Latest News

MoM Surge of 90%! Grid&Source-Side Energy Storage Rebounds Sharply in November, with Full-Year Scale Expected to Exceed Last Year

Source: CNESA

After a phase adjustment in China's new-type energy storage market in October 2025, the commissioning scale of new-type energy storage in November declined slightly year on year but rebounded markedly month on month. Meanwhile, the market's deeper structure adjusted compared with October:

Market recovery with a positive long-term outlook: Although installed capacity in November declined year on year, the month-on-month increase was significant. Newly added installations in the first 11 months reached nearly 40 GW, up more than 25% year on year, and full-year additions are expected to exceed last year.

Accelerated deployment of independent storage: In November, independent energy storage accounted for over 70%, with month-on-month growth rates exceeding 80% in power capacity and 200% in energy capacity. Inner Mongolia recorded more than 1.1 GW of newly commissioned independent storage, ranking first nationwide in both power and energy capacity.

Rise of local energy groups: Newly added installations by local energy groups reached a 45% share, surpassing for the first time the “Five Major and Six Minor” power generation groups and the “third-party enterprises”, highlighting a further diversification of market investors.

Faster rollout of diversified technologies: Beyond mainstream lithium batteries, technologies such as compressed air, flow batteries, and flywheels are being deployed at an accelerated pace, supporting the industry's long-term development.

Overall Analysis of New-Type Energy Storage Projects in November

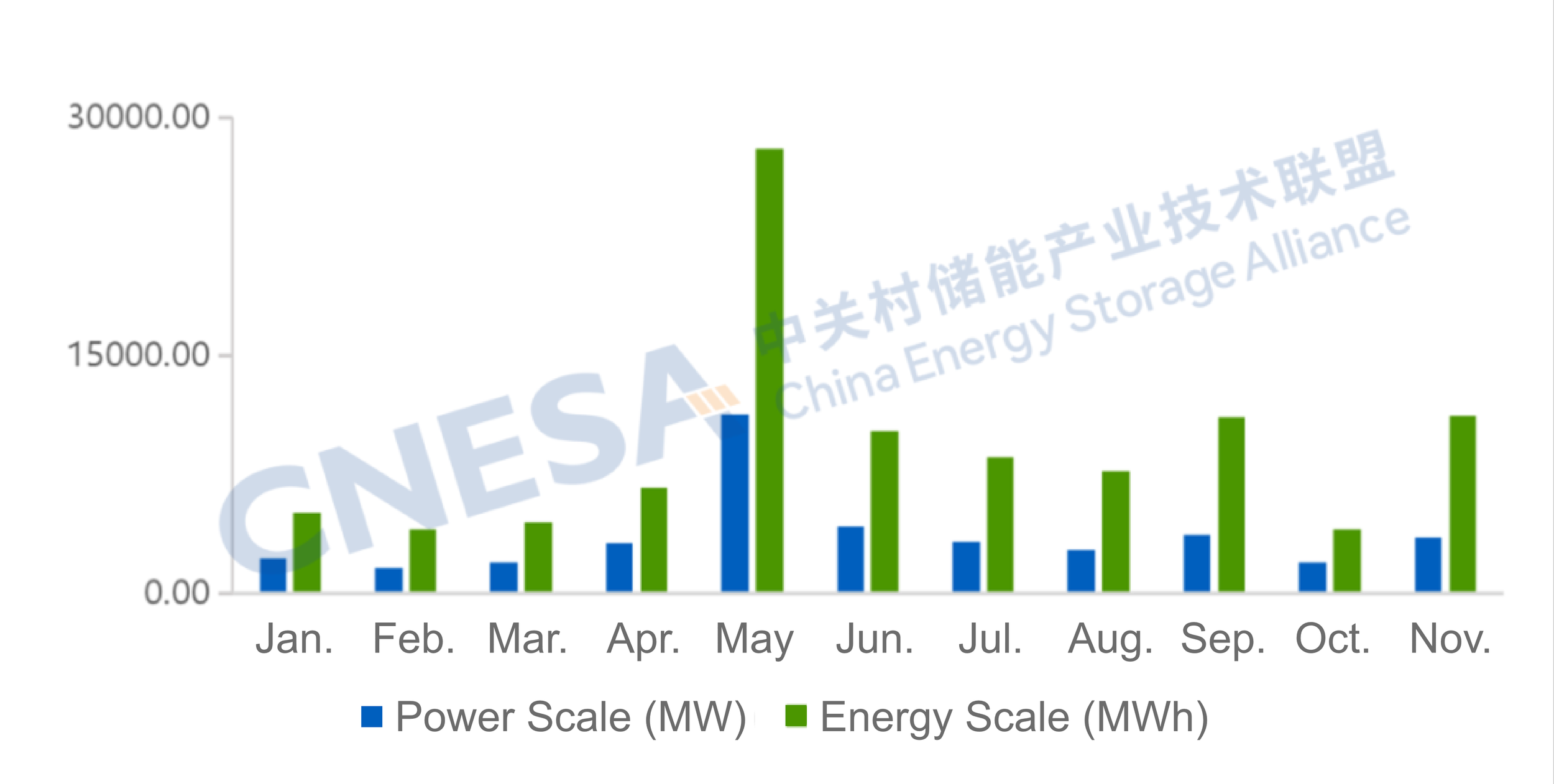

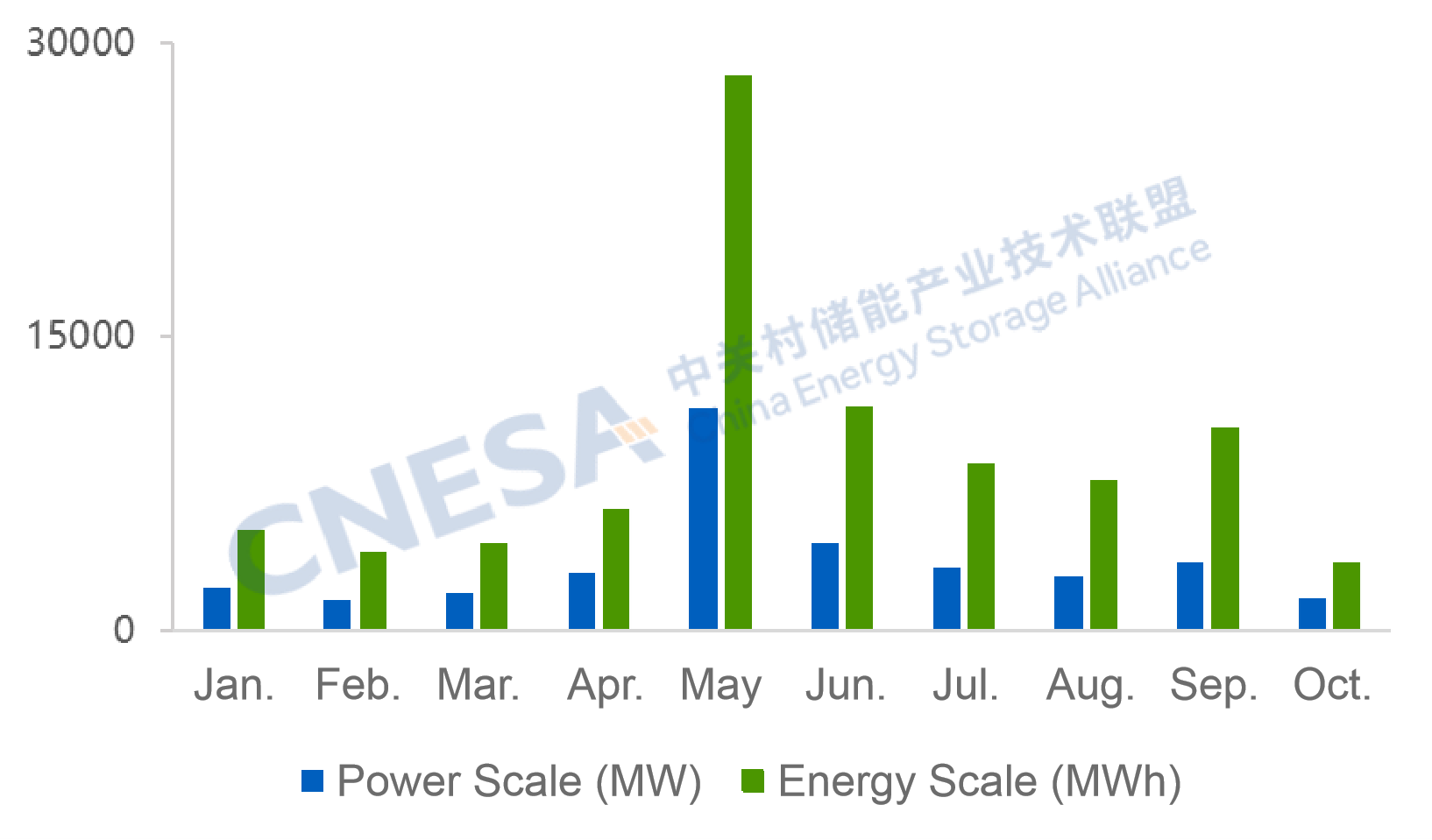

According to incomplete statistics from CNESA, in November 2025 China commissioned a total of 3.51 GW / 11.18 GWh of new-type energy storage projects, representing -22% / -7% year on year and +81% / +180% month on month. While monthly additions continued to decline year on year in November, cumulative additions in the first 11 months reached 39.5 GW, up 28% year on year. Considering potential concentrated grid connections ahead of the “12.30” commissioning deadline, total additions for the year are expected to exceed last year.

Figure 1. Installed Capacity of Newly Commissioned New-Type Energy Storage Projects in China, Jan-Nov 2025

Data source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: Year-on-year (YoY) compares the same period last year; month-on-month (MoM) compares the previous statistical period.

Analysis of Grid&Source-Side New-Type Energy Storage Projects in November

In November, newly added grid&source-side installations totaled 3.32 GW / 10.62 GWh, -15% / -1% year on year and +90% / +202% month on month.

Key characteristics include:

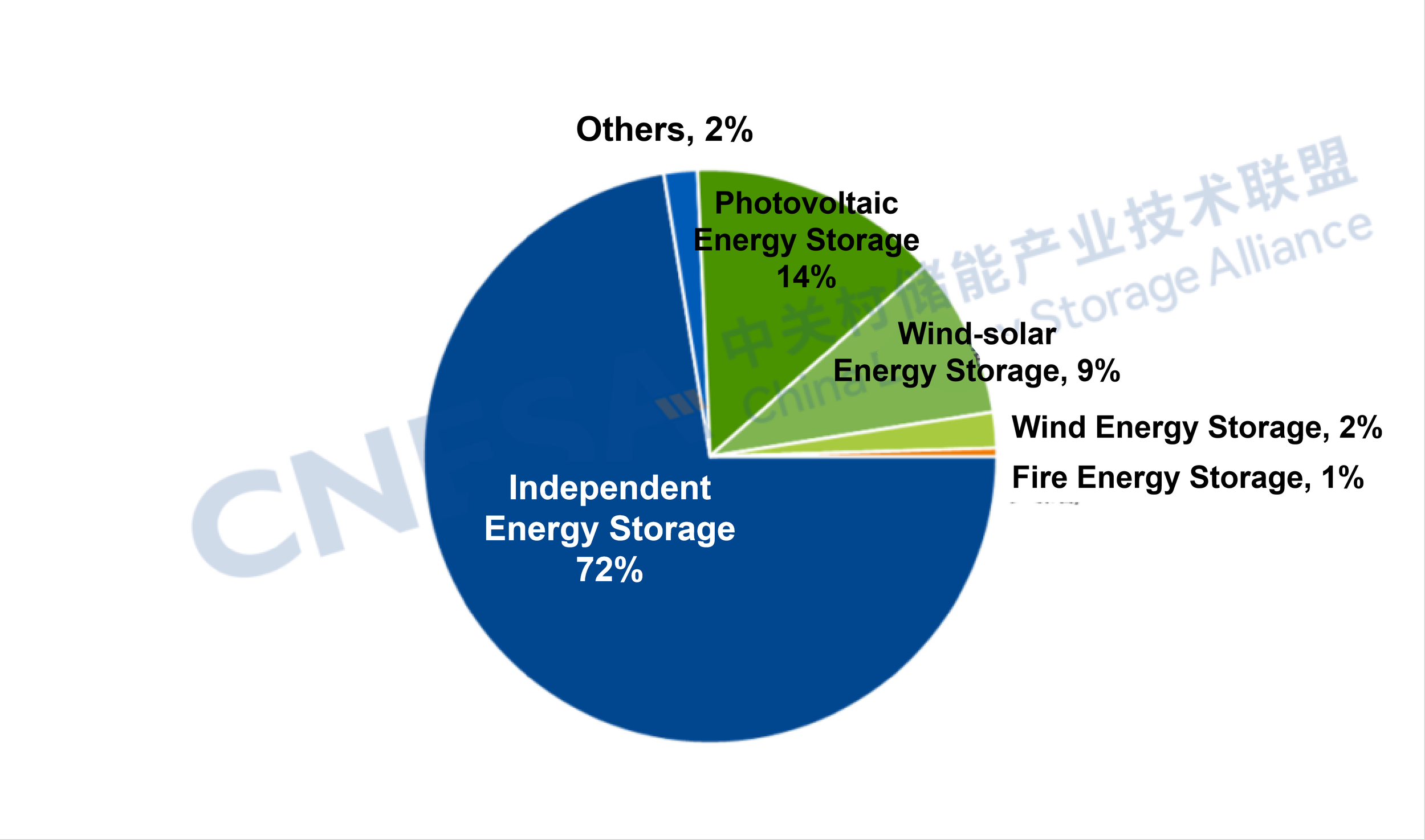

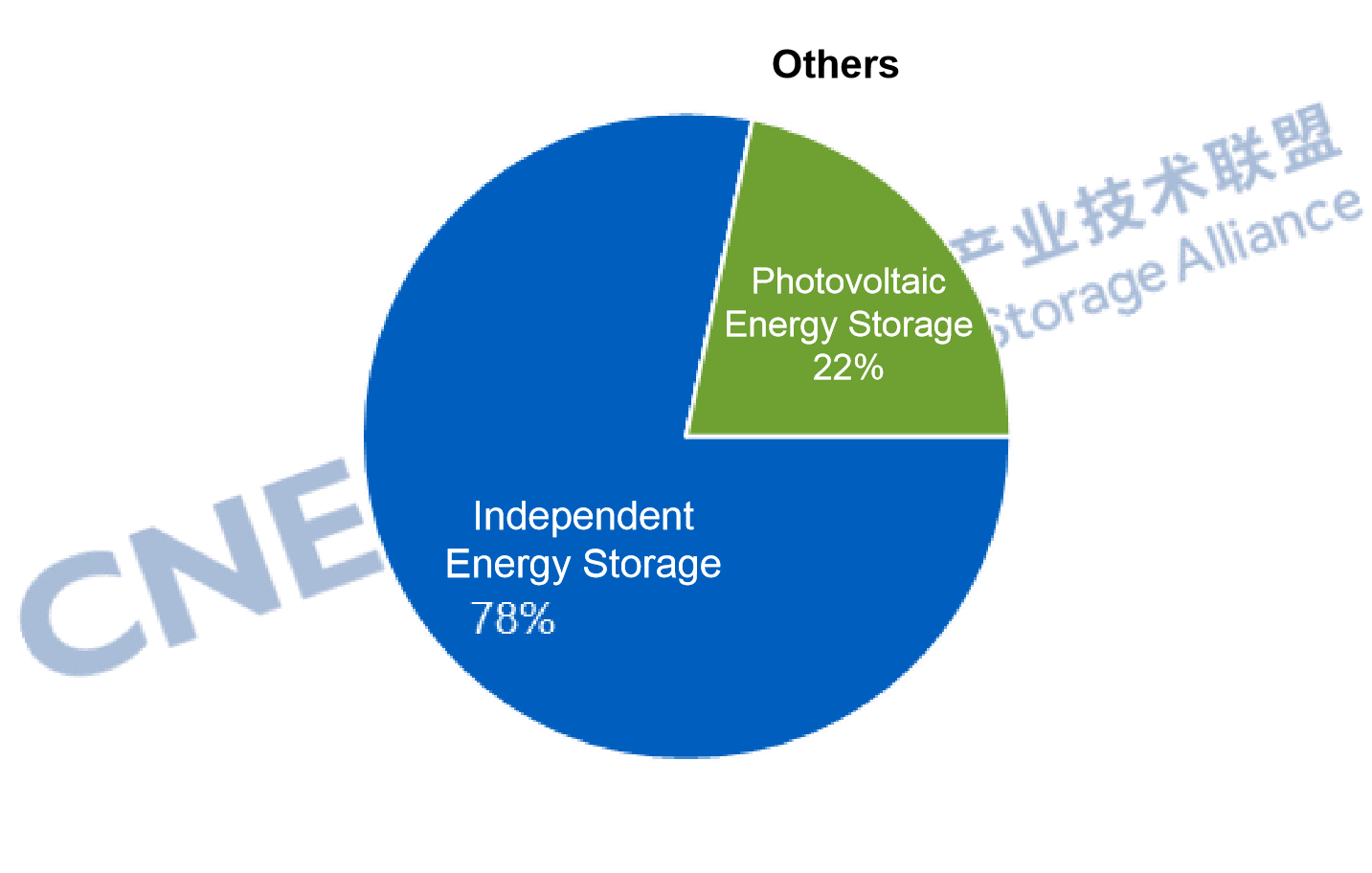

Newly added Independent storage accounted for 72%, down 6 percentage points from October.

Independent storage additions reached 2.41 GW / 8.19 GWh, -9% / +11% year on year and +82% / +217% month on month, with projects of 100 MW or above accounting for 79% by number.

Power-generation-side additions were 853.3 MW / 2,322.1 MWh, -33% / -31% year on year and +99% / +148% month on month. Renewable-plus-storage projects accounted for 98% of power capacity, covering multiple application scenarios such as UHV DC projects, agrivoltaics, and pastoral-solar hybrid systems.

Figure 2. Application Breakdown of Newly Commissioned Grid&Source-Side Energy Storage Projects in Nov. 2025 (MW%)

Data source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: “Others” include substations, emergency power supply, etc.

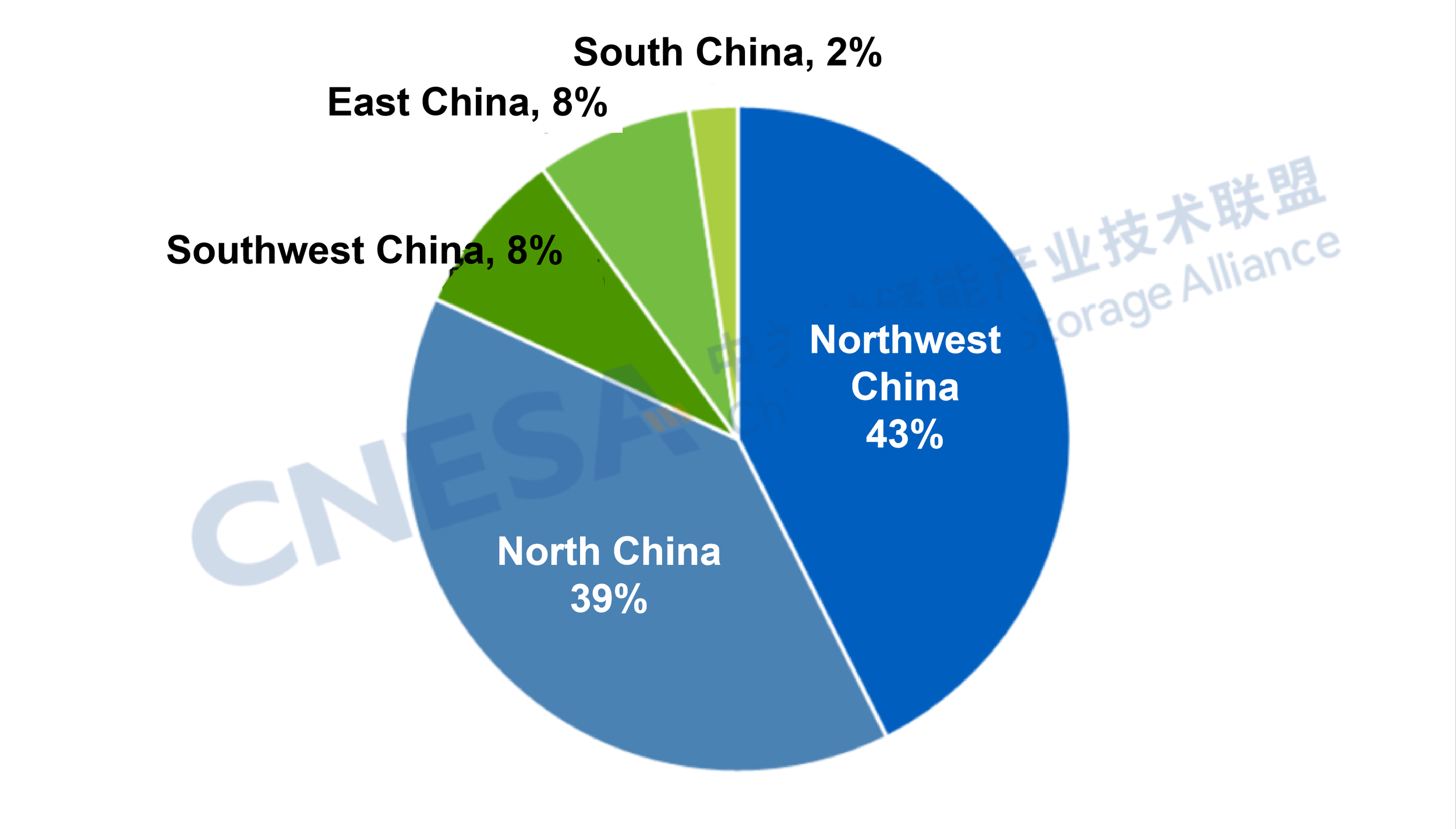

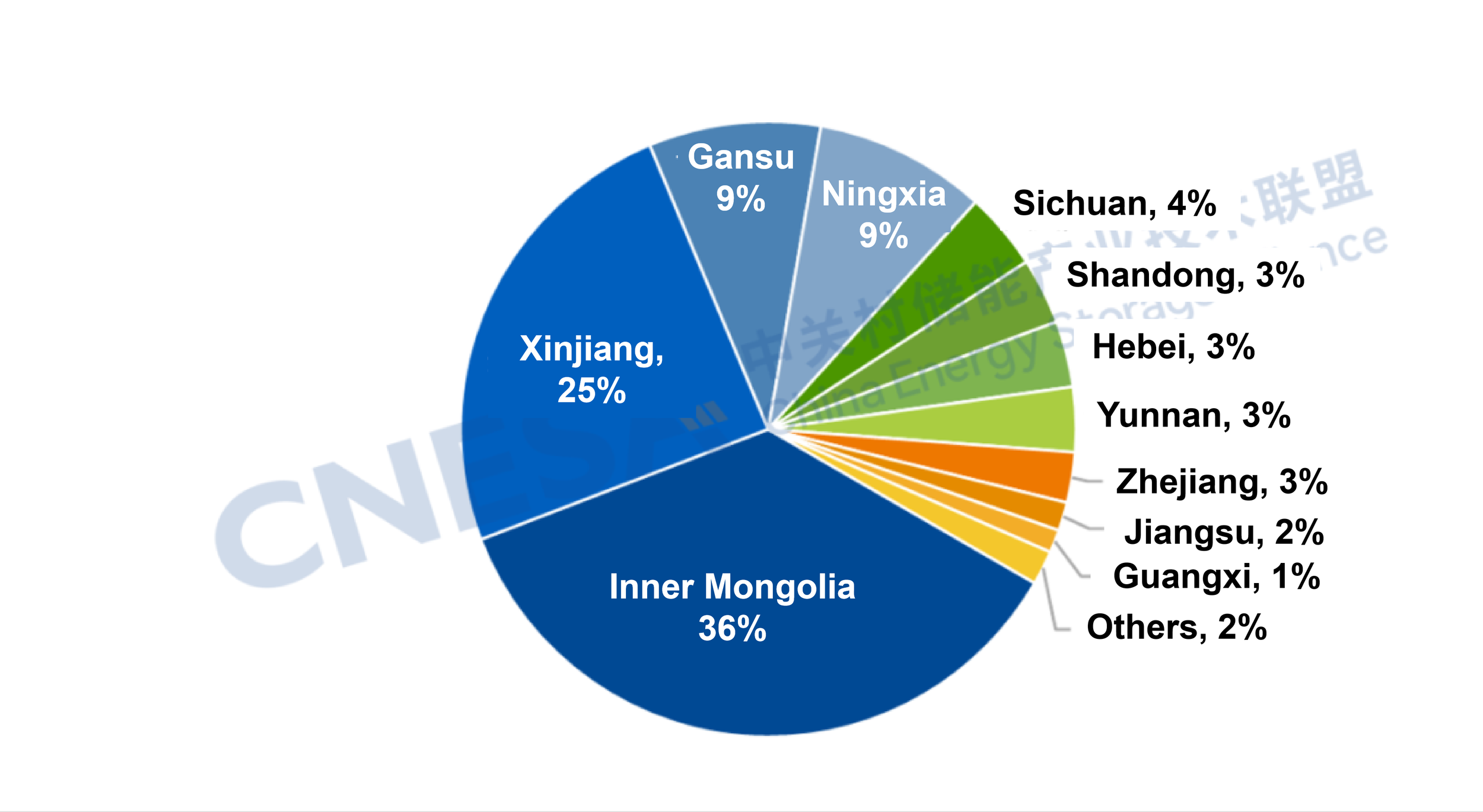

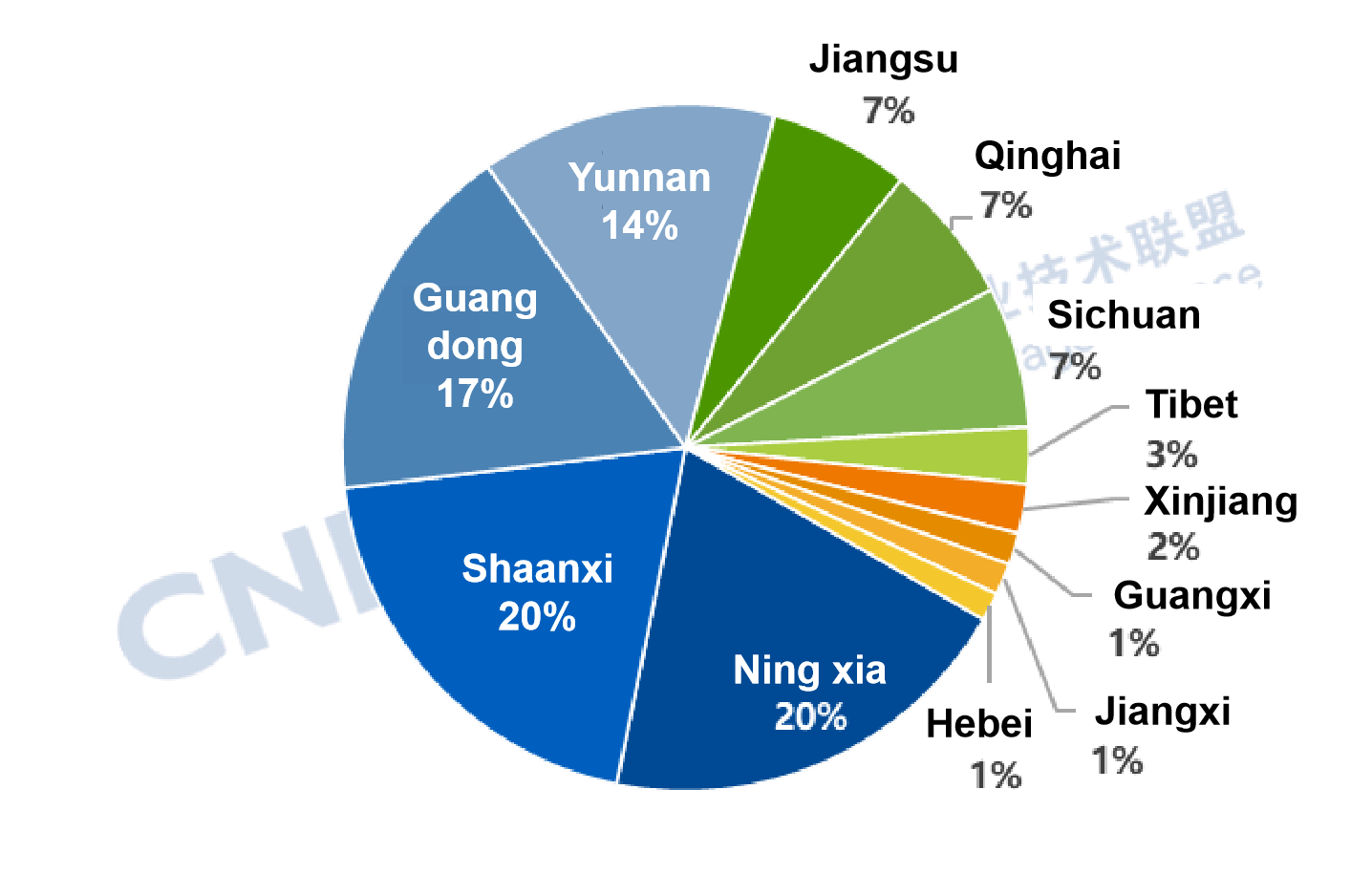

Northwest Leads with Over 40% Share; Inner Mongolia Ranks First

In November, the Northwest region accounted for 43% of newly added capacity, ranking first nationwide. Combined additions in the Northwest and Southwest exceeded half of the national total.

By province, the Inner Mongolia Autonomous Region saw multiple Independent grid-side demonstration projects commissioned - such as those included in the 2025 New-Type Energy Storage Special Action Implementation Project List and the first batch of Independent storage construction projects - totaling over 1.1 GW with an average storage duration of 4 hours, ranking first nationwide in both power and energy capacity. Xinjiang, Gansu, and Ningxia followed closely.

As a key national energy and strategic resource base in China, Inner Mongolia had surpassed 150 GW of installed renewable capacity by the end of October 2025, ranking first nationwide. Wind and solar accounted for over 80% of new installed capacity, further solidifying their dominant role (data source: Inner Mongolia Autonomous Region Energy Bureau). From the perspective of consumption, approximately 80% of renewable generation is consumed locally, with around 20% exported. The combined pressure of local consumption and grid stabilization continues to drive demand for new-type energy storage.

Figure 3. Regional Distribution of Newly Commissioned Grid&Source-Side Energy Storage Projects in China, November 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

Figure 4. Provincial Distribution of Newly Commissioned Grid&Source-Side Energy Storage Projects in China, November 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

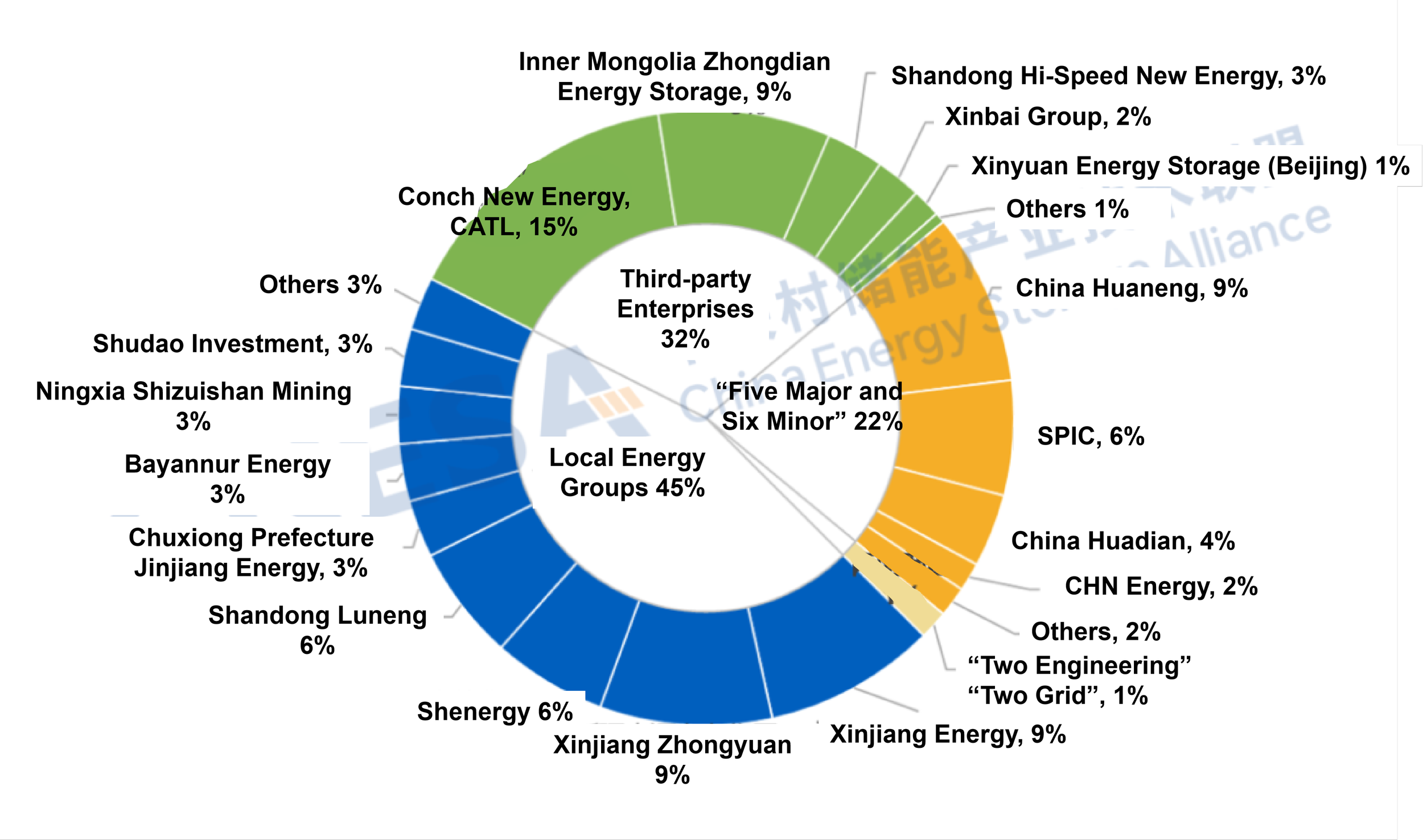

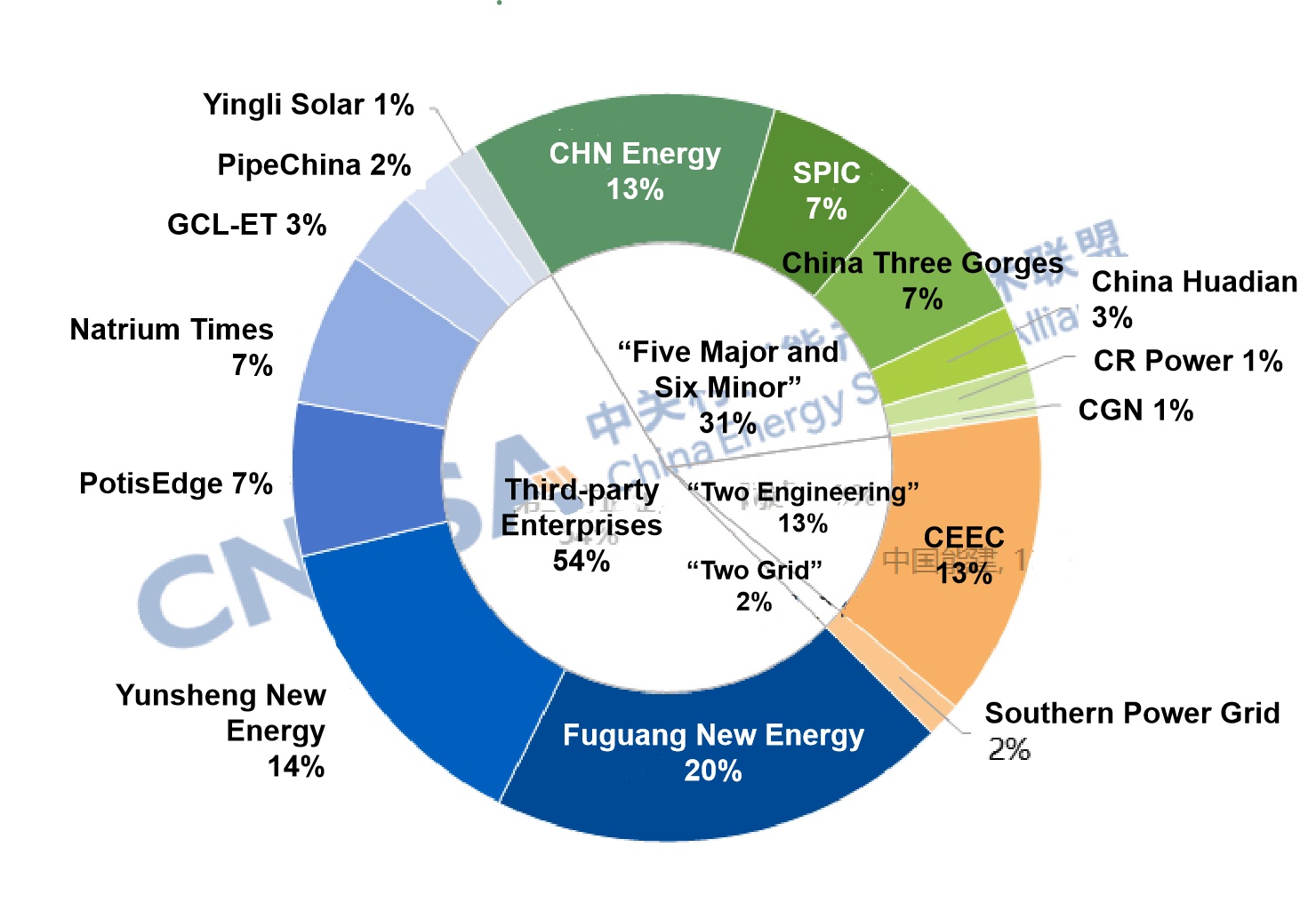

Faster Deployment by Local Energy Groups Highlights Investor Diversification

Driven by rising market demand, supportive national policies, diversified technology pathways, and declining costs, the market potential of energy storage is being fully released, with increasing investor diversification.

In November, projects invested in and built by local energy groups such as Xinjiang Energy Group, Xinjiang Zhongyuan Power Group, and Shenergy Group were commissioned in succession. Local energy groups accounted for 45% of newly added power capacity - the highest among all enterprise types - contrasting sharply with September and October, when third-party enterprises and the “Five Major and Six Minor” power generation groups dominated.

Leveraging advantages in policy coordination and approvals, resource integration and location, business linkage and industrial chain synergy, capital strength and decision-making efficiency, and operations, local energy groups have become a key pillar of the new-type energy storage market. Meanwhile, third-party enterprises - such as joint entities involving Conch New Energy and CATL, and Inner Mongolia Zhongdian Energy Storage - maintained a high level of participation, accounting for over 30% of monthly additions. The “Five Major and Six Minor” power generation groups (including China Huaneng, SPIC, and China Huadian) accounted for 22%, down 9 percentage points from October, continuing the decline seen since August.

Figure 5. Owner Distribution of Newly Commissioned Grid&Source-Side Energy Storage Projects in China, November 2025 (MW%)

Data source: CNESA DataLink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: “Third-party enterprises” refer to entities other than large state-owned generation groups, the two grid companies, two construction groups and local energy companies.

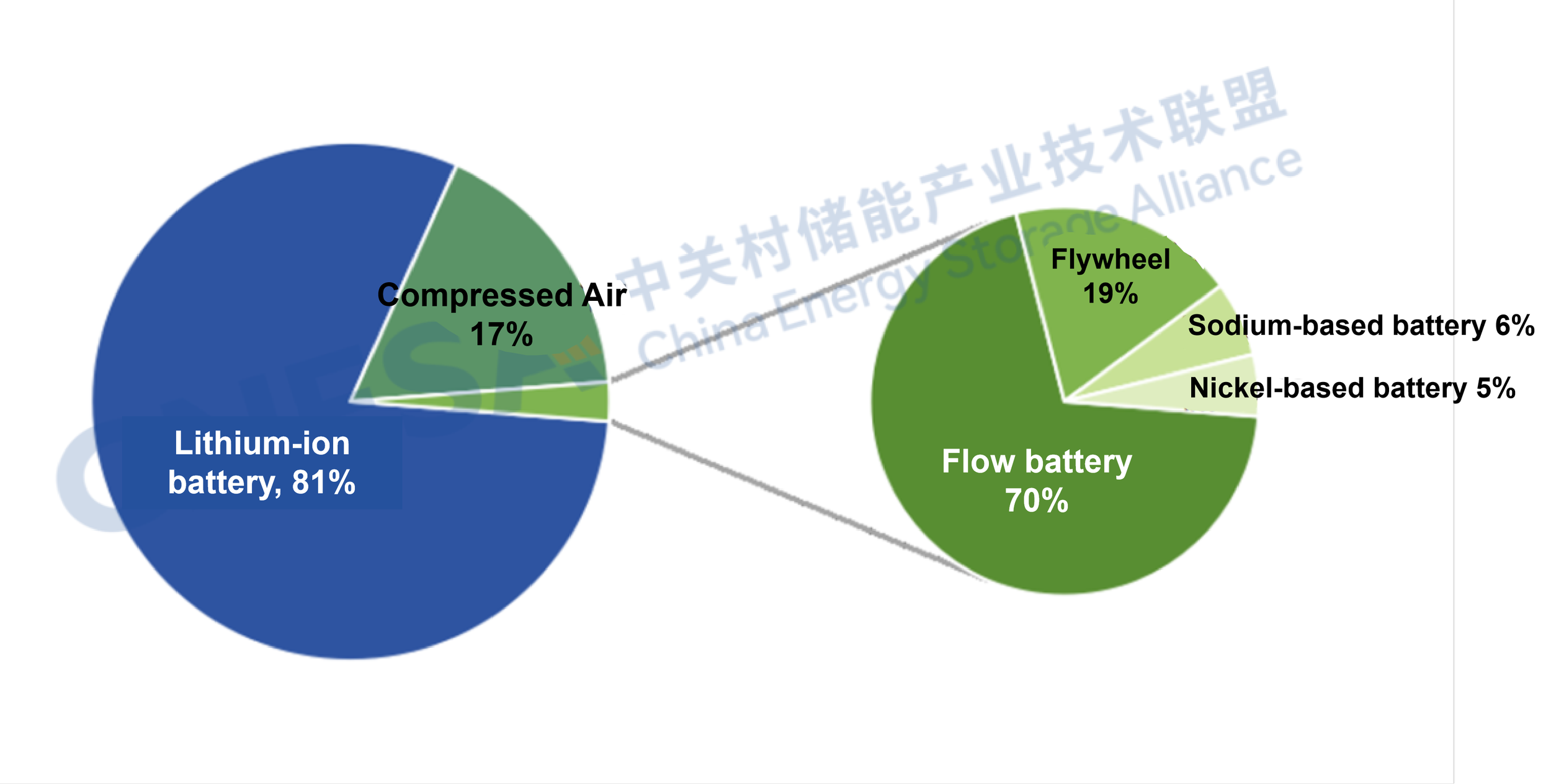

Accelerated Deployment of Non-Lithium Technologies

Technologically, newly commissioned grid&source-side projects were dominated by lithium iron phosphate (LFP) batteries, accounting for 91% of power capacity, followed by lead-carbon batteries (6%) and flow batteries (3%).

From a project development perspective, non-lithium technologies such as compressed air energy storage and hybrid systems are accelerating, highlighting a trend toward diversified technology pathways.

In compressed air storage, multiple 300 MW-class projects have completed filings and entered the planning stage; the Golmud 60 MW liquid air energy storage demonstration project and the Yumen 300 MW compressed air energy storage demonstration project have entered commissioning.

For hybrid storage, multiple 100 MW-class demonstration projects have launched or completed tenders, with some under construction or advancing, involving combinations such as lithium + sodium-ion batteries, lithium + flow batteries, lithium + flywheels, and lithium + nickel-metal hydride batteries.

Figure 6. Technology Distribution of Newly Planned and Under-Construction Grid&Source-Side Energy Storage Projects in China, November 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

The China Energy Storage Alliance (CNESA) has consistently adhered to standardized, timely, and comprehensive information collection practices to continuously track developments in energy storage projects. Leveraging its long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses on installed energy storage capacity, providing valuable references for industry decision-making. Since June 2025, the monthly energy storage project analysis has been divided into two sections: “Grid&Source-Side Market” and “User-Side Market”. This issue focuses on interpreting the grid&source-side market in November.

CENSA Upcoming Events:

Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Dec 31, 2025.

Down 35% Year-on-Year! CNESA Analysis of Installed Capacity of the New Grid&Source-Side Energy Storage Projects in October

Source: CNESA

After a small installation peak in September, China's new energy storage market saw a temporary decline in October 2025. According to incomplete statistics from the CNESA Datalink Global Energy Storage Database, both the month-on-month and year-on-year growth of newly commissioned capacity declined in October, mainly due to project cycle factors. Meanwhile, profound structural changes are taking place in the market:

● Short-term decline while long-term growth:

Although October's installed capacity declined, the cumulative capacity in the first ten months of 2025 still maintained a robust 36% growth, and 7-9 GW of projects are expected to come online before year-end, suggesting a record-breaking annual installation.

● Independent storage takes the lead:

In October, independent energy storage projects accounted for more than three-quarters of total installations, becoming the absolute main force.

● Third-party enterprises surpass state-owned giants:

A landmark shift occurred - “third-party enterprises”, represented by equipment manufacturers, accounted for over half of the newly installed capacity for the first time, surpassing traditional large energy groups and highlighting a clear trend toward diversified investment.

● Diverse technologies and accelerated non-lithium deployment:

In addition to mainstream lithium-ion systems, technologies such as compressed air, flow batteries, and flywheels are being accelerated in planning and construction, injecting new momentum into the industry's long-term development.

Overall Analysis of New Energy Storage Projects in October

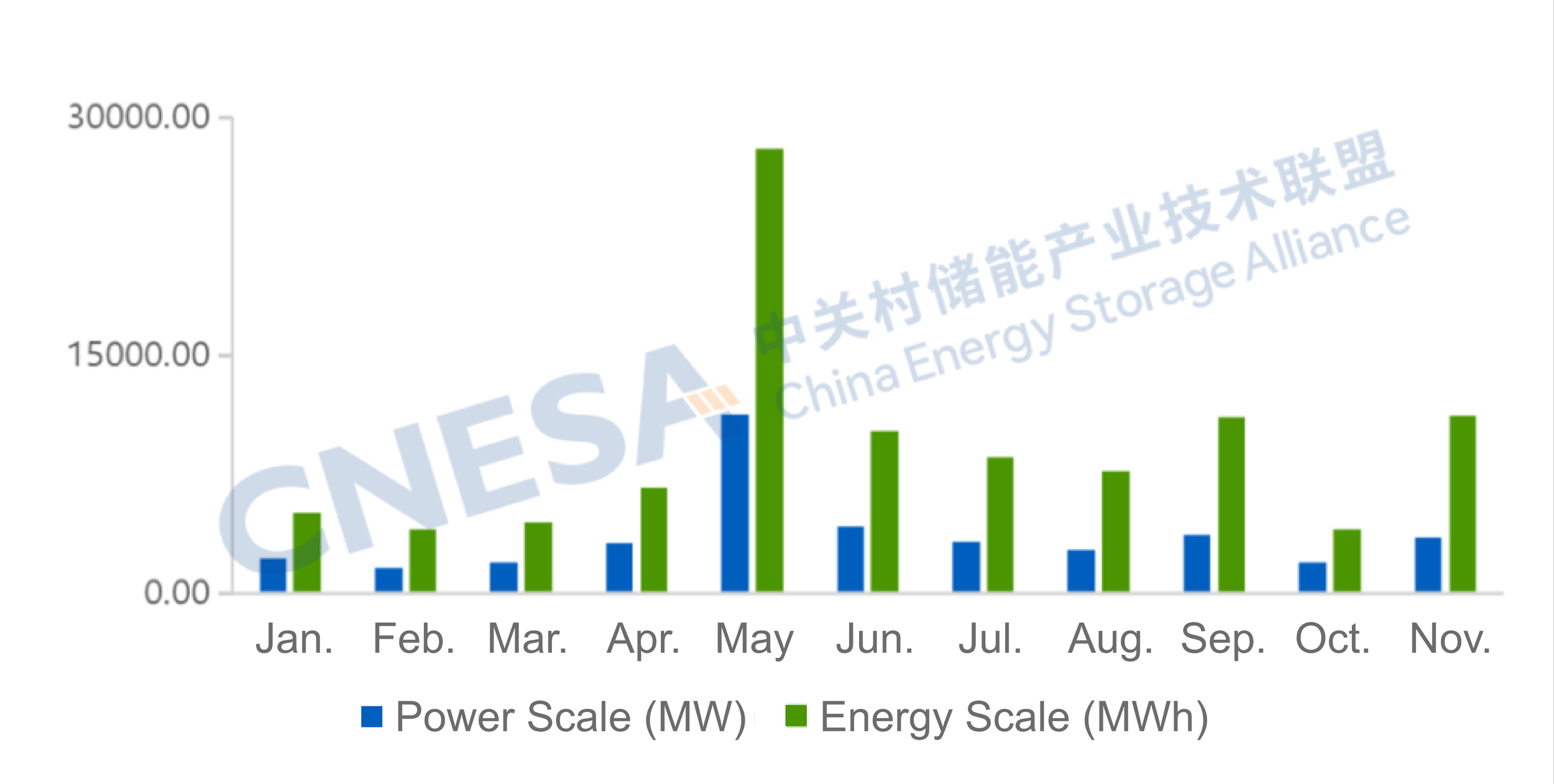

According to incomplete statistics from the CNESA Datalink Global Energy Storage Database, in October 2025, China added 1.70 GW / 3.52 GWh of newly commissioned new energy storage capacity - down 35% and 49% YoY, and 51% and 66% MoM, respectively. Although the first month of Q4 saw a decrease, total new capacity from January to October reached 35.8 GW, up 36% YoY. Following the September commissioning surge, the October decline mainly reflected the influence of construction cycles.

As of the end of October, about 7-9 GW of new energy storage projects were under commissioning or scheduled for grid connection by year-end. If these projects proceed as planned, China's new commissioned capacity in 2025 could reach 42-45 GW. This estimate is based solely on currently known under-construction/commissioned project data and does not represent a final forecast.

Figure 1. Installed Capacity of Newly Commissioned New Energy Storage Projects in China, Jan-Oct 2025

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: Year-on-year (YoY) compares the same period last year; month-on-month (MoM) compares the previous statistical period.

Analysis of Grid&Source-side New Energy Storage Projects in October

In October, newly commissioned grid&source-side new energy storage capacity totaled 1.51 GW / 3.04 GWh, representing year-on-year declines of 35% and 49%, and month-on-month declines of 53% and 69%.

Key trends included:

Independent storage accounts for over 75%, with capacity down 30% YoY

Independent energy storage added 1.18 GW / 2.31 GWh, down 30% and 48% YoY, with 78% of projects above 100 MW.

On the source side, new installations totaled 327.5 MW / 735 MWh, representing a YoY growth of -47%/-52%, all paired with renewable energy projects, involving various specific application scenarios including UHV DC transmission and solar-grazing hybrid application.

Figure 2. Application Distribution of Newly Commissioned Grid&Source-Side Energy Storage Projects in Oct. 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: “Others” include substations and similar facilities.

Western China accounts for over 50% of new installations; Ningxia and

Shanxi lead in scale

By region, western China contributed over half of October's new capacity, with the northwest region alone accounting for nearly 30%, the highest nationwide.

By province, Ningxia and Shanxi province ranked joint first in new power capacity, while Ningxia topped in new energy capacity.

As a key national new energy demonstration zone, Ningxia's renewable capacity had exceeded 50 GW by August 2025, representing 60% of total power installations - with solar surpassing coal to become the largest power source.

High proportions of wind and solar have created growing demand for storage to smooth grid fluctuations and enhance renewable integration. In addition, large-scale national initiatives such as the “Desert, Gobi and Wasteland” renewable base and UHV DC transmission projects have further expanded the application space for energy storage in Ningxia.

Figures 3. Regional Distribution of Newly Commissioned Grid&Source-Side New Energy Storage Projects in China, Oct. 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

Figures 4. Provincial Distribution of Newly Commissioned Grid&Source-Side New Energy Storage Projects in China, Oct. 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

Third-party enterprises drive growth, highlighting diversification of

investors

Driven by rising market demand, national policy incentives, technological diversification, and declining costs, the energy storage market's investment ecosystem is becoming increasingly diverse.

In October, projects invested by private power companies such as Fuguang New Energy and Yunsheng New Energy and energy storage/new energy manufacturers such as PotisEdge and Natrium Times (NTEL) accounted for over 50% of new installations - up 18 percentage points from September.

Nevertheless, large state-owned energy groups remain key players due to their advantages in project investment scale, construction coordination, and operational management.

In October, China's “Five Major and Six Minor” and “Two Grid and Two Engineering” state-owned power enterprises contributed 46% of newly installed capacity. Among them, “Five Major and Six Minor” and “Two Grid and Two Engineering” including CHN Energy, SPIC, and China Three Gorges Corporation accounted for 31%, down 10 percentage points from September, while the “Two Grid and Two Engineering” increased their share by 4 points.

Figure 5. Ownership Distribution of Newly Commissioned Grid&Source-side New Energy Storage Project in China, Oct. 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

Note: “Third-party enterprises” refer to entities other than large state-owned generation groups, the two grid companies, two construction groups and local energy companies.

Acceleration in non-lithium technology deployment

From a technical perspective, newly commissioned grid&source-side projects were dominated by lithium iron phosphate batteries, accounting for 98.5% of capacity, with sodium-ion batteries representing 1.5%.

In terms of planned and under-construction projects, deployment of non-lithium technologies such as compressed air and hybrid storage is accelerating, signaling faster diversification of technology pathways.

Compressed air: Multiple 100 MW-level compressed air projects have completed filing and entered the planning stage; the 350 MW Anning (Yunnan) compressed air project has begun construction.

Hybrid storage: Hebei Province announced a pilot list including 97 hybrid projects totaling 13.82 GW; construction of two 100 MW lithium + flow battery projects began in Weifang, Shandong; the 100 MW flywheel-lithium hybrid station is under construction in Heishan, Liaoning; the 300 MW / 1200 MWh independent power-side storage project using lithium + flow battery hybrid technology has entered the grid-commissioning stage at Gushanliang, Ordos, Inner Mongolia.

Figure 6: Technological Distribution of Newly Commissioned Grid&Source-Side New Energy Storage Projects in China, Oct. 2025 (MW%)

Source: CNESA Datalink Global Energy Storage Database

https://www.esresearch.com.cn/

The China Energy Storage Alliance (CNESA) has consistently adhered to standardized, timely, and comprehensive information collection practices to continuously track developments in energy storage projects. Leveraging its long-term data accumulation and in-depth professional analysis, CNESA regularly publishes objective market analyses on installed energy storage capacity, providing valuable references for industry decision-making. Since June 2025, the monthly energy storage project analysis has been divided into two sections: “Grid&Source-Side Market” and “User-Side Market”. This issue focuses on interpreting the grid&source-side market in October.

CENSA Upcoming Events:

1. Dec.4-5 | 2025 China Energy Storage CEO Summit | Xiamen, Fujian

Register Now to attend

Read more: http://en.cnesa.org/new-events-1/2025/12/4/dec4-5-2025-china-energy-storage-ceo-summit

2. Apr. 1-3, 2026 | The 14th Energy Storage International Conference & Expo

Register Now to attend, free before Oct 31, 2025.

Sign up for our free monthly newsletter to stay informed about the Chinese energy storage market.