battery swapping stations.

Among these, C&I energy storage is the most mature application scenario, primarily relying on time-of-use (TOU) electricity price arbitrage. However, its economic performance is highly sensitive to provincial peak–valley price spread policies. Distributed PV plus storage can be divided into source-side and load-side configurations: source-side projects are typically full-grid-connection projects that mainly participate in market-based electricity trading, while load-side systems are primarily used to improve self-consumption rates and capture TOU price arbitrage opportunities. Green power direct supply projects include both grid-connected and off-grid models. In grid-connected projects, energy storage serves dual functions by reducing renewable energy curtailment and enabling TOU price arbitrage, whereas in off-grid projects, storage plays a combined role in minimizing curtailment and ensuring power supply reliability. distribution transformer area energy storage focuses on dynamic capacity expansion and is mostly implemented as grid-led demonstration projects. Virtual power plants enhance system flexibility by aggregating distributed energy storage resources and participating in demand response, energy markets, and ancillary service markets. Energy storage deployed at EV charging and battery swapping stations primarily targets transformer capacity expansion and peak–valley price arbitrage. Overall, however, distributed energy storage business models in China remain at an exploratory stage and face multiple challenges, including insufficient policy continuity, limited and single revenue streams, incomplete safety standards and operation & maintenance systems, and the absence of effective cost recovery mechanisms.

To enhance the utilization rate and economic performance of distributed energy storage, and to promote its diversified and market-oriented development, the report recommends that during the period 2025–2027, priority should be given to reasonably widening time-of-use (TOU) electricity price peak–valley spreads, improving demand response mechanisms, strengthening safety standards, and enhancing fiscal and tax support, so as to ensure basic project revenues and safe operation of distributed energy storage systems. During the period 2028–2030, efforts should focus on deepening power market reforms, including improving dynamic TOU pricing adjustment mechanisms, promoting the participation of distributed energy storage in spot electricity markets, and exploring the monetization of capacity value and ancillary service value of distributed energy storage. At the same time, greater emphasis should be placed on unlocking the environmental value potential of distributed energy storage in areas such as green electricity, green certificates, and carbon markets, with the ultimate goal of establishing diversified revenue streams and comprehensively enhancing the economic viability and market competitiveness of distributed energy storage.

Liu Wei, Secretary General of the China Energy Storage Alliance (CNESA), stated that distributed energy storage, as a critical link connecting power generation, the grid, and end users, is gradually transitioning from pilot demonstrations to large-scale deployment, and has become an important driving force for energy transition, enhancing grid flexibility, and improving user-side power resilience. However, distributed energy storage still faces challenges such as limited application scenarios, imperfect market mechanisms, and immature business models. CNESA will continue to leverage its platform advantages to promote the integration of policy, technology, and markets, and work together with all stakeholders to build a sound industrial ecosystem for the development of distributed energy storage, thereby supporting the achievement of China’s dual-carbon goals.

Experts from the IEEE PES International Subcommittee on Electrical Energy Storage Markets and Planning noted that, with continued improvements in technology, economics, and safety, distributed energy storage will see widespread deployment during the 15th Five-Year Plan period, and will play a key supporting role in the development of China’s new power system and the enhancement of overall national competitiveness.Looking ahead, the future development of distributed energy storage will increasingly focus on its core value attributes, fully leveraging its technical advantages and value potential to support the safe and stable construction of localized power grids, and gradually evolving from the traditional single arbitrage-based model toward source–load interaction models.

According to the expert, the evolution of distributed energy storage will exhibit five major characteristics:

First, market-oriented development.

Future investments in distributed energy storage will be increasingly market-driven and more diversified. Market participants will include renewable energy investors, load-side enterprises, as well as financial institutions such as securities firms, funds, and trusts.

Second, diversification of technology pathways.

Driven by requirements related to economic viability and safety, technologies such as sodium-ion batteries and vanadium redox flow batteries are expected to develop in parallel, resulting in a diversified technological landscape.

Third, microgrid integration.

Following the introduction of policies supporting green power direct supply, localized distribution networks are being deployed more extensively. In the future, local wind and solar resources will be integrated into comprehensive energy microgrid systems, with distributed energy storage playing a smoothing role to enhance system safety and stability.

Fourth, enhanced convenience.

Distributed energy storage systems are typically smaller in capacity and are often deployed using temporary building structures, featuring modular designs that enable faster installation, easier maintenance, and advantages in mobility and scalability.

Fifth, AI-driven operation.

By integrating local energy balance data into control platforms and enabling interaction with energy storage systems, combined with weather and load variations, AI-based deployment can be used to forecast future loads, achieve localized microgrid balancing and regulation, and continuously optimize system performance.

When discussing how to address the development challenges of distribution transformer area energy storage, the expert emphasized that the first priority should be to enhance the safety of energy storage systems and establish corresponding standards and operational guidelines, enabling grid operators to carry out operation and maintenance in a regulated and standardized manner, while also mobilizing investment enthusiasm across society. In addition, the overall beneficiaries of Taqu energy storage deployment include local users, local governments, and society as a whole. Users benefit from high-quality, stable, and sufficient electricity supply; local governments enhance their ability to attract investment by strengthening power supply security; and society benefits from the clean, low-carbon, and secure development of the power system. Therefore, it is recommended that grid companies be encouraged to regularly publish demand for Taqu energy storage, and, under the premise of government-backed public welfare investment mechanisms (such as capacity payments or subsidies), promote diversified investment. Ultimately, this approach would form socialized assets maintained and operated by grid companies or their professional entities, achieving a shared investment and benefit distribution mechanism that benefits the state, government, enterprises, and individuals alike.

Wang Shuyang, Deputy Director of the Supply–Demand Interaction Division at the Energy Consumption Research Institute of the China Electric Power Research Institute, pointed out that the proportion of distributed energy storage participating in system operation through virtual power plants (VPPs) remains relatively low at present. There are two main reasons for this situation. First, the volume of energy storage resources aggregated by virtual power plants is still limited. Second, user-side energy storage systems are typically located within user premises and often lack independent metering devices. As a result, during statistical accounting, these systems are frequently classified as either generation sources or loads, making it difficult to separately identify and account for them as distributed energy storage.

In terms of market participation, Wang Shuyang explained that virtual power plants currently mainly participate in the energy market, peak-shaving market, and demand response programs, while Hubei Province has also explored participation in secondary frequency regulation. In the spot electricity market, provinces such as Shanxi, Shandong, Ningxia, and Fujian have already carried out pilot practices. For example, Shanxi has enabled virtual power plants to earn revenue from their regulation activities by relaxing medium- and long-term contract constraints. Regarding peak-shaving ancillary services, the North China region has launched regional peak-shaving ancillary services since November, with the Jibei Integrated Energy Virtual Power Plant demonstrating strong participation performance. Meanwhile, Zhejiang Province conducted normalized response regulation for new market entities during this year’s summer peak period.

Wang Shuyang emphasized that, as a high-quality flexibility resource, distributed energy storage inevitably needs to participate in the power market through aggregation mechanisms such as virtual power plants. This approach not only reduces decision-making costs for individual resources, but also enables numerous small-scale distributed energy storage units to collectively meet market access thresholds, thereby generating economies of scale and enhancing bargaining power in the electricity market.

He further noted that distributed energy storage could continue to explore participation in additional ancillary services, such as frequency regulation and voltage regulation, in the future. Compared with standalone energy storage, distributed energy storage may face cost pressures in the application of grid-forming technologies, which calls for technological breakthroughs to enable lightweight, standardized mass production, so as to better realize its regulation capabilities. At the policy and regulatory level, Wang Shuyang highlighted the need to promote the installation of independent metering for distributed energy storage systems, facilitating accurate measurement and settlement in a market-based environment. In addition, due to the highly decentralized nature of distributed energy storage, achieving effective coordination with grid operations requires the application of AI technologies to optimize decision-making and fully leverage the regulation potential of distributed energy storage resources.

Peng Kuankuan, Deputy General Manager of Domestic Marketing at Shanghai Pylon Technology Co., Ltd., pointed out that the business models of distributed energy storage mainly include time-of-use (TOU) price arbitrage, virtual power plants (VPPs), and demand-side response. Among these, the TOU peak–valley arbitrage model is relatively stable, while revenue streams from other models still face significant uncertainty. From the perspective of the current overall market environment, distributed energy storage on the user side exhibits a high degree of decentralization, a characteristic that determines the diversity of its application scenarios. He emphasized that across different scenarios, the most important missions of distributed energy storage are to reduce costs for customers, ensure the reliability and security of electricity supply, and achieve effective coordination with green power.

Peng Kuankuan noted that in recent years, data centers have become a key area of focus for the energy storage industry. Although data center energy storage has been deployed in China for many years, practical operation still faces challenges related to policy frameworks, electricity pricing, and safety, with safety concerns being particularly prominent among data center owners and tenants.

In the past, data center energy storage largely followed the logic of commercial and industrial energy storage. However, current application scenarios are gradually expanding to support multiple functions, including:

reducing data center carbon emissions through the use of green electricity;

lowering electricity costs through peak shaving and valley filling, while paying close attention to capacity charges and safety issues;

serving as backup power; and

smoothing short-term peak load fluctuations, especially as AI data centers become more widespread.

Peng Kuankuan also highlighted telecom base station energy storage as a highly promising application scenario. China has a vast number of telecom base stations—over ten million nationwide—with relatively concentrated customers, mainly the three major telecom operators and China Tower, making the business model easier to implement. This year, his company has supplied power to base stations through “distributed PV + energy storage” solutions and carried out peak shaving and valley filling practices. From an economic perspective, this model has demonstrated relatively stable returns. More importantly, given the large number of base stations, effective coordination between energy storage systems and base stations could unlock substantial dispatchable resources and achieve considerable aggregate scale.

Peng Kuankuan further pointed out that whether distributed energy storage business models can achieve breakthroughs in the short term depends on two key factors: policy and technology. From a policy perspective, the framework of market mechanisms is expected to become clearer over the next three years, although overall maturity will remain limited; over a longer time horizon, the outlook is more optimistic. From a technology perspective, the continued decline in energy storage costs will accelerate the maturation of business models, which has also been a key driver behind the industry’s rapid growth in the past. Regarding safety considerations, he noted that grid companies are more concerned with the reliability of response rather than the intrinsic safety of individual devices. As distributed energy storage consists of decentralized terminal resources that typically participate in dispatch through virtual aggregators, grid operators do not directly control these devices. Therefore, safety concerns do not undermine grid confidence in dispatch, and the safety performance of mainstream battery technologies is already sufficient to meet current application requirements.

Gao Zhiyuan, Marketing Director of XYZ Storage (Beijing) Co., Ltd., stated that following the release of the basic operating rules for the power market, the most significant change has been the formal recognition of energy storage as a distinct market entity. Previously, energy storage mainly played a supporting role within the power system; going forward, its more important role will be that of a flexible regulation resource. With the identity of energy storage clarified, various regions have introduced corresponding pilot and demonstration policies. For example, Guangdong Province released the Implementation Rules for the Operation and Management of Virtual Power Plants in Guangdong (Trial), under which virtual power plants aggregating distributed energy storage have begun participating in frequency regulation and peak-shaving ancillary services of the Guangdong power grid. In August this year, Zhejiang Province issued the Implementation Rules for Market-Oriented Response of New Market Entities in the Power Sector of Zhejiang (Trial), enabling energy storage systems deployed in certain projects to participate in virtual power plant bidding, fully demonstrating the flexibility of energy storage and its capability to participate in electricity markets. Shandong Province has also introduced relevant policies supporting the participation of distributed energy storage in capacity compensation mechanisms and power trading. Under the encouragement of national and local policies, as well as support from state-owned capital and private investment, distributed energy storage has begun to participate in the power market as an independent entity. Its revenue structure has evolved from a single electricity price spread model to a diversified combination of market-based trading, ancillary services, and targeted local subsidies, with these cases serving as effective demonstrations for broader replication. However, Gao Zhiyuan emphasized that transforming these pilot projects into widespread market practices will still require joint efforts from both government and industry, as well as full utilization of market-based adjustment mechanisms. For instance, policy adjustments have created certain challenges for photovoltaic projects, and many commissioned distributed PV systems are facing returns below expectations. By retrofitting these projects with an appropriate proportion of energy storage, it is possible to optimize the overall electricity price structure and improve project returns.

Drawing on the company’s practical project experience, Gao Zhiyuan introduced the application of distributed energy storage across different scenarios. He pointed out that distributed energy storage can effectively address “source–load interaction”, and that future development should focus on the load side, with in-depth analysis of specific scenarios. Beyond electricity price-related revenues, it is necessary to explore additional value streams and marginal benefits. In the data center scenario, this involves not only understanding electricity consumption characteristics and distribution system structures, but also addressing safety and space constraints. Data centers have a rigid demand for backup power as well as for energy storage. By leveraging electricity price differentials and regulation-induced fluctuations to capture marginal arbitrage value, energy storage can achieve an integrated “backup-plus-storage” model. In the telecom base station sector, base stations require backup power and consume large amounts of electricity, while communication reliability is particularly critical during extreme weather events. Energy storage can enhance power supply reliability while also enabling energy storage and dispatch functions. This model is expected to create new application scenarios that meet essential operational needs while generating additional marginal value, thereby stimulating investment enthusiasm across the industry.

Zhang Mingjun, Project Manager and Deputy Dean of the Virtual Power Plant Research Institute at Shanxi Fengxing Measurement & Control Co., Ltd., explained that at present, distributed energy storage participates in electricity trading mainly through aggregation by virtual power plants (VPPs), involving medium- and long-term transactions and spot markets in the wholesale market, as well as demand response and peak-shaving ancillary services. However, in many regions, regulations stipulate that a virtual power plant can obtain only one source of revenue for the same regulation capability during the same time period. For example, in Shanxi Province, a VPP’s regulation capacity during a given time period can participate in only one market—either conventional electricity retail combined with demand response, or the electricity spot market.

Zhang Mingjun expects that distributed energy storage will experience significant development in terms of technology, markets, and business models in the future. At the technological level, progress will primarily rely on “AI+” applications to achieve more accurate load forecasting and electricity price forecasting, enabling distributed energy storage charging and discharging strategies to better align with price signals. From a market perspective, the profit potential of distributed energy storage is expected to expand further. In addition to participating in wholesale market transactions through VPPs to capture price spreads between medium- and long-term contracts and the spot market, distributed energy storage will also be able to generate revenue by participating in deep peak-shaving or reserve ancillary services. In addition, capacity markets are currently being piloted. Shanxi Province is exploring mechanisms whereby virtual power plants aggregate the total capacity of distributed energy storage to participate in capacity market transactions, providing long-term capacity support to the power system and thereby obtaining capacity compensation or leasing revenues. In terms of business models, Zhang Mingjun emphasized that traditional calculation models based solely on peak–valley price arbitrage will be completely phased out, and that distributed energy storage business models will evolve toward becoming true carriers of energy value. From a long-term perspective, this transformation will promote the healthy and sustainable development of the industry, as the real value of energy storage lies not merely in behind-the-meter peak–valley arbitrage, but in its ability—through virtual power plant aggregation—to provide flexibility and reliability support to the power system on the grid side. Under previous mechanisms, such flexibility was difficult to price and trade in a rational and effective manner.

Huang Hui, Senior Program Manager of the Energy Transition Program at the Natural Resources Defense Council (NRDC), stated that with the development of distributed renewable energy and diversified loads, the value of distributed energy storage is becoming increasingly multidimensional. At present, driven by policies promoting market access for distributed resources, local consumption of renewable energy, and the expanded use of green electricity across industries, distributed energy storage is transitioning from a simple commercial and industrial peak–valley arbitrage model toward serving as a supporting unit for distributed renewable energy integration—including smoothing output fluctuations and improving self-consumption rates—as well as a grid-supporting micro-regulation unit. From a technical perspective, distributed energy storage systems are required to evolve toward grid-forming capabilities and intelligent operation, with further improvements needed in response speed and control accuracy. At the same time, operational logic is gradually shifting from simple charging and discharging strategies to dynamic optimization across multiple markets.

Huang Hui noted that in terms of specific application scenarios, recent developments in green power direct supply, zero-carbon industrial parks, and data centers have significantly driven the rapid growth of distributed energy storage. This is primarily because these new policies set explicit requirements for on-site consumption of green electricity. For example, policies for zero-carbon industrial parks stipulate that electricity demand within such parks should be met primarily through direct supply of green power, with the direct supply ratio generally required to be no less than 50%. These application scenarios also impose high requirements for power supply reliability, and the rigid demand for stable and green electricity has become a key driver of distributed energy storage deployment. In addition, as market mechanisms gradually open up on the user side, revenue diversification has become another critical factor promoting the development of distributed energy storage. For instance, by aggregating distributed energy storage resources into virtual power plants, projects can participate in spot markets, frequency regulation, and reserve services, thereby increasing the revenues of individual projects. Meanwhile, the logic of power supply and consumption is shifting from a focus on electricity volume to an emphasis on power quality. In the future, different customers will have differentiated requirements for supply reliability and power quality levels. Distributed energy storage—particularly distribution transformer area (Taqu) energy storage—can achieve cost recovery by providing more reliable electricity and charging differentiated power quality service fees.

Huang Hui further emphasized that grid-side standalone energy storage and distributed energy storage each have their own advantages. For example, in frequency regulation, standalone energy storage features fast response, stable capacity, and more precise and controllable single-point regulation, resulting in higher suitability. Distributed energy storage, when aggregated into virtual power plants, is affected by factors such as communication constraints of dispersed resources and limited adjustable margins, leading to relatively lower adaptability and requiring technological upgrades to participate efficiently. However, distributed energy storage demonstrates greater advantages in managing distribution network congestion. Through the coordination of distributed energy storage and flexible loads across multiple nodes, virtual power plants can provide targeted solutions to distribution network congestion, highlighting a key system-level value that complements standalone energy storage.

CENSA Upcoming Events:

Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Dec 31, 2025.